Off-Road Vehicle Market

Off-Road Vehicle Market Size, Share & Trends Analysis Report By Vehicle Type (All-terrain Vehicle (ATV), Utility Task Vehicle (UTV), Snowmobiles), By Application (Sports, Agriculture, Military), By Propulsion (Disel, Electric) Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

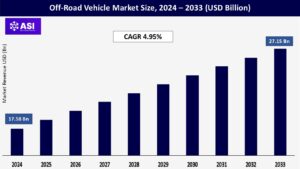

CAGR: 4.95%

Last Updated : June 2, 2026

The global Off-road Vehicle Market size was valued at USD 17.58 billion in 2024 and is estimated to grow from USD 18.45 billion in 2025 to reach USD 27.15 billion by 2033, growing at a CAGR of 4.95% during the forecast period (2025-2033).

ATVs and UTVs were mainly used for sports and leisure activities. These vehicles are now utilized in the agricultural industry, and for patrolling, hunting, gardening, and other tasks, as their applications have evolved through time. Manufacturers are also attempting to promote the use of electric ATVs and UTVs.

Because most ATVs and UTVs are not allowed to be operated on highways and other main roads, government authorities across the world have boosted budgetary allocations to develop new off-road paths that may be useful for leisure enthusiasts and stimulate adventure sports activities in the area. This is expected to grow the market under investigation.

Due to operational circumstances off-road vehicles are designed to operate on rugged terrain end users expect better output efficiency and optimum performance in high-end driving activities. Additionally, most producers of off-road vehicles are working on these drive systems to meet shifting consumer demands.

Additionally, end consumers’ demand outlook has evolved more in favor of increased comfort and driving dynamics. Off-road cars with four-wheel drive and all-wheel drive are becoming more popular due to evolving consumer demands that allow them to function on rugged terrain.

The adoption of AWD and 4WD utility vehicles has grown significantly recently, and this trend is predicted to continue in the years to come. This is expected to promote the expansion of off-road vehicles.

Off-road vehicle demand is rising quickly because additional safety features may be incorporated into new off-road vehicles due to stricter regulatory oversight and new testing criteria, increasing the market’s potential for growth. New measures being taken by governments could increase the market for off-road vehicles.

Government officials have boosted the budgetary allotments for the construction of new off-road paths, which may benefit recreational enthusiasts and improve the popularity of adventure sports in the area. Countries are developing new off-road parks, which will undoubtedly help youthful ATV and UTV users increase the scale of their commercialization.

In March 2021, the Grand Prairie City Council approved the specific use permit for Lone Star Off-Road Park. The site is an outdoor amusement park for off-road vehicles, all-terrain vehicles, including Jeeps, and off-highway vehicles.

The growing number of off-roading competitions in the North American region as the American Motorcyclist Association (AMA) organizes various dedicated ATV series, like ATV Motocross National Championship Series and ATV Extreme Dirt Track National Championship Series. This racing series will further increase the share of Americans who own an ATV in the coming years.

Though ATVs are popular adventure vehicles mainly in North America, some states in the United States and Canada do not allow their usage on most public roads, streets, or highways. This is due to many ATV-related injuries and fatalities reported in just the United States.

For instance, the “Annual Report of ATV Related Deaths and Injuries 2020” estimates 524,600 injuries treated in emergency rooms between 2015 and 2019 based on data from five off-highway vehicles and the U.S. Consumer Product Safety Commission (CPSC) and NEISS (an annual average of 104,900 injuries).

These product codes cover ATVs, ROVs, UTVs, and perhaps some other unspecified off-highway vehicles. The U.S. Department of Transportation classified ATVs as motor vehicles that are not permitted to be used on significant roadways due to all the above statistics.

They can only be used in cities and rural areas in some states. Their use is restricted to specified routes with explicit mention of the authorization for operation in several major cities and suburbs.

Canada increased the severity of the penalties for using ATVs to combat forest fires. If violators’ vehicles are discovered to be lacking a spark detector, they may be subject to a fine of USD 460 or an administrative penalty of up to USD 10,000.

In case of a forest fire caused by the vehicles, the operator can even receive a court order fine of USD 1 million. All these factors may deter the growth of the market studied. However, the number of ATV-related fatalities is significantly decreasing with stringent regulations.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Vehicle Type |

All-terrain Vehicle (ATV) Utility Task Vehicle (UTV) Snowmobiles |

| By Application Sports |

Agriculture Sports Military |

| By Propulsion Type |

Disel Electric |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Utility Task Vehicles (UTVs) dominate the off-road vehicle market, commanding approximately 73% of the total market share in 2024, with a market value of USD 11.55 billion. The segment’s strong performance is driven by its versatility in operating across rough terrains, making them essential in agriculture, defense, and military operations.

UTVs’ high cargo-carrying capacity and quick mobility on hard surfaces are crucial for anti-terrorist operations and border security combats, particularly in coastal areas. The segment is witnessing significant technological advancements, with manufacturers continually introducing models with improved towing capacities, greater payload capacities, and advanced safety features.

The shift toward electrification is also gaining traction, with companies like Polaris and Honda launching electric UTV models that offer lower emissions and reduced maintenance costs.

Furthermore, the growing popularity of outdoor recreational activities has significantly boosted the UTV market, with consumers increasingly drawn to these vehicles for trail riding, dune bashing, hunting, and other adventure sports.

All-Terrain Vehicles (ATVs) represent a significant segment in the off-road vehicle market, offering unique capabilities for both recreational and utility purposes. The segment’s growth is driven by increasing recreational and sports expenditure and the rising number of off-roading events worldwide.

The military sector’s growing adoption of ATVs for diverse applications, including transporting armed forces and ammunition across long distances, provides additional momentum to market expansion. Manufacturers are actively introducing new models with advanced features and improved safety systems to meet evolving consumer demands.

The segment is also witnessing a transformation with the integration of electric powertrains, as companies respond to growing environmental concerns and stricter emission regulations.

Additionally, the agricultural sector continues to be a steady source of demand, with farmers utilizing ATVs for various tasks including crop monitoring, livestock management, and general transportation across farmland.

The snowmobile segment encompasses a diverse range of vehicles designed specifically for travel on snow and ice. Snowmobiles are classified into mountain models for deep snow, trail models for groomed trails, performance models for speed and racing, and touring models for long-distance travel with increased comfort and storage.

Snowmobiles are in high demand among recreational enthusiasts, adventure sports participants, and utility users in industries such as forestry and rescue missions. The increasing popularity of winter sports, introduction of electric snowmobiles and eco-friendly technologies, and advancements in technology are driving the growth of the segment.

Ski-Doo offers zero-emission snowmobiles which attract environment-conscious consumers contributing to higher sales and market expansion. Key Players in this segment are Polaris, Ski-Doo, Yamaha, Alpine Snowmobile, etc.

The diesel segment held a 47% market share in 2024. Off-road vehicles market, the diesel segment refers to vehicles powered by diesel engines. These vehicles typically offer robust torque and fuel efficiency, making them well-suited for heavy-duty applications in industries like agriculture, construction, and utilities.

Despite the growing popularity of electric and gasoline-powered off-road vehicles, the diesel segment continues to see demand, particularly in sectors where durability and towing capacity are paramount.

However, there’s a rising trend towards cleaner diesel engines compliant with stricter emissions regulations to address environmental concerns.

The electric off-road vehicle market is expected to experience considerable growth during the analyzed timeframe owing to the rising demand for off-road vehicles from applications including sports events, agriculture, tourism, and others.

In addition, the rise in demand for off-road vehicles owing to the increasing popularity of the off-road sports and tourism sector is anticipated to drive market growth in the coming years.

Moreover, the rise in investment towards research and development of off-road electric vehicles to fulfill the goal of minimizing carbon emissions is expected to propel the market growth from 2025 to 2033.

The sports segment maintains its dominant position in the off-road vehicle market, accounting for approximately 69% of the total market share in 2024. This substantial market share is driven by the growing popularity of off-road racing events and rising recreational activities across major regions.

All-terrain vehicles (ATVs) and utility terrain vehicles (UTVs) are witnessing considerable demand due to their high power, excellent maneuverability, and ability to be driven through various terrains, making them ideal for off-road racing and numerous recreational purposes.

Leading manufacturers leverage off-road racing competitions, adventure sports events, and tourism-related activities to demonstrate their vehicles’ performance, building brand recognition and sparking consumer interest.

The implementation of stringent safety standards by regulatory bodies, including mandatory safety gear requirements, vehicle specifications, and track safety measures, has further strengthened consumer confidence in sports-oriented off-road vehicles.

The agriculture segment is projected to be the fastest-growing segment in the off-road vehicle market, with an expected growth rate of approximately 6% during the forecast period 2025-2023.

This growth is primarily attributed to the increasing adoption of ATVs and UTVs for various agricultural applications, including animal handling, transporting feed, spraying pesticides and fertilizers, planting seeds, and general transportation.

The agricultural community’s preference for these vehicles over traditional methods like horses and pickup trucks is driven by their versatility, cost-effectiveness, and user-friendly nature.

Manufacturers are responding to this growing demand by developing specialized agricultural models with enhanced features such as improved towing capacities, greater payload capabilities, and advanced technology integration like GPS systems for precision farming applications.

The military segment is anticipated to witness rapid growth over the projected period. Off-road vehicles market, the military segment refers to vehicles specifically designed for military applications, such as troop transport, reconnaissance, and logistics support.

Trends in this segment include a growing demand for rugged, versatile vehicles capable of operating in diverse terrain conditions. Military off-road vehicles are increasingly incorporating advanced technologies for improved performance, durability, and survivability.

Additionally, there is a trend towards the development of electric-powered and autonomous off-road vehicles to enhance operational efficiency and reduce environmental impact.

The Asia-Pacific region represents a dynamic market for off-road vehicles, with China, Japan, India, and South Korea emerging as key markets. Each country exhibits distinct characteristics in terms of adoption patterns and usage scenarios.

The region demonstrates strong growth potential driven by increasing recreational activities, agricultural mechanization, and industrial applications.

The market is witnessing significant developments in electric off-road vehicles, particularly in China and Japan, while emerging economies like India are showing increased adoption in both recreational and utility segments.

The European off-road vehicle market demonstrates a diverse landscape with varying adoption rates across different countries. Germany, the United Kingdom, France, Spain, and Italy represent the key markets, each with its unique characteristics and growth drivers.

The region’s market is influenced by strict emission regulations and safety standards, particularly affecting vehicle design and manufacturing processes. The agricultural sector remains a significant driver for ATV and UTV adoption, while recreational and adventure tourism activities continue to expand across various European countries.

The North American region accounted for the largest share of more than 65% of the global revenue in 2024. A considerable rise in the adoption of ATVs & UTVs for recreational activities, such as trailing and mountain riding, was observed as one of the key factors driving the segment growth.

In addition, the increased use of ATVs for farming activities and the growing availability of off-road vehicles at local stores at various places owing to supportive government policies proved to be the driving factor for the segment growth. The Europe region is expected to register the fastest CAGR over the forecast period.

The Middle East and Africa region shows promising growth prospects, driven by rising adventure tourism and increasing demand for off-road vehicles in military and defense operations.

South America emerges as the larger market in this region, while the Middle East and Africa demonstrate faster growth potential. Government initiatives promoting manufacturing plant setup and the construction of new off-road trails contribute to market development across both regions.

The market is expected to grow CAGR of 4.95 % from 2025 to 2033.

The current market size is USD 17.58 Billions in 2024.

North America currently holds the largest market shares.

Top industry players are, Polaris Inc., BRP Inc., Honda Motor Company, Yamaha Motor Corporation, Arctic Cat Inc., Suzuki Motor Corporation, American LandMaster, Kawasaki Motors Corp., Kwang Yang Motor Co. Ltd, Kubota Corporation., etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Off-Road Vehicle Market, By Vehicle Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Off-Road Vehicle Market, By Application Sports

5.3 Off-Road Vehicle Market, By Propulsion Type

6.1 North America Off-Road Vehicle Market , By Country

6.1.1 Off-Road Vehicle Market, By Vehicle Type

6.1.2 Off-Road Vehicle Market, By Application Sports

6.1.3 Off-Road Vehicle Market, By Propulsion Type

6.2 U.S.

6.2.1 Off-Road Vehicle Market, By Vehicle Type

6.2.2 Off-Road Vehicle Market, By Application Sports

6.2.3 Off-Road Vehicle Market, By Propulsion Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping