Medical Carts Market

Medical Carts Market Share & Trends Analysis Report, By Product (Mobile Computing Carts, Wall‑Mounted Workstations, Medication Carts, Storage Columns/Cabinets & Accessories, Other Carts), By Type (Use Case) (Anesthesia Carts, Emergency Carts, Procedure Carts, Telemedicine Carts, Other Types), By Material (Metal, Plastic, Wooden, Other Materials), By Configuration (Mobile (On‑Casters), Wall‑Mounted, Stationary), By End User (Hospitals, Ambulatory Surgical Centers, Physician Offices/Clinics, Nursing Homes, Home Healthcare, Other Settings)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

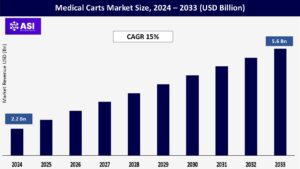

CAGR: 15%

Last Updated : January 21, 2026

The global medical carts market size was valued at approximately USD 2.2 billion in 2024 and is projected to reach USD 5.6 billion by 2033, growing at a CAGR of 15% during the forecast period (2025–2033).

The medical carts market revolves around mobile workstations that enable clinicians to move essential equipment, medications, and digital devices directly to the point of care. A typical cart blends a rugged, antimicrobial chassis—often powder-coated steel or molded ABS plastic—with smooth-rolling, lockable casters and height-adjustable columns so nurses, anesthesiologists, or emergency teams can wheel the cart to a bedside, ICU bay, or operating theatre and still maintain ergonomic posture.

Integrated battery packs or hot-swap power modules keep laptops, barcode scanners, and diagnostic peripherals running through a full shift, while modular drawers, slide-out trays, and accessory rails let hospitals reconfigure the same cart as a medication dispensing unit, a code-blue crash cart, or a procedure-specific supply hub.

Built-in RFID locks and tamper-evident seals protect controlled substances, and seamless work surfaces plus copper-infused or silver-ion coatings support infection-control protocols. Increasing EMR adoption pushes demand for carts that pair directly with hospital Wi-Fi, touchscreen PCs, and computerized physician-order-entry software, reinforcing their role as a linchpin of workflow efficiency and patient-safety initiatives.

A major driver for the medical carts market is the widespread adoption of Electronic Health Records (EHR) across hospitals and clinics, particularly in developed healthcare systems. As healthcare providers move towards digitized patient records for improved clinical decision-making and regulatory compliance, the need for point-of-care computing solutions has surged.

Medical carts integrated with computer systems allow nurses and physicians to input and access patient data directly at the bedside, reducing errors, enhancing documentation accuracy, and improving patient safety. This trend is particularly strong in North America and Europe, where government mandates and incentives have accelerated the integration of EHR systems into hospital workflows, positively influencing the medical carts market size.

As a result, demand for technologically advanced mobile workstations capable of supporting wireless connectivity, real-time data entry, and barcode scanning has significantly increased.

Another important driver is the growing pressure on healthcare institutions to improve operational efficiency and enhance patient safety, especially in high-volume and critical care environments. Medical carts streamline clinical workflows by minimizing the time staff spend retrieving supplies, medications, or equipment.

This allows healthcare workers to dedicate more time to patient care, which is particularly valuable amid ongoing nursing shortages and increased patient loads. Moreover, specialized carts such as anesthesia carts, crash carts, and isolation carts are designed to reduce contamination risks and comply with infection control protocols.

By optimizing task-specific mobility and standardizing equipment availability, these carts play a crucial role in reducing medical errors, preventing cross-contamination, and ensuring rapid response during emergencies, thereby strengthening their value proposition in modern healthcare settings.

A significant restraint in the medical carts industry is the high upfront cost associated with advanced carts, which can limit growth in the medical carts market size, especially those integrated with electronic systems, power supplies, and smart features like barcode scanners or touchscreen displays.

These technologically advanced medical carts can cost several thousand dollars each, making large-scale adoption a substantial financial burden for small- to mid-sized hospitals, outpatient centers, and clinics particularly in developing regions.

Beyond the purchase price, there are ongoing maintenance expenses, such as battery replacements, IT servicing, software updates, and part repairs, which further add to the total cost of ownership.

Moreover, institutions may require staff training to effectively operate integrated systems, adding to operational complexity and budget concerns. This cost sensitivity can delay procurement decisions or lead to the adoption of lower-end models that may lack critical features, thereby impeding market growth in cost-conscious healthcare settings.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product |

Mobile Computing Carts Wall‑Mounted Workstations Medication Carts Storage Columns/Cabinets & Accessories Other Carts |

| By Type (Use Case) |

Anesthesia Carts Emergency Carts Procedure Carts Telemedicine Carts Other Types |

| By Material |

Metal Plastic Wooden Other Materials |

| By Configuration |

Mobile (On‑Casters) Wall‑Mounted Stationary |

| By End User |

Hospitals Ambulatory Surgical Centers Physician Offices/Clinics Nursing Homes Home Healthcare Other Settings |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Medical Carts Market is segmented by Product, Type, Material, Configuration and End User. Each factor from the integration of electronic health records and power-assisted mobility to infection control features and modular design—plays a crucial role in improving clinical workflow efficiency, enhancing patient safety, and supporting the delivery of responsive, technology-enabled healthcare.

The market is led by mobile computing carts, which hold the largest medical carts market share due to their ability to integrate electronic health records (EHRs), diagnostic tools, and wireless communication systems at the point of care. These carts support real-time documentation, medication administration, and patient monitoring.

Wall-mounted workstations offer a space-saving alternative, especially in compact or high-traffic clinical environments such as ICU bays or outpatient exam rooms. Medication carts are specifically designed for secure drug storage and distribution, often incorporating locking drawers, barcode scanning, and tamper-evident systems.

Storage columns, cabinets, and accessories serve as fixed or semi-mobile storage solutions for bulk supplies, while other carts include specialized units for phlebotomy, ultrasound, or neonatal care.

The industry of medical carts is further divided based on functional specialization. Anesthesia carts are tailored for surgical settings and come equipped with drawers for anesthetics, monitors, and airway management tools. Emergency carts (crash carts) are essential in code-blue situations, offering quick access to defibrillators, emergency drugs, and life-saving instruments.

Procedure carts are used for wound care, minor surgeries, and routine tasks, ensuring that frequently used supplies are readily accessible. The rising use of telemedicine carts, particularly post-COVID-19, reflects the shift toward remote care; these are equipped with cameras, monitors, and connectivity tools to support virtual consultations. Other types include isolation carts and dialysis carts that meet specific infection control or patient treatment requirements.

Metal carts (usually aluminum or stainless steel) dominate the medical carts market due to their durability, corrosion resistance, and ease of disinfection, making them suitable for high-usage environments like operating rooms and ERs. Plastic carts (often made from ABS or polycarbonate) are lightweight and cost-effective, and their modularity makes them popular in outpatient and primary care settings.

Wooden carts, though limited in use, are preferred in long-term care and home healthcare for aesthetic appeal and patient comfort. The “other materials” category may include hybrid constructions and antimicrobial-coated materials designed to minimize infection risks.

Mobile (on-casters) carts represent the largest share, as they provide maximum flexibility and ease of movement between departments. These are essential in dynamic settings such as emergency departments and wards.

Wall-mounted units are ideal for areas where floor space is limited, offering a fixed yet accessible workstation. Stationary carts, often seen in operating rooms and labs, are designed to hold heavy or sensitive equipment and are usually more robust in build.

Hospitals account for the largest demand for medical carts due to their extensive infrastructure and multi-department workflows. Ambulatory surgical centers (ASCs) increasingly utilize procedure and anesthesia carts to support outpatient surgeries.

Physician offices and clinics typically opt for compact, versatile carts that assist in basic patient examination, documentation, and storage. Nursing homes benefit from medication and wooden carts that blend functionality with a home-like atmosphere.

Home healthcare providers use lightweight and mobile carts to carry essential supplies during patient visits. The other settings category includes rehabilitation centers, specialty diagnostic labs, and military field hospitals.

North America holds the largest share of the global medical carts market, driven by the region’s mature healthcare infrastructure, widespread adoption of electronic health records (EHR), and high emphasis on workflow efficiency and patient safety.

The U.S., in particular, is a leader in integrating mobile computing carts across hospital departments to support clinical documentation, barcode medication administration (BCMA), and mobile diagnostics.

Strong investments in healthcare IT, favorable reimbursement policies, and a high incidence of chronic diseases also contribute to the growing need for advanced medical cart systems. Additionally, increasing demand for telehealth and home healthcare has expanded the use of telemedicine carts and lightweight portable units across the region.

Europe represents the second-largest market share for medical carts, with strong growth fueled by ongoing healthcare digitization efforts, government investments in public health systems, and stringent safety standards. Countries like Germany, the UK, France, and the Nordics are at the forefront of adopting medical workstations that support paperless workflows and reduce medication errors.

European hospitals also prioritize infection control and ergonomics, making antimicrobial-coated, modular carts particularly popular. Budget constraints in certain Eastern and Southern European countries, however, may lead to more cautious procurement or reliance on mid-range cart models.

The Asia-Pacific region is emerging as the fastest-growing industry due to rapid healthcare infrastructure development, rising hospital admissions, and increasing adoption of mobile healthcare technologies.

Countries like China, India, Japan, and South Korea are investing heavily in modernizing their healthcare systems, creating new opportunities for mobile and stationary medical carts in both urban and rural healthcare facilities.

Local manufacturers in countries such as China and Taiwan are also producing cost-effective carts tailored for regional needs, contributing to competitive pricing and wider adoption.

In Latin America, market growth is driven by the modernization of healthcare facilities and the gradual shift toward digital documentation and improved patient safety protocols. Brazil, Mexico, and Argentina lead the adoption, particularly in larger hospitals and urban medical centers.

However, budget limitations and inconsistent infrastructure can hinder widespread use of high-end, IT-integrated carts. There is increasing interest in basic procedure carts and medication trolleys that offer modular storage and mobility without the added cost of electronics.

The Middle East & Africa region presents a mixed outlook. High-income countries in the Gulf Cooperation Council (GCC), such as the UAE and Saudi Arabia, are investing in world-class healthcare infrastructure, including smart hospitals that integrate advanced mobile workstations and telemedicine carts.

In contrast, many African nations still face limitations in funding, infrastructure, and trained personnel, restricting adoption to essential and cost-effective cart models primarily used in public hospitals and clinics.

The medical carts market was valued at USD 2.2 billion in 2024.

The medical carts market is projected to grow at a CAGR of 15% from 2025 to 2033.

The Mobile Computing Carts hold the largest market share.

The North America region is expected to witness the highest growth rate.

The Major players include Capsa Healthcare, Ergotron, Inc. and Harloff Manufacturing Co.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Medical Carts Market, By Product

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Medical Carts Market, By Type (Use Case)

5.3 Medical Carts Market, By Material

5.4 Medical Carts Market, By Configuration

5.5 Medical Carts Market, By End User

6.1 North America Medical Carts Market , By Country

6.1.1 Medical Carts Market, By Product

6.1.2 Medical Carts Market, By Type (Use Case)

6.1.3 Medical Carts Market, By Material

6.1.4 Medical Carts Market, By Configuration

6.1.5 Medical Carts Market, By End User

6.2 U.S.

6.2.1 Medical Carts Market, By Product

6.2.2 Medical Carts Market, By Type (Use Case)

6.2.3 Medical Carts Market, By Material

6.2.4 Medical Carts Market, By Configuration

6.2.5 Medical Carts Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping