Medical Protective Equipment Market

Medical Protective Equipment Market Share & Trends Analysis Report, By Product Type (Surgical Masks, N95/Respirators, Gloves (Examination/Surgical), Gowns & Protective Clothing, Face Shields & Goggles, Head Covers, Shoe Covers, Other PPE), By Usability (Disposable PPE, Reusable PPE), By End User( Hospitals & Clinics, Ambulatory Surgical Centers, Diagnostic & Research Laboratories, Government Agencies & NGOs, Home Healthcare, Other End Users), By Material Type( Latex, Nitrile, Polypropylene, Rubber, Fabric, Plastic, Antimicrobial Textiles, Others), By Application ( Infection Control, Hazardous Material Handling, Surgical & Procedural Protection, Patient Care & Trauma Response, Lab & Research Use)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

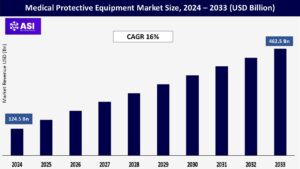

CAGR: 16%

Last Updated : December 15, 2025

The global Medical Protective Equipment Market size was valued at approximately USD 124.5 billion in 2024 and is projected to reach USD 462.5 billion by 2033, growing at a CAGR of 16% during the forecast period (2025–2033).

The Medical Protective Equipment Market encompasses a broad range of personal protective products that are essential for ensuring safety and hygiene in medical environments. This market includes items such as face masks, gloves, surgical gowns, face shields, goggles, head covers, shoe covers, and respirators.

These products are used by healthcare professionals, laboratory technicians, and patients to prevent exposure to infectious agents, harmful chemicals, and other hazards, especially during surgical procedures, patient care, and outbreak situations like pandemics.

The use of medical protective equipment is critical in reducing cross-contamination, maintaining sterile environments, and ensuring the safety of both medical staff and patients. Key properties of medical protective equipment include its barrier effectiveness against fluids and pathogens, durability, breathability, and comfort for extended use.

The materials used are often non-woven fabrics like polypropylene for masks and gowns, nitrile or latex for gloves, and high-impact plastic like polycarbonate for face shields.

Many of these products are designed to be disposable to ensure hygiene and infection control, though some high-grade protective gear may be reusable after proper sterilization. Compliance with regulatory standards such as FDA, CE, and ISO certifications is essential for all products in this category.

The COVID-19 pandemic highlighted the critical need for personal protective equipment (PPE) in preventing the transmission of infectious diseases. Even after the pandemic, heightened awareness about infection control continues to drive demand in hospitals, clinics, labs, and even public spaces.

Governments, institutions, and businesses are maintaining stockpiles of protective gear, and regulations mandating the use of PPE in healthcare settings remain stringent, ensuring consistent market growth.

With global healthcare infrastructure expanding especially in emerging economies there is a continuous rise in medical and surgical procedures, which require large quantities of sterile protective equipment.

The growing number of healthcare professionals, patients, and diagnostic and surgical activities is driving the need for high-quality gloves, gowns, face masks, and shields. Additionally, the increase in outpatient care, home healthcare services, and mobile clinics further boosts the demand for disposable and reusable protective gear.

The fluctuation in raw material costs particularly for materials like polypropylene (used in masks and gowns), latex, nitrile, and polycarbonate poses a major restraint in the medical protective equipment market. During times of global crises, such as the COVID-19 pandemic, supply chains were heavily disrupted, leading to shortages and price spikes for essential components.

This volatility impacts manufacturing costs, product availability, and profit margins, especially for small and mid-sized manufacturers. Furthermore, reliance on international suppliers for key materials increases vulnerability to trade restrictions, logistic delays, and geopolitical instability.

These challenges can lead to inconsistent supply, higher end-user prices, and decreased accessibility in price-sensitive or remote markets.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Surgical Masks N95/Respirators Gloves (Examination/Surgical) Gowns & Protective Clothing Face Shields & Goggles Head Covers Shoe Covers Other PPE |

| By Usability |

Disposable PPE Reusable PPE |

| By End User |

Hospitals & Clinics Ambulatory Surgical Centers Diagnostic & Research Laboratories Government Agencies & NGOs Home Healthcare Other End Users |

| By Material Type |

Latex Nitrile Polypropylene Rubber Fabric Plastic Antimicrobial Textiles Others |

| By Application |

Infection Control Hazardous Material Handling Surgical & Procedural Protection Patient Care & Trauma Response Lab & Research Use |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Medical Protective Equipment Market is segmented by Product Type, Usability, End User, Material Type and Application. Rising global emphasis on infection control, expanding healthcare infrastructure, and heightened pandemic preparedness have collectively reinforced the critical role of medical protective equipment in safeguarding both healthcare workers and patients.

These drivers contribute to the widespread adoption of high-quality protective solutions, fostering the development of safer clinical environments and strengthening resilience across health systems worldwide.

Surgical Masks, N95/Respirators, Gloves (Examination/Surgical), Gowns & Protective Clothing, Face Shields & Goggles, Head Covers, Shoe Covers, and Other Personal Protective Equipment (PPE). Surgical masks and N95 respirators dominate the market due to their critical role in preventing airborne infections, especially in surgical settings and during outbreaks like COVID-19.

Gloves, both examination and surgical, form an essential part of infection prevention protocols and hold a large market share across all healthcare settings. Gowns and protective clothing are vital during high-risk procedures, surgeries, and infectious disease management, especially in hospitals and isolation units.

Face shields and goggles are primarily used to protect against splashes, sprays, and respiratory droplets, particularly in operating rooms and laboratories. Head and shoe covers, though smaller in market size, are essential in maintaining sterile environments in surgical theaters and cleanrooms. The other PPE category includes aprons, arm covers, and specialty protection gear used in specialized labs or emergency response units.

The market is classified into Disposable PPE and Reusable PPE. Disposable PPE holds the majority share owing to its widespread use in infection control, convenience, and compliance with hygiene protocols that prevent cross-contamination. It is particularly prevalent in emergency settings, outpatient care, and infectious disease management.

Reusable PPE, on the other hand, is gaining traction in environments where environmental sustainability, cost control, and long-term use are priorities. Hospitals and labs often invest in reusable gowns, face shields, and protective eyewear that can be sterilized and reused multiple times without compromising safety.

The market is segmented into Hospitals & Clinics, Ambulatory Surgical Centers (ASCs), Diagnostic & Research Laboratories, Government Agencies & NGOs, Home Healthcare, and Other End Users. Hospitals and clinics are the largest end users due to their extensive use of PPE in surgical procedures, patient care, and infection control.

ASCs are rapidly adopting PPE due to the rising number of outpatient surgeries and minor procedures. Diagnostic and research laboratories require high-quality protective gear for biohazard handling and contamination prevention during testing and research.

Government agencies and NGOs, particularly during pandemics or natural disasters, play a significant role in distributing and using PPE for public safety and frontline healthcare workers.

Home healthcare is a growing segment as patients receive treatments like wound care, dialysis, or respiratory therapy at home, necessitating basic protective gear. The other end users segment includes academic institutions, nursing homes, and industrial healthcare settings.

The market includes Latex, Nitrile, Polypropylene, Rubber, Fabric, Plastic, Antimicrobial Textiles, and Others. Nitrile and latex dominate the gloves segment due to their superior fit, flexibility, and protection against pathogens.

Polypropylene, a lightweight nonwoven fabric, is widely used in the manufacture of masks, gowns, and caps due to its breathability, filtration efficiency, and cost-effectiveness. Rubber and plastic are common in the manufacture of reusable PPE like goggles, face shields, and shoe covers.

Fabric materials, both disposable and reusable, are used for gowns and drapes in surgical environments. The increasing adoption of antimicrobial textiles—materials embedded with silver, copper, or other agents to actively kill or inhibit pathogens—is driving innovation and providing added layers of protection in high-risk settings.

The others category includes advanced composite materials and smart textiles being developed for next-generation protective solutions.

The market is segmented into Infection Control, Hazardous Material Handling, Surgical & Procedural Protection, Patient Care & Trauma Response, and Lab & Research Use. Infection control is the largest segment, fueled by global awareness post-pandemic and strict hospital-acquired infection (HAI) protocols.

Hazardous material handling includes use in labs, chemical handling units, and waste management departments where exposure to biological or toxic substances is a risk. Surgical and procedural protection accounts for a large portion of PPE used in sterile environments during operations and invasive diagnostics.

Patient care and trauma response relies on protective equipment for emergency responders, paramedics, and home caregivers. Lab and research use demands specialized PPE designed to withstand chemical exposure, provide barrier protection, and ensure accuracy during diagnostic or pharmaceutical research work.

Continues to lead the medical protective equipment market, largely due to high healthcare spending, strict infection control protocols, and preparedness for public health emergencies.

The U.S. has heavily invested in stockpiling PPE post-COVID-19 and maintains strong domestic production and regulation, ensuring consistent market demand.

Also holds a substantial share, driven by strong regulatory standards (such as CE marking), universal healthcare access, and high awareness of occupational safety in clinical settings. Countries like Germany, France, and Italy are notable consumers of advanced protective gear.

Region, rapid industrialization, increased healthcare investment, and pandemic preparedness initiatives have accelerated demand. China and India are significant producers and exporters of PPE, while Japan, South Korea, and Southeast Asian countries are investing in quality upgrades and healthcare infrastructure.

Shown increasing demand, especially in countries like Brazil, Argentina, and Chile, due to the region’s focus on infection control and public health improvements. However, supply chain limitations and economic constraints remain challenges.

Demand is growing in urban centers and private healthcare facilities, with countries like the UAE and South Africa leading the way. Public sector healthcare programs and support from global NGOs continue to help improve access to essential protective equipment in lower-income areas.

The market was valued at USD 124.5 billion in 2024.

The market is projected to grow at a CAGR of 16% from 2025 to 2033.

Surgical Masks hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include 3M Company, Honeywell International Inc. and Kimberly-Clark Corporation

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Medical Protective Equipment Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Medical Protective Equipment Market, By Usability

5.3 Medical Protective Equipment Market, By End User

5.4 Medical Protective Equipment Market, By Material Type

5.5 Medical Protective Equipment Market, By Application

6.1 North America Medical Protective Equipment Market , By Country

6.1.1 Medical Protective Equipment Market, By Product Type

6.1.2 Medical Protective Equipment Market, By Usability

6.1.3 Medical Protective Equipment Market, By End User

6.1.4 Medical Protective Equipment Market, By Material Type

6.1.5 Medical Protective Equipment Market, By Application

6.2 U.S.

6.2.1 Medical Protective Equipment Market, By Product Type

6.2.2 Medical Protective Equipment Market, By Usability

6.2.3 Medical Protective Equipment Market, By End User

6.2.4 Medical Protective Equipment Market, By Material Type

6.2.5 Medical Protective Equipment Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping