Nanosatellite and Microsatellite Market

Nanosatellite and Microsatellite Market Size, Market Share & Trends Analysis Report By Type (Nanosatellites, Microsatellites), By End-Use (Commercial, Government & Military, Academic & Research), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIADR1014

CAGR: 12.3%

Last Updated : April 28, 2026

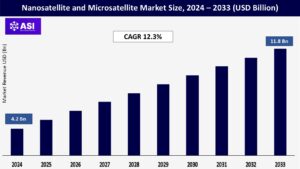

The global Nanosatellite and Microsatellite Market size was valued at approximately USD 4.2 billion in 2024 and is projected to reach USD 11.8 billion by 2033, growing at a robust CAGR of 12.3% during the forecast period (2026–2033).

The market is experiencing strong demand driven by advancements in miniaturization technology, increased government investments in space programs, and the rising use of small satellites for commercial applications.

Key growth drivers include the expansion of satellite-based communication services, earth observation capabilities, and defense and intelligence applications. The development of cost-effective satellite launch solutions, coupled with the growing adoption of satellite constellations by companies such as SpaceX and Amazon, is further fueling market expansion.

Additionally, the increasing use of nanosatellites and microsatellites for IoT connectivity, scientific research, and remote sensing is shaping the future of the industry.

The growing reliance on satellite technology for global communication, remote sensing, and environmental monitoring is a key driver of the nanosatellite and microsatellite market. These small satellites offer cost-effective solutions for real-time data collection, enabling applications in weather forecasting, disaster management, agriculture, and urban planning.

The surge in demand for high-speed internet and global connectivity, especially in remote and underserved regions, is propelling the adoption of satellite constellations. Companies such as SpaceX (Starlink), OneWeb, and Amazon (Project Kuiper) are deploying thousands of nanosatellites to create broadband networks, supporting the global expansion of internet services.

Additionally, government agencies and defense organizations are leveraging nanosatellites and microsatellites for surveillance, reconnaissance, and national security operations. The affordability and rapid deployment capabilities of these satellites make them ideal for military and intelligence applications, contributing to market growth.

In Satellite Miniaturization and Launch Systems Advancements in satellite miniaturization, propulsion systems, and modular satellite architectures are significantly enhancing the performance and affordability of nanosatellites and microsatellites.

The development of advanced payloads, high-resolution imaging sensors, and AI-driven data processing capabilities is expanding the scope of satellite applications.

Innovations in launch systems, including the emergence of dedicated small satellite launch vehicles such as Rocket Lab’s Electron, Virgin Orbit’s LauncherOne, and SpaceX’s Rideshare program, are reducing launch costs and increasing accessibility for commercial and academic satellite operators. These advancements are accelerating the adoption of small satellites across industries.

Despite their cost advantages compared to traditional satellites, nanosatellites and microsatellites still face challenges related to high launch costs and limited operational lifespan. The need for frequent replacements and maintenance can increase overall project expenses. Additionally, regulatory constraints and spectrum allocation challenges pose hurdles to market expansion.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Nanosatellites Microsatellites |

| By End-Use |

Commercial Government & Military Academic & Research |

| Key Players |

Lockheed Martin Corporation Northrop Grumman Corporation Airbus Defence and Space Thales Alenia Space Sierra Space Planet Labs Spire Global Rocket Lab Blue Canyon Technologies GomSpace Group |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Nanosatellites dominated the market in 2024 with a share of over 53.6%, driven by their lightweight structure, cost efficiency, and increasing deployment in satellite constellations. Microsatellites are gaining traction due to their enhanced payload capacity and extended mission capabilities.

The commercial segment leads the market, accounting for 62.1% of the share in 2024, driven by rising demand for satellite-based services, including IoT connectivity, broadband internet, and remote sensing.

Government and military applications are expanding, with defense agencies investing in small satellites for surveillance and security operations. The academic and research sector is also witnessing growth, with universities and research institutions leveraging nanosatellites for scientific experiments and space exploration.

North America accounted for 48.3% of the global nanosatellite and microsatellite market share in 2024, supported by strong government funding, the presence of leading space technology firms, and increasing private sector investments. The U.S. leads the region, with NASA, the Department of Defense, and private enterprises driving market expansion.

Europe holds a 23.7% market share, with key players such as the European Space Agency (ESA) and private space startups advancing satellite technology. Countries like Germany, the UK, and France are significant contributors to the region’s growth.

Asia-Pacific is projected to witness the highest CAGR of 14.1% during the forecast period, fueled by rising investments in space programs by China, India, and Japan. Government initiatives such as India’s PSLV program and China’s commercial satellite development efforts are enhancing regional market growth.

Middle East and Africa are emerging markets, with increasing investments in satellite communication infrastructure and earth observation projects. The UAE and Saudi Arabia are leading regional developments, with space agencies launching initiatives to expand satellite capabilities.

Latin America is experiencing steady growth, with Brazil and Mexico investing in satellite technology for environmental monitoring and telecommunication applications.

The global market was valued at approximately USD 4.2 billion in 2024.

The market is projected to grow at a CAGR of 12.3% from 2026 to 2033.

Key drivers include advancements in satellite technology, increasing demand for global connectivity, and rising investments in defense and intelligence applications.

Nanosatellites hold the largest market share due to their affordability and widespread deployment in satellite constellations.

North America holds the largest market share at 48.3%.

The Asia-Pacific region is expected to grow at a CAGR of 14.1% from 2026 to 2033.

Major players include Lockheed Martin, Northrop Grumman, Airbus, Thales Alenia Space, and Planet Labs.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Nanosatellite and Microsatellite Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Nanosatellite and Microsatellite Market, By End-Use

6.1 North America Nanosatellite and Microsatellite Market, By Country

6.1.1 Nanosatellite and Microsatellite Market, By Type

6.1.2 Nanosatellite and Microsatellite Market, By End-Use

6.2 U.S.

6.2.1 Nanosatellite and Microsatellite Market, By Type

6.2.2 Nanosatellite and Microsatellite Market, By End-Use

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping