Medical Devices Reimbursement Market

Medical Devices Reimbursement Market Share & Trends Analysis Report By Application (Diagnostic Devices, Therapeutic Devices, Surgical Devices, Home Healthcare Devices) By End-User (Hospitals & Clinics, Ambulatory Surgical Centers (ASCs), Home Healthcare Settings, Diagnostic Centers, Long-term Care Facilities) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 5.9%

Last Updated : March 7, 2026

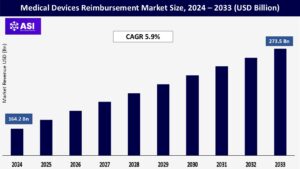

The global Medical Devices Reimbursement Market was valued at approximately USD 164.2 billion in 2024 and is projected to reach USD 273.5 billion by 2033, growing at a CAGR of 5.9% during the forecast period (2025–2033).

Medical device reimbursement is the process whereby healthcare entities collect compensation from a public or private funder for costs incurred in caring for a patient using a device. Reimbursement represents one of the most important means by which patients obtain access to, and treatment through, advanced medical technology. Reimbursement varies by region and payer, and is critical to the adoption and commercialization of new medical devices in the market.

Important market drivers include the increasing prevalence of chronic diseases such as diabetes, cardiovascular diseases, and cancers, increasing levels of healthcare spending by a healthcare system in transition, and a supportive public/private partnership to expand healthcare insurance coverage. Moreover, the rising rate of take-up of high-cost medical technology, particularly in minimally invasive and home-based care, is prompting stakeholders to revise and extend reimbursement regulations in markets across the world.

The increasing global burden of chronic diseases, such as diabetes, cancer, cardiovascular diseases, and chronic respiratory diseases, is driving demand for reimbursable medical devices. The World Health Organization (WHO) indicates that non-communicable diseases (NCDs) account for roughly 74% of global deaths, with cardiovascular diseases responsible for 17.9 million deaths each year.

Increased prevalence of these diseases necessitates continuous monitoring, diagnostic, and treatment devices—most of which can be associated with expensive medical devices, including continuous glucose monitors, insulin pumps, implantable cardiac defibrillator, and infusion pumps. Governments and insurers in both developed and developing countries are providing expanded reimbursement opportunities to improve equitable access to this life-saving technology.

For example, in 2023, India’s Ayushman Bharat scheme announced expanded reimbursement for implantable cardiac devices and orthopedic implants to reduce out-of-pocket spending for patients. Similarly, CMS has updated Medicare reimbursement codes to include continuous glucose monitors as a basic requirement for diabetic patient care. These developments in reimbursement policy are making medical devices more available and affordable, providing further momentum for the global reimbursement market.

The ongoing transition to value-based systems (e.g. reimbursement tied to outcomes and value) is changing how reimbursement is developed for devices. Volume-based reimbursement is being replaced by performance-based reimbursement, pushing device manufacturers to show real-world clinical and economic outcomes.

As the landscape changes and payers consider covering new devices, demonstrating improved patient outcomes (such as recovery timelines or decreased readmission) will continue to gain traction. A prime example is the U.S. 2024 Medicare Coverage of Innovative Technology (MCIT) rule, which will fast-track Medicare reimbursement for FDA-designated breakthroughs.

Existing devices such as portable dialysis and AI cardiac imaging, will be first in line for this new Medicare MCIT pathway. In the EU, medical device regulation (MDRs) has cultivated collaboration between device manufacturers and insurers around health technology analyses (HTA) to support coverage of devices that have high-value/cost effectiveness and clinically validated data. This regulatory structure supporting evidence-based reimbursement is broadening the landscape of covered devices. Around the world, this is paving the way for market growth.

A critical barrier in the global medical devices reimbursement space is the complexity and inconsistency of reimbursement policies between markets, and even between regions of the same market. Reimbursement mechanisms across both public and private payers are inconsistent and hard to navigate, creating a long approval and coverage process that prevents manufacturers from launching new products in a timely fashion, and taking away market access opportunities. For example, there are centralized healthcare systems in some countries where reimbursement is reasonably consistent with bureaucracy-laden policies of a single (sometimes rather bureaucratic) payer organization (e.g. the UK NHS).

However, other markets (like the US) operate under a multi-payer approach with different reimbursement criteria identified by several main payers, such as Medicare, Medicaid, and substantial private payer networks. As a consequence, a new product launch may take longer than intended, involve more than domestic administrative costs, and has a higher requirement for evidence and additional R&D efforts.

In addition to the inefficiencies for the medtech sector, many smaller and mid-size medtech companies struggle to obtain reimbursement approvals, therefore meaningful market access is simply much more delayed, and they have less access to connections and funding which can impede overall adoption of new and innovative technologies.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Application |

Diagnostic Devices Therapeutic Devices Surgical Devices Home Healthcare Devices

|

| By End-User |

Hospitals & Clinics Ambulatory Surgical Centers (ASCs) Home Healthcare Settings Diagnostic Centers Long-term Care Facilities |

| Key Players |

Medtronic plc Boston Scientific Corporation Abbott Laboratories Johnson & Johnson (DePuy Synthes, Ethicon) Stryker Corporation Zimmer Biomet Holdings, Inc. GE HealthCare Siemens Healthineers Koninklijke Philips N.V. Braun Melsungen AG Terumo Corporation Smith & Nephew plc Edwards Lifesciences Corporation Olympus Corporation Roche Diagnostics |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Medical Devices Reimbursement Market is segmented by application Type and End-User. Each segment plays a critical role in shaping the accessibility, affordability, and adoption of medical technologies worldwide.

The Diagnostic Devices segment accounted for the largest share of the genomics market in 2024 at 41.7%. This market share was supported by the need for early detection of diseases and preventive care. Diagnostic devices commonly used across care settings include MRI machines, CT scanners, PET systems, and IVD (in vitro diagnostic) kits. These devices are accepted as reimbursable services by public and private insurers.

With population burdens from chronic diseases growing in families and communities, payers are starting to include advanced diagnostics in their coverage plans. For example, Medicare’s coverage of cancer screening for patients using genomic-based diagnostic tests. This growth is contributing to increased demand in the Diagnostic Devices segment. The Therapeutic Devices segment will grow at a CAGR of almost 6.8% through 2033 due to the increases in the adoption rates of high-value devices, such as implantable cardiac defibrillators, insulin pumps, and neurostimulators.

These devices are important to address long-term chronic disease schedules and are eligible for reimbursement by both government and private insurance plans. For example, the NHS in the U.K. provides full reimbursement for the deep brain stimulation systems prescribed for treating Parkinson’s, contributing to demand across Europe.

In addition, Surgical devices, which includes robotic surgical systems, endoscopic devices, and energy-based devices, are increasingly included in reimbursement plans, especially for minimally invasive procedures. As value-based care continues to expand and payers reimbursing surgical success rather than surgeon fees, new technologies for precision surgical approaches are becoming optional for many hospitals.

Home Healthcare Devices are also proving to be the fasted growing area of medical devices due the global movement to Remote Patient Monitoring and aging-in-place care models. Many devices, such as portable oxygen concentrators, glucose monitors, CPAP devices, and mobile ECG devices are also being reimbursed more frequently as methods to reduce emergency visits and increase patient quality of life. For instance, in the United States, following COVID, CMS increased reimbursement for Remote Patient Monitoring tools which has accelerated growth in this area.

The largest market share of 53.4% was attributed to Hospitals & Clinics in 2024 since most high-cost reimbursed devices (i.e., implantable cardiac defibrillators, orthopedic implants, and imaging systems) are deployed in this setting. Hospitals routinely interact with both public and private payers to obtain reimbursements; in particular, inpatient and surgical reimbursements are particularly focused on. More recently, the growth of multispecialty and super-specialty hospitals is also contributing to segment growth.

The segment of Ambulatory Surgical Centers (ASCs) is growing rapidly to meet the demand for outpatient procedures that involve reimbursed devices (e.g., laparoscopic tools, endoscopes, and implanted minimally invasive devices). ASCs have demonstrated faster approval timelines for insurance, and ultimately offer better value to payers, physicians, and patients through faster and less expensive care delivery.

Home Healthcare Settings are an increasingly important segment as the effort to coordinate care through remote patient monitoring and manage chronic disease continues to increase. Devices (e.g., portable oxygen concentrators, wearable ECG monitors and smart infusion pumps) are increasingly being reimbursed through long-term care contracts.

The Centers for Medicare & Medicaid Services (CMS) and other insurers have also begun expanding reimbursement codes for remote monitoring equipment to minimize hospital readmissions. They’re also a driver of growth for the market and will continue to grow as reimbursements expand for preventive screenings and long-term, continuous care devices. The continued push for early diagnosis and value-based care provides these settings with greater access to technologies with reimbursement.

North America held the largest share of the medical devices reimbursement market at 41.2% in 2024, due to a long-standing healthcare reimbursement system and deeper insurance penetration. The United States was the most significant player in the region with a large number of publicly funded healthcare programs such as Medicare and Medicaid; many private health insurers also provide coverage in some capacity for various medical devices.

The reimbursement policies are also expanding for newer advanced medical devices such as robotic surgical systems, continuous glucose monitors (CGMs), and remote monitoring and other disruptive technologies. Additionally, Canada’s publicly funded provincial health systems further address provincially funded health care system reimbursements of medically necessary devices. Collectively, both systems contribute to the firm position of North America in the medical devices reimbursement market.

Europe contributes considerably to the landscape of the overall market, with Germany, UK, France, and the Netherlands leading the way as there are strong public insurance schemes and Health Technology Assessment (HTA) frameworks that support reimbursement by the public health system. In Germany, for example, statutory health insurance (SHI) covers numerous high-cost devices, including orthopedic implants and many cardiac devices.

The evolution of the region will continue to be driven by an aging population, developing digital health infrastructure, and increasing early adoption of innovative homecare technologies. The European Union (EU) is also now establishing Medical Device Regulation (MDR); every manufacturer must show choices are safe and cost-effective, which corresponds with payers’ demands for evidence-based reimbursement.

The Asia-Pacific region is expected to attain the fastest CAGR of 7.6% during the forecast period, thanks to increased healthcare expenditures, greater insurance coverage, and healthcare system reforms occurring in China, India, Japan, and South Korea. Specifically, China has started to include more devices in its National Reimbursement Drug List (NRDL) and make these devices eligible for public insurance coverage.

In India, the low-income segments can now even access implants and diagnostic devices with the Ayushman Bharat scheme. Japan has great universal health coverage and a rapidly aging population, with more home healthcare and monitoring devices being included in its reimbursement. These trends will improve access and uptake of medical technologies throughout the region.

Latin America and the Middle East & Africa (MEA) regions are experiencing moderate growth aided by continuing improvements in healthcare infrastructure and access to health insurance. Brazil, Mexico, Saudi Arabia, and South Africa are active participants, where public health programs are starting to include sophisticated diagnostics and therapeutic devices within their reimbursement programs.

More specifically, there is a good amount of economic inequality, limited insurance coverage, and regulatory frameworks are often fragmented. These hurdles notwithstanding, the growing burden of disease, investment in healthcare from outside the region, and public-private partnerships are slowly widening reimbursement access and increasing affordability for patients.

The market was valued at USD 164.2 billion in 2024.

The market is projected to grow at a CAGR of 5.9% from 2025 to 2033.

The public payers hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Medtronic plc, Boston Scientific Corporation, Abbott Laboratories.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Medical Devices Reimbursement Market, By Application

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Medical Devices Reimbursement Market, By End-User

6.1 North America Medical Devices Reimbursement Market , By Country

6.1.1 Medical Devices Reimbursement, By Application

6.1.2 Medical Devices Reimbursement, By-End User

6.2 U.S.

6.2.1 Medical Devices Reimbursement, By Application

6.2.2 Medical Devices Reimbursement, By-End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping