Medical Oxygen Concentrators Market

Medical Oxygen Concentrators Market Share & Trends Analysis Report, By Product Type (Portable Oxygen Concentrators (POCs), Stationary Oxygen Concentrators (Fixed Oxygen Concentrators)), By Technology Type (Continuous Flow Oxygen Concentrators, Pulse Dose Oxygen Concentrators (On-Demand Flow)), By Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Sleep Apnea, Respiratory Distress Syndrome (RDS), Pneumonia, Cystic Fibrosis, Other Respiratory Conditions), By End-User (Homecare Settings, Hospitals & Clinics, Ambulatory Surgical Centers (ASCs) & Physician Offices) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

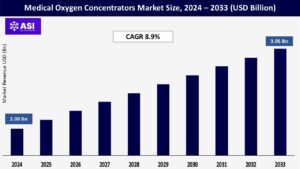

CAGR: 8.9%

Last Updated : March 27, 2026

The global medical oxygen concentrators market size was valued at approximately USD 2.08 billion in 2024 and is projected to reach USD 3.05 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 8.9% during the forecast period of 2025–2033.

The medical oxygen concentrators market plays a crucial role in the healthcare industry and is seeing strong growth. This is largely driven by the rising number of people with respiratory diseases, an aging population that needs more support for conditions like COPD, and a growing preference for receiving care at home. As these needs increase, the market is evolving to offer more advanced, portable, and user-friendly oxygen therapy solutions. These improvements aim to make respiratory care more accessible and effective for patients all over the world.

The demand for medical oxygen concentrators is being driven by several important factors. First, chronic respiratory conditions like COPD, asthma, cystic fibrosis, sleep apnea, and idiopathic pulmonary fibrosis are becoming more common worldwide. COPD alone is one of the leading causes of death, affecting millions and often requiring long-term oxygen therapy to help patients manage their symptoms and maintain a better quality of life. Environmental factors also play a big role.

Air pollution, rising smoking rates, and occupational hazards all contribute to the development and worsening of respiratory illnesses, further increasing the need for reliable oxygen therapy solutions. Additionally, the COVID-19 pandemic created a huge surge in demand for oxygen therapy. Even as the immediate crisis has eased, many patients are still dealing with long-term respiratory complications like lung fibrosis, especially in home care settings. This ongoing need has cemented oxygen concentrators as an essential part of respiratory care for many people around the world.

Several important factors are helping drive the growth of the medical oxygen concentrators market. Around the world, governments are investing more in strengthening healthcare infrastructure, especially in emerging economies. This includes buying and distributing essential medical equipment like oxygen concentrators to make sure hospitals and clinics are better prepared to meet patient needs.

Public health campaigns are also playing a key role by raising awareness about respiratory health and the benefits of oxygen therapy. These initiatives help people get diagnosed earlier and understand their treatment options, which in turn increases demand for concentrators. Improving reimbursement policies and government subsidies for home oxygen therapy are making these devices more affordable and accessible for patients in many countries, further boosting market growth.

While strict regulations can sometimes slow things down, there’s also strong regulatory support for expanding access. For example, during the COVID-19 pandemic, many governments issued emergency use authorizations to speed up availability. In other cases, specific guidelines like allowing portable oxygen concentrators (POCs) on flights have helped make these devices easier for patients to use in their everyday lives.

One of the biggest challenges with medical oxygen concentrators is their high upfront cost. Advanced stationary or portable models can cost anywhere from a few hundred to several thousand US dollars. For many people, especially in low- and middle-income countries, this kind of expense is simply out of reach. In addition, reimbursement policies for home oxygen therapy aren’t always robust or even available in many places. Without comprehensive coverage, patients often have to pay most or all of the cost themselves, making access even more difficult. It’s not just the initial price, either. There are ongoing costs for things like replacing filters, routine maintenance, and repairs, all of which can add up over time. These expenses create a significant financial burden for patients and can also strain healthcare systems trying to make these essential devices more widely available.

One of the key challenges with oxygen concentrators is their need for a constant and reliable power supply. In areas with frequent power outages or unstable electrical grids, especially in rural or remote regions, this can be a serious obstacle to consistent treatment. Patients may worry about whether they’ll have access to oxygen when they need it most. Even portable oxygen concentrators (POCs), which are designed for mobility, have their limitations. Their batteries only last so long before needing a recharge, which can be inconvenient for patients who are very active or who live in places where charging options or backup power aren’t readily available.

Power failures can be particularly dangerous for people who rely on stationary concentrators at home. Without alternative oxygen sources like backup cylinders or generators, these outages can lead to life-threatening situations, causing significant anxiety for patients and their families and increasing the risk of serious health complications.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Portable Oxygen Concentrators (POCs) Stationary Oxygen Concentrators (Fixed Oxygen Concentrators) |

| By Technology Type |

Continuous Flow Oxygen Concentrators Pulse Dose Oxygen Concentrators (On-Demand Flow) |

| By Application |

Chronic Obstructive Pulmonary Disease (COPD) Asthma Sleep Apnea Respiratory Distress Syndrome (RDS) Pneumonia, Cystic Fibrosis Other Respiratory Conditions |

| By End-User |

Homecare Settings Hospitals & Clinics Ambulatory Surgical Centers (ASCs) & Physician Offices |

| Key Players |

Koninklijke Philips N.V. (Philips Respironics) Inogen, Inc. Invacare Corporation Drive DeVilbiss Healthcare LLC (Drive DeVilbiss International) CAIRE Inc. (a Chart Industries company) ResMed Inc. GCE Group O2 Concepts LLC Nidek Medical Products, Inc. Niterra Co., Ltd. (formerly NGK Spark Plug Co., Ltd., which owns CAIRE) Besco Medical Co. Ltd. React Health Jiangsu Yuyue Medical Equipment & Supply Co., Ltd. (Yuwell) Longfian Scitech Co., Ltd. OxyGo LLC BPL Medical Technologies (primarily India-focused) Oxymed (primarily India-focused) Teijin Limited |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Medical Oxygen Concentrators Market is categorized by product type, by technology, by application, and by end-user. Each segment provides a comprehensive understanding of its dynamics and growth opportunities. The Medical Oxygen Concentrators Market is segmented in various ways to provide a detailed understanding of its dynamics, consumer preferences, and operational aspects.

Medical oxygen concentrators come in two main types based on how and where they’re used: portable and stationary models. Portable Oxygen Concentrators (POCs) are lightweight, compact, and battery-powered, giving patients the freedom to move around while still receiving their oxygen therapy. Whether it’s going to work, traveling, or simply running errands, these devices make it easier for patients to maintain an active lifestyle.

Thanks to ongoing technological advancements like smaller designs, longer battery life, and even FAA approval for air travel, POCs have become increasingly popular, especially among people who don’t want to be confined to one place. As a result, this segment is growing rapidly and is often favored over traditional stationary units or bulky oxygen tanks for those on the go.

On the other hand, Stationary Oxygen Concentrators are larger and designed for use in one location, typically at home or in a healthcare facility. They plug into a wall outlet and deliver a continuous flow of oxygen, making them ideal for patients who need round-the-clock therapy, such as the elderly or bedridden individuals. Despite their size, these units remain the most widely used, holding a larger share of the market (over 50% as of 2023). That’s largely because they’re more cost-effective for long-term use and essential for managing chronic respiratory conditions that require consistent, high-volume oxygen delivery.

Oxygen concentrators can also be classified based on how they deliver oxygen to patients. Continuous Flow Oxygen Concentrators provide a steady, uninterrupted stream of oxygen at a set rate (measured in liters per minute), regardless of how the patient is breathing. This makes them especially important for people with severe, long-term respiratory conditions like COPD, asthma, or bronchiectasis, where consistent oxygen delivery is essential. Because of this critical role, continuous flow models hold the largest share of the market, over 56% as of 2023, and are commonly used in hospitals as well as in home settings for patients who need reliable, round-the-clock therapy.

Pulse Dose Oxygen Concentrators, on the other hand, are designed to be more efficient. They sense when the patient inhales and deliver a precise “pulse” of oxygen only at that moment, which helps conserve oxygen and extend battery life. This technology is especially popular in portable models, making them ideal for active users who want more freedom and flexibility without sacrificing treatment quality. As demand for portable oxygen solutions grows, this segment is expected to see the fastest growth in the coming years, with a projected annual growth rate of around 5.5%.

The medical oxygen concentrators market can also be broken down based on the specific health conditions they’re used to treat. Chronic Obstructive Pulmonary Disease (COPD) is the biggest application area, making up the largest share of the market (around 42% in 2023). COPD is a group of progressive lung diseases that make it hard to breathe by blocking airflow. For many patients, oxygen therapy is a vital, long-term part of managing the disease and improving quality of life.

Asthma is another important use case. While daily management often relies on inhalers, severe asthma attacks can lead to dangerous drops in blood oxygen levels, requiring supplemental oxygen in emergency settings. Sleep Apnea is a disorder where breathing repeatedly stops or becomes very shallow during sleep.

While CPAP and BiPAP machines are standard treatments, oxygen therapy may be added in certain cases to help maintain safe oxygen levels overnight. Respiratory Distress Syndrome (RDS) mainly affects newborns, especially premature babies with underdeveloped lungs. Oxygen therapy is critical for helping them breathe properly in neonatal care units. Pneumonia, a lung infection that can fill air sacs with fluid or pus, often requires oxygen therapy in severe cases to ensure patients get enough oxygen while their lungs heal.

Cystic Fibrosis, a genetic condition that severely damages the lungs and other organs, can also necessitate oxygen therapy as lung function declines. Finally, other respiratory conditions, including pulmonary fibrosis, emphysema, lung cancer, and complications from infectious diseases like COVID-19, can lead to significant breathing problems that require oxygen therapy. All of these diverse applications highlight why oxygen concentrators are such an essential part of modern respiratory care.

The medical oxygen concentrators market can also be understood by looking at where these devices are most often used. Homecare settings represent the largest and fastest-growing segment, accounting for more than 60% of the market in 2023. More and more patients are managing their respiratory conditions at home, using both stationary units for continuous overnight oxygen and portable models for greater freedom during daily activities. This shift toward home-based care is being driven by a desire for greater patient comfort, cost savings compared to long hospital stays, and continuous improvements in easy-to-use, reliable home devices.

Hospitals and clinics remain essential users of oxygen concentrators as well. These facilities rely on them for critical care, emergency oxygen delivery, post-operative recovery, and the treatment of patients with acute respiratory conditions during their stay. Because hospitals and clinics are central points for diagnosis and ongoing care, they account for a significant share of the market.

Ambulatory surgical centers (ASCs) and physician offices also use oxygen concentrators, though for more specific needs. They provide immediate oxygen support during minor surgical procedures, diagnostic tests, and patient consultations, and they help manage recovery for those who have undergone short-term procedures. This wide range of settings highlights how oxygen concentrators have become a critical part of respiratory care across the entire healthcare landscape.

The medical oxygen concentrators market shows different trends across regions, shaped by local healthcare systems, economic conditions, and the burden of respiratory diseases. North America and Europe currently lead the market, thanks to their well-established healthcare infrastructure, widespread access to medical technology, and high rates of respiratory conditions like COPD and sleep apnea.

Meanwhile, the Asia-Pacific region is emerging as the fastest-growing market. With its large and growing population, rising cases of chronic respiratory illnesses, and ongoing investments in healthcare infrastructure, countries like China, India, and Southeast Asian nations are seeing a sharp increase in demand for oxygen concentrators. Though currently smaller in size, Latin America and the Middle East & Africa (MEA) are also showing strong potential.

As these regions continue to expand their healthcare services and improve access to medical equipment, the market for oxygen concentrators is expected to grow steadily. Overall, each region presents unique opportunities and challenges, but the global need for accessible, reliable respiratory care continues to rise across the board.

North America consistently holds the largest share of the global medical oxygen concentrators market, accounting for roughly 32% to over 41% of market revenue in 2024, depending on the source. This dominant position is driven by several key factors. The region faces a high prevalence of respiratory diseases such as COPD, asthma, and sleep apnea, with contributing factors including an aging population, lifestyle habits like smoking, and environmental challenges. The need to manage these chronic conditions ensures steady demand for oxygen therapy.

North America also benefits from a highly advanced healthcare infrastructure. The U.S. and Canada have well-developed medical systems with substantial healthcare spending and a strong emphasis on chronic disease management and home-based care. There’s also a notable openness to adopting advanced medical technologies. Both patients and healthcare providers readily embrace innovations like portable and smart oxygen concentrators, which improve quality of life and support better disease management.

Another important factor is favorable reimbursement policies. Programs like Medicare in the U.S. offer robust coverage for home oxygen therapy, making these devices more affordable and accessible to patients. Additionally, many of the world’s leading manufacturers of oxygen concentrators are either based in North America or have significant operations there, helping to drive continuous R&D and expand market reach.

The United States stands out as the largest market in the region, followed by Canada. Current trends include ongoing innovation in portable devices, better integration with digital health platforms for remote monitoring, and a growing focus on user-friendly designs and energy-efficient technology.

Europe is the second-largest market for medical oxygen concentrators and is expected to see steady growth in the coming years. Some projections estimate a CAGR of around 12.2% for the broader oxygen concentrator market between 2024 and 2030. Several factors are driving this growth. Europe’s aging population is especially important because older adults are more prone to chronic respiratory diseases like COPD and pulmonary fibrosis, which often require long-term oxygen therapy to manage symptoms and maintain quality of life.

The region also benefits from robust healthcare systems, both public and private, with significant healthcare spending that supports the adoption of advanced medical devices. Many European countries are increasingly promoting home-based care to reduce hospital stays and offer patients a more comfortable, familiar setting for managing chronic conditions.

There’s also a growing awareness among both patients and healthcare professionals about the benefits of newer, more advanced oxygen therapy options. Europe is home to a strong base of medical device innovation, helping ensure a steady pipeline of improved, user-friendly products. Germany leads the European market, thanks to its large elderly population and advanced healthcare infrastructure. Other major markets include the UK, France, and Italy. However, varying reimbursement policies across different countries can pose a challenge, sometimes creating differences in how easily patients can access and afford these essential devices.

The Asia-Pacific region is expected to be the fastest-growing market for medical oxygen concentrators worldwide. While estimates for growth rates vary, the entire medical oxygen systems market in this region is projected to expand rapidly in the coming years. Several important factors are driving this growth. First, countries like China and India have huge and still growing populations. Along with that, they face a rising burden of respiratory diseases, fueled by urbanization, industrial pollution, and lifestyle changes.

This combination creates a large, unmet need for reliable oxygen therapy. Healthcare infrastructure across the region is also improving quickly. Governments and private companies are making major investments to modernize hospitals and clinics, especially in emerging economies. At the same time, rising disposable incomes in countries like China and India mean more people can now afford advanced medical devices, including oxygen concentrators.

There’s also a noticeable increase in public awareness about respiratory health and a push to improve access to essential medical equipment. The growth of local manufacturers in countries like China and India is helping address supply chain issues and reduce costs, making these devices more accessible to broader segments of the population. China is expected to lead the Asia-Pacific market, thanks to its sheer population size and the rapidly growing need for respiratory care. India is also projected to see substantial growth, driven by similar factors and a rising demand for home healthcare solutions.

Meanwhile, Japan, South Korea, and Australia represent mature markets with high rates of adoption of advanced concentrator technologies. However, there are still challenges to overcome. Affordability remains a major barrier for many people in the region, and reliable electricity access, especially in rural areas, can limit the use of electric concentrators.

The Middle East and Africa (MEA) region is considered a developing market for medical oxygen concentrators, with significant growth potential, especially in the Gulf Cooperation Council (GCC) countries. A key driver is the high incidence of respiratory diseases in many parts of the region. Conditions like diabetes (which can increase vulnerability to respiratory issues) are widespread and often worsened by environmental factors and lifestyle choices.

Healthcare systems in the MEA are also rapidly modernizing. Oil-rich GCC nations, in particular, are making major investments to upgrade hospitals and clinics and adopt advanced medical technologies, boosting demand for reliable oxygen therapy solutions. Rising disposable incomes in wealthier parts of the region have increased people’s ability to afford medical devices, while public health campaigns are helping raise awareness about the importance of respiratory health and early treatment.

Saudi Arabia and the UAE are the leading markets in the Middle East, thanks to strong government support for healthcare investment and a focus on delivering high-quality medical services. In sub-Saharan Africa, South Africa stands out as a key market with relatively better infrastructure and demand. However, there are still important challenges. Political instability in certain countries, uneven access to healthcare services, and affordability issues, especially in less developed African nations, can limit the widespread adoption of medical oxygen concentrators in parts of the region.

The market was valued at USD 2.08 billion in 2024.

The market is projected to grow at a CAGR of 8.9% from 2025 to 2033.

Home care segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include Koninklijke Philips N.V., ResMed, Inogen, Drive DeVilbiss Healthcare, and CAIRE Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Medical Oxygen Concentrators Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Medical Oxygen Concentrators Market, By Technology Type

5.3 Medical Oxygen Concentrators Market, By Application

5.4 Medical Oxygen Concentrators Market, By End-Users

6.1 North America Medical Oxygen Concentrators Market, By Country

6.1.1 Medical Oxygen Concentrators Market, By Product Type

6.1.2 Medical Oxygen Concentrators Market, By Technology Type

6.1.3 Medical Oxygen Concentrators Market, By Application

6.1.4 Medical Oxygen Concentrators Market, By End-Users

6.2 U.S.

6.2.1 Medical Oxygen Concentrators Market, By Product Type

6.2.2 Medical Oxygen Concentrators Market, By Technology Type

6.2.3 Medical Oxygen Concentrators Market, By Application

6.2.4 Medical Oxygen Concentrators Market, By End-Users

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping