Latin America Diabetes Devices Market

Latin America Diabetes Devices Market Share & Trends Analysis Report By Product Type (Blood Glucose Monitoring Devices, Insulin Delivery Devices, Continuous Glucose Monitoring (CGM) Devices, Smart Insulin Pens, Diabetes Management Apps & Software) By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Diabetes Clinics) By End User (Hospitals, Homecare Settings, Diagnostic Centers, Ambulatory Surgical Centers) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

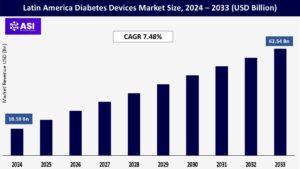

CAGR: 7.48%

Last Updated : March 7, 2026

The global Latin America Diabetes Devices Market was valued at approximately USD 18.58 billion in 2024 and is projected to reach USD 62.54 billion by 2033, growing at a CAGR of 7.48% during the forecast period (2025–2033).

Diabetes devices are essential instruments that monitor and manage blood glucose levels in patients with diabetes. The devices include blood glucose meters, continuous glucose monitors (CGMs), insulin pens, insulin pumps, and lancets. The purpose of diabetes devices is to monitor and manage blood glucose levels. They are necessary in maintaining glycemic control, reducing complications, and improving patient outcomes.

The increasing burden of diabetes across Latin America will contribute to the demand for diabetes devices. Urbanization, sedentary lifestyles, dietary changes, and lack of physical activity have increased the burden of diabetes across Latin America. The heightened demand for advanced technology in diabetes care is also due to rising awareness among patients, increased healthcare access, when necessary, and various public health programs to increase awareness and education on early diabetes diagnosis, intervention and management.

A rising burden of diabetes in Latin America is a critical driver of the diabetes devices market. As reported by the International Diabetes Federation (IDF), approximately 32 million adults in the region were diabetic in 2021, and projections are estimated to reach as high as 49 million adults living with diabetes by 2045. Countries like Mexico, Brazil, and Argentina all have alarming rates of Type 2 diabetes, with increases attributable to rapid urbanization, consumption of processed foods, high sugar intake, and sedentary lifestyles. For example, Mexico has one of the highest rates of Type 2 diabetes in the world, with more than 14% of the adult population affected and suspected even more undiagnosed.

The continuing rise of childhood and adult obesity—a major risk factor for diabetes—continues to be prevalent. PAHO estimates that in Latin America, 60% of adults and 20% of children are overweight or obese. In acknowledgment of the public health challenge of diabetes, many governments are implementing national diabetes awareness and control programs. One example is Brazil’s “Strategic Action Plan to Tackle NCDs 2021–2030”, which emphasizes early diagnosis and ongoing follow-up care in order to stimulate increased demand and access to blood glucose meters and insulin devices.

Rapid development of diabetes technology is changing disease management in Latin America, benefitting patients with devices that provide more precise and user-friendly connections to devices. One good example is Abbott’s FreeStyle Libre 2 CGM system, which launched in Brazil and Chile in 2023, and provides users with real-time glucose readings that do not require fingersticks.

Its affordability and ease of use have made it a popular CGM across Latin America – especially among younger people and those in middle-income groups. Medtronic also expanded into Latin America in late 2023, by offering the MiniMed 780G insulin pump system in selective countries like Argentina and Mexico. The pump system features automated insulin delivery using SmartGuard technology to reduce the frequency of hyperglycemia and hypoglycemia.

Digital health start-ups are also disrupting the market in Latin America. For example, GlucoseUp, a Mexican healthtech start-up, offered a new mobile app in 2024 that integrated with Bluetooth – enabled glucose monitors and insulin pens, enabling remote monitoring by endocrinologists and primary care physicians. This product addresses access gaps in regions with limited access to health care and takes every opportunity to engage the patient in real-time.

The high costs of advanced diabetes devices along with limited healthcare access are extremely restrictive to market growth in Latin America. For many populations, the costs of managing diabetes with advanced devices such as continuous glucose monitors (CGMs) and insulin pumps is unreasonable, as CGMs cost $100 or more per sensor and insulin pumping systems cost over $3,000.

Basic glucose meters and syringes are available through public health systems in multiple countries such as Bolivia and Paraguay, but coverage for newer technologies is nonexistent. More than 70% of medical technologies are imported into many Latin American countries, making them vulnerable to tariffs and fluctuating currency which further increases costs.

Limited insurance coverage and insufficient public systems make access to devices unequal, particularly to those in remote or underserved settings. These economic and structural barriers limit patient access to tools for effective diabetes management preventing many patients from being able to access diabetes devices that might assist with long-term health outcomes.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Blood Glucose Monitoring Devices Insulin Delivery Devices Continuous Glucose Monitoring (CGM) Devices Smart Insulin Pens, Diabetes Management Apps & Software

|

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies Diabetes Clinics

|

| By End User |

Hospitals Homecare Settings Diagnostic Centers Ambulatory Surgical Centers

|

| Key Players |

Abbott Laboratories Medtronic plc Roche Diabetes Care Dexcom, Inc. Becton Dickinson (BD) Sinergium Biotech DAIICHI SANKYO Ascensia Diabetes Care Insulet Corporation Nipro Corporation |

| Geographies Covered | |

| Latin America |

Brazil |

The Latin America Diabetes Devices Market is segmented by product type and end-user. Each segment plays a vital role in enhancing diabetes management and improving glycemic outcomes across the region.

When it comes to the overall market share, Blood Glucose Monitoring Devices dominated in 2024. Blood glucose meters and accompanying test strips are widely and cheaply available for daily blood sugar measurements. Glucose meters and test strips are recommended for patient use in both Type 1 and Type 2 diabetes, allowing them greater patient compliance for disease management.

Continuous glucose monitoring (CGM) devices will be the fastest-growing type of devices. The growth is due to the growing awareness surrounding CGM devices, improvements in accuracy, the growth of wearables for patients such as Abbott’s FreeStyle Libre, availability and access to wearables like CGM devices. The patient adoption of CGM devices is moving at the fastest pace, especially in Brazil and Mexico with urban patients who are looking for real-time monitoring devices.

Insulin Delivery Devices, such as insulin pens and insulin pumps, all have increasing penetration in the market. The convenience and control of smart pen devices and patch pumps have improved adoption amongst insulin delivery devices. The sub-segment of insulin pumps is projected to maintain modest growth with patient education development and reimbursement for devices developing in many countries.

Hospitals remain a leading channel, holding onto the bigger market share in 2024, as they are able to administer the entire continuum of diabetes care, including inpatient monitoring, insulin therapy initiation, and diabetes education. Large urban hospitals in particular are early adopters of advanced technologies such as CGMs (continuous glucose monitors) and insulin pumps.

Homecare settings are the most rapidly growing channel as patients desire to do monitoring and treatments at home. The COVID-19 pandemic facilitated the transition to home-care monitoring and diabetes education, and remote glucose monitoring technologies continue to grow. Retail pharmacies and online have also been expanding availability, particularly in blood glucose meters and insulin pens, enabling patients to self-manage their diabetes without a lot of clinical visits.

Diabetes clinics and diagnostic centers, especially in an urban areas that allow for specialty level care for chronic diabetes patients, will remain a key channel for long-term monitoring. These clinics are increasingly equipped with newer devices in facilitating remote monitoring and in individualizing therapy.

In 2024, Hospital Pharmacies held the largest market share due to high patient volumes in public and private hospital settings, combined with vehicles for continuing prescription-based diabetes management devices. Hospital pharmacies are also the primary supplier of insulin, syringes, and glucose meters for inpatients as well as patients that have just been discharged from a hospital admission.

Retail Pharmacies is the second largest market segment and provides access to easily obtained more commonly used diabetes device products like blood glucose meters, test strips, insulin pens and refills. In countries like Brazil and Mexico retail pharmacy chains such as Drogasil or Farmacias Guadalajara have increased their diabetes product portfolio, increasing accessibility for consumers. Online pharmacies show the highest growth opportunities as internet penetration, smartphone usage and e-commerce commitments spread across Latin America.

Online pharmacies are typically utilized more by younger patients or patients living in remote areas looking for devices and refills sent directly to their home. Diabetes Clinics or Specialty Stores also help with distribution, particularly for advanced devices like continuous glucose monitors (CGMs) and insulin pumps, as these devices typically require education and support by a professional.

In 2024, North America held the largest share of the market, or a 36.4% share. Growth in North America can be attributed to the presence of advanced health care systems, reporting of high prevalence of diabetes, and quicker uptake of CGM and insulin pump technology. Within North America, the U.S. reports the highest market shares, supported by reimbursement policies, technology dependent end consumers, and the existence of top manufacturers Medtronic, Abbott and Dexcom. Canada has also contributed to North America’s market share with coverage for large urban city dwellers receiving advanced endocrinology services.

Europe accounts for a 27.1% of the total share of the diabetes devices market in 2024. Growth in the European market is partly attributed to publically funded health systems, aging population, and high levels of awareness for diabetes management. Significant contributions come from Germany, the UK, France, and the Netherlands. The European Union initiatives related to chronic disease management and the increased utilization of digital health platforms also favour the uptake of devices, particularly CGMs and smart insulin pens.

The Asia-Pacific region is the fastest-growing market, forecasting a CAGR of 8.2% and having a current share of 21.6% in 2024. Rapid urbanized and income growth and an increase in diabetes rates are primarily in India, China, and Japan; are driving the growth of blood glucose monitors and insulin delivery devices. Government health programs, more people being insured with new coverage, and awareness campaigns all have contributed to making devices more accessible in urban and semi-urban areas.

The Latin America region accounted for 8.4% of the market in 2024, where Brazil and Mexico are the largest contributors. The Latin America region is experiencing moderate growth due to increases in diabetes rates and access to health care; however, barriers such as distribution of care, economic challenges, and affordability of devices for reimbursement are limiting widespread adoption of glucose monitors and advanced insulin delivery devices. Still, with the emerging telemedicine and digital health investments in the region, the diabetes care infrastructure continues to improve.

More established than growth; the Middle East and Africa (MEA) region accounts for 6.5% in the global market in 2024. Many countries are increasing investment in diabetes care programs such as Saudi Arabia, the UAE and South Africa are addressing lifestyle-related disease burden. Emerging programs are helping with access; however, even with regular access advanced devices are not reaching rural and low-income areas. There is growing usage and dependence on mobile health solutions and public-private partnerships that are gradually increasing the penetration of devices in the MEA region.

The market was valued at USD 18.58 billion in 2024.

The market is projected to grow at a CAGR of 7.48 % from 2025 to 2033.

The insulin delivery devices hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Abbott Laboratories, Medtronic plc and Roche Diabetes Care

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Brazil

5.2 Mexico

5.3 Argentina

5.4 Chile

5.5 Colombia

5.6 Rest of LATAM

6.1 Global Market Share (%) By Players

6.2 Market Ranking By Revenue for Players

6.3 Competitive Dashboard

6.4 Product Mapping