Nucleic Acid Therapeutics CDMO Market

Nucleic Acid Therapeutics CDMO Market Share & Trends Analysis Report, By Service Type (Process Development, Manufacturing, Analytical & Quality Control, Fill & Finish, Packaging), By Nucleic Acid Type –DNA, RNA (mRNA, siRNA, ASO, miRNA, Others), By Therapeutic Area (Oncology, Infectious Diseases, Genetic Disorders, Neurological Disorders, Others), By End User(Biotechnology Companies, Pharmaceutical Companies, Academic & Research Institutes)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

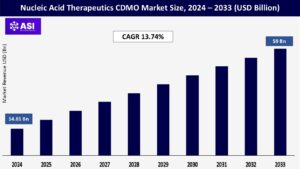

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 13.74%

Last Updated : December 15, 2025

The global Nucleic Acid Therapeutics CDMO Market was valued at approximately USD 14.81 billion in 2024 and is projected to reach USD 59 billion by 2033, growing at a CAGR of 13.74% during the forecast period (2025–2033).

The Nucleic Acid Therapeutics CDMO Market involves specialized service providers that help pharmaceutical and biotech companies develop and manufacture nucleic acid-based therapies like DNA, RNA (mRNA, siRNA), and gene-editing molecules. These therapies target diseases such as cancer, genetic disorders, and infections.

CDMOs offer services including process development, analytical testing, regulatory support, and GMP-compliant production. Key strengths of this market include advanced technologies, high purity standards, and strict regulatory compliance. As demand for personalized medicine grows, the market is expanding rapidly, driven by innovation and strategic collaborations.

The increasing interest in nucleic acid-based drugs such as mRNA vaccines, siRNA, antisense oligonucleotides, and gene therapies is a major driver of the CDMO market. These therapies offer targeted, personalized treatment options for a range of diseases including cancer, rare genetic disorders, and infectious diseases.

The success of mRNA vaccines during the COVID-19 pandemic has validated the potential of nucleic acid technologies, leading to expanded R&D pipelines in both large pharmaceutical companies and biotech startups.

However, the complex nature of developing and manufacturing nucleic acid drugs requires specialized infrastructure and expertise, which many sponsors lack in-house. As a result, they are increasingly outsourcing development and production to CDMOs with the capabilities to meet quality, scalability, and regulatory demands.

Pharmaceutical and biotech companies are increasingly outsourcing complex and cost-intensive processes to CDMOs to reduce time-to-market, control costs, and access advanced technologies.

Nucleic acid therapeutics require highly specialized manufacturing processes (e.g., oligonucleotide synthesis, lipid nanoparticle formulation, plasmid production), and CDMOs offer the expertise, equipment, and regulatory knowledge to handle these tasks efficiently.

Outsourcing allows drug developers to focus on research and commercialization while relying on CDMOs for GMP-compliant production and scale-up. This trend is further reinforced by the shortage of in-house capabilities and the need for flexible, rapid-response manufacturing solutions, particularly for early-phase clinical trials and personalized therapies.

One significant restraint in the Nucleic Acid Therapeutics CDMO market is the high complexity and cost associated with the manufacturing processes of nucleic acid-based therapies. Producing DNA, RNA (including mRNA, siRNA), and gene editing molecules requires specialized technologies, strict environmental controls, and compliance with rigorous GMP standards.

These processes involve advanced techniques such as oligonucleotide synthesis, lipid nanoparticle formulation, plasmid DNA production, and viral vector engineering each requiring precise handling to ensure product purity, stability, and efficacy.

Furthermore, scaling up production from laboratory to commercial levels is particularly challenging, often leading to delays and increased costs. The need for cleanrooms, contamination control, and high-end analytical methods significantly adds to capital and operational expenditures.

Small and mid-sized CDMOs may struggle to meet these technical and regulatory demands, limiting their participation in the market. Additionally, regulatory scrutiny from authorities like the FDA and EMA adds another layer of complexity, making compliance both time-consuming and resource-intensive. This high barrier to entry can slow market growth and limit innovation, especially in regions with limited infrastructure or expertise.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Service Type |

Process Development Manufacturing Analytical & Quality Control Fill & Finish Packaging

|

| By Nucleic Acid Type |

DNA RNA (mRNA, siRNA, ASO, miRNA, Others) |

| By Therapeutic Area |

Oncology Infectious Diseases Genetic Disorders Neurological Disorders Others |

| By End-User |

Biotechnology Companies Pharmaceutical Companies Academic & Research Institutes |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Nucleic Acid Therapeutics CDMO Market is segmented by Service Type, Nucleic Acid Type, Therapeutic Area and End User.

Each factor plays a crucial role in accelerating drug development timelines, improving the quality and scalability of nucleic acid-based therapies, and supporting the growing demand for innovative, targeted treatments across genetic, infectious, and oncological diseases.

Process Development This includes early-stage development activities such as plasmid design, oligonucleotide synthesis optimization, and formulation design. As nucleic acid drugs are complex and sensitive, customized process development is critical to ensure stability, efficacy, and scalability. The growing pipeline of RNA and gene therapies is driving demand for specialized process development services.

Manufacturing CDMOs offer cGMP-compliant manufacturing of nucleic acid therapeutics, including bulk drug substances (e.g., mRNA, DNA plasmids) and drug products. Manufacturing capabilities often include high-throughput oligonucleotide synthesis, lipid nanoparticle (LNP) encapsulation, and viral vector production. As demand for scalable solutions increases, this is one of the fastest-growing segments.

Analytical & Quality Control This involves rigorous testing and validation to ensure nucleic acid purity, identity, potency, and stability. Techniques like HPLC, qPCR, gel electrophoresis, and mass spectrometry are employed. Given the regulatory scrutiny and the complexity of nucleic acid drugs, this segment is essential and growing rapidly.

Fill & Finish Includes sterile filling of nucleic acid-based formulations into vials or syringes under aseptic conditions. Fill & finish is critical for product safety and shelf-life. RNA and DNA therapeutics, especially those using LNPs, require advanced sterile filling technologies to avoid degradation or contamination.

Packaging Specialized packaging is needed to protect the integrity of sensitive nucleic acid-based drugs. This includes temperature-controlled packaging and labeling for clinical or commercial use. As cold chain requirements for RNA drugs grow, packaging solutions are becoming increasingly vital.

DNA Includes plasmid DNA used in gene therapy, DNA vaccines, and CRISPR applications. With the rise of genetic engineering and DNA-based immunotherapies, demand for DNA manufacturing and development is increasing.

RNA mRNA The largest and fastest-growing RNA subsegment due to its success in COVID-19 vaccines and expanding applications in oncology and infectious diseases.

siRNA (small interfering RNA) Used in gene silencing therapies, especially for rare and metabolic diseases. ASO (Antisense Oligonucleotides) These modify gene expression and are widely researched for neurological and genetic disorders.

miRNA (Micro RNA) An emerging area with potential for regulating multiple gene targets, though still mostly in preclinical and early clinical phases.

Others Includes guide RNAs for CRISPR and long non-coding RNAs under investigation for various therapies.

Oncology A leading segment due to the high unmet need for targeted cancer therapies. mRNA vaccines, siRNA, and DNA-based immunotherapies are increasingly used in cancer treatment. CDMOs are expanding capabilities to support oncology-focused pipelines.

Infectious Diseases Accelerated by the success of mRNA vaccines for COVID-19, this segment remains strong. New vaccines and antiviral nucleic acid drugs are under development for diseases like influenza, RSV, and HIV.

Genetic Disorders One of the core application areas for nucleic acid therapeutics, especially DNA- and RNA-based therapies, to correct or silence defective genes. Rare genetic diseases are a key focus due to the suitability of personalized nucleic acid approaches.

Neurological Disorders Includes therapies for diseases such as ALS, Huntington’s, and spinal muscular atrophy, with antisense oligonucleotides (ASOs) and siRNA showing therapeutic promise. This is a growing therapeutic segment.

Others Includes cardiovascular diseases, autoimmune disorders, metabolic diseases, and regenerative medicine applications, reflecting the broadening pipeline of nucleic acid therapeutics.

Biotechnology Companies Major consumers of CDMO services, especially startups and mid-sized firms lacking in-house manufacturing. These companies drive innovation and typically outsource early-stage development, clinical manufacturing, and scale-up to CDMOs.

Pharmaceutical Companies Large pharma firms increasingly partner with or acquire CDMOs to expand their nucleic acid capabilities. They typically require full-scale, commercial-grade manufacturing and regulatory support.

Academic & Research Institutes Key players in early-stage discovery and preclinical development. They often collaborate with CDMOs to translate lab findings into scalable production for clinical trials or licensing deals.

Holds the dominant position in the nucleic acid therapeutics CDMO market, driven by a well-established biotechnology ecosystem, substantial R&D investments, and the presence of key market players such as Thermo Fisher Scientific, Catalent, and Aldevron.

The United States, in particular, leads due to its rapid adoption of mRNA, siRNA, and gene therapies, supported by advanced infrastructure and a strong regulatory framework.

The region’s robust clinical trial landscape and favorable funding environment further accelerate innovation and outsourcing demand, although high operational costs and regulatory complexities remain as challenges.

Represents another significant market, fueled by strong academic research, government funding, and a supportive regulatory environment led by the European Medicines Agency (EMA). Countries such as Germany, the UK, Switzerland, and France are key contributors, offering a mix of innovation and manufacturing capabilities.

The region is witnessing steady expansion in CDMO capacities for oligonucleotide and gene therapy manufacturing. However, varying regulations across countries and slower approval processes in some regions slightly hinder unified market growth.

The fastest-growing region in the nucleic acid therapeutics CDMO market, with countries like China, India, South Korea, and Japan at the forefront. The region benefits from cost-efficient manufacturing, a growing skilled workforce, and rising investments in biotechnology infrastructure.

China and India, in particular, are becoming global hubs for outsourcing due to their scalability and expanding GMP-compliant facilities. Government initiatives and national healthcare programs are further encouraging innovation in gene and RNA-based therapies.

Nonetheless, challenges such as inconsistent regulatory standards and intellectual property concerns must be addressed for sustainable growth.

An emerging market in this space, showing gradual progress as awareness of nucleic acid therapeutics increases. Countries like Brazil, Mexico, and Argentina are witnessing growth in clinical trials and biopharma investments.

The region offers potential for expansion due to its large patient population and growing interest from global CDMOs seeking to broaden their geographic reach. However, underdeveloped biotech infrastructure, regulatory hurdles, and limited investment in R&D continue to limit rapid growth.

Region is currently at a nascent stage in the nucleic acid therapeutics CDMO market but is showing promising developments. Government-backed initiatives, especially in the UAE and Saudi Arabia, are aiming to build strong life sciences and biotech capabilities under broader economic diversification plans.

Collaborations with international pharma companies and investments in research are emerging trends. Yet, the region faces significant constraints such as lack of skilled personnel, limited manufacturing capacity, and underdeveloped regulatory systems.

The market was valued at USD 14.81 billion in 2024.

The market is projected to grow at a CAGR of 13.74% from 2025 to 2033.

Process Development hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Thermo Fisher Scientific, Catalent, Inc. and Lonza Group AG.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Nucleic Acid Therapeutics CDMO Market, Service Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Nucleic Acid Therapeutics CDMO Market, By Nucleic Acid Type

5.3 Nucleic Acid Therapeutics CDMO Market, By Therapeutic Area

5.4 Nucleic Acid Therapeutics CDMO Market, By End-User

6.1 North America Nucleic Acid Therapeutics CDMO Market, By Service Type

6.1.1 Nucleic Acid Therapeutics CDMO Market, By Nucleic Acid Type

6.1.2 Nucleic Acid Therapeutics CDMO Market, By Therapeutic Area

6.1.3 Nucleic Acid Therapeutics CDMO Market, By End User

.2 U.S.

6.2.1 Nucleic Acid Therapeutics CDMO Market, By Service Type

6.2.2 Nucleic Acid Therapeutics CDMO Market, By Nucleic Acid Type

6.2.3 Nucleic Acid Therapeutics CDMO Market, By Therapeutic Area

6.2.4 Nucleic Acid Therapeutics CDMO Market, By End-User

.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America