Oncology Cancer Drugs Market

Oncology Cancer Drugs Market Share & Trends Analysis Report, By Drug Type (Chemotherapy, Targeted Therapy, Immunotherapy(Biologic Therapy), Hormonal Therapy, Cytotoxic Drugs, and others), By Cancer type (Lung cancer, breast cancer, colorectal cancer, prostate cancer, blood cancer, liver cancer, stomach cancer, bladder cancer, and others), By Therapy type (Chemotherapy, Targeted Therapy, Immunotherapy), By Route of administration ( Injectable (Intravenous, Subcutaneous, Intramuscular) Oral,Other Routes), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies). Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

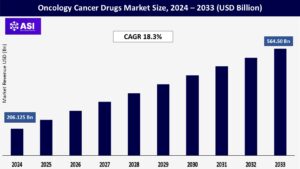

CAGR: 18.3%

Last Updated : December 25, 2025

The global Oncology Cancer Drugs Market size was valued at approximately USD 206.125 billion in 2024 and is projected to reach USD 564.50 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 18.3% during the forecast period of 2025–2033.

The global oncology drugs market is set for impressive growth between 2025 and 2033, fueled by rising cancer rates, ongoing innovation in drug development, and evolving regulatory support. By 2033, the market is expected to reach USD 564.5 billion, reflecting a healthy compound annual growth rate (CAGR) of 18.3%. Within this broader trend, specific segments like generic oncology drugs and breast cancer treatments are also gaining momentum, driven by increasing demand and expanded access to life-saving therapies.

The oncology drugs market is experiencing dynamic growth, largely fueled by a wave of innovative therapies emerging from ongoing research and development. One of the most transformative areas is the rise of targeted therapies, which are designed to home in on specific genetic mutations or molecular features of cancer cells. Unlike traditional chemotherapy, these treatments offer greater precision and fewer side effects, significantly improving patient outcomes.

Another major breakthrough is in immunotherapy, including game-changing approaches like immune checkpoint inhibitors and CAR-T cell therapies, which empower the body’s immune system to identify and destroy cancer cells. These therapies are showing remarkable results, especially in hard-to-treat cancers, and are paving the way for long-term remission in some patients.

Complementing these advances is the rise of precision medicine, driven by discoveries in genomics and biomarkers, which make it possible to tailor treatments to each patient’s unique biological makeup. This personalized approach not only increases treatment effectiveness but also minimizes unnecessary side effects. Further supporting the market’s momentum is a robust drug pipeline, with hundreds of new oncology candidates currently in clinical trials offering hope for more breakthroughs and sustained market expansion in the years ahead.

Several underlying factors are driving the steady rise in cancer cases globally, which in turn fuels the demand for oncology drugs. One major contributor is the aging population as people live longer, the likelihood of developing cancer increases, since cancer is more prevalent in older adults. Alongside aging, modern lifestyle habits are also playing a role.

Diets high in processed foods, sedentary behavior, smoking, and excessive alcohol use, combined with exposure to environmental pollutants, have all been linked to an increased cancer risk. At the same time, advancements in diagnostic tools and growing public awareness are leading to earlier and more accurate cancer detection. While early diagnosis improves survival outcomes, it also means more patients are being identified and treated boosting the demand for effective oncology therapies. These converging trends are shaping both the challenges and opportunities in the cancer treatment landscape.

One of the most pressing challenges facing the oncology drugs market is the extremely high cost of innovative treatments, particularly targeted therapies and immunotherapies. While these drugs offer significant clinical benefits, their price tags often place them out of reach for many. For patients especially in low- and middle-income countries the cost can be a major barrier, even when insurance or government subsidies are available.

This issue goes beyond individual affordability; it also places immense pressure on health insurers and public healthcare programs, which must make difficult decisions about coverage and eligibility. As a result, access to these therapies is often limited or delayed, not based on medical need, but on financial constraints. On a broader scale, the rising costs of cancer treatments are straining national healthcare budgets, forcing systems to balance innovation with sustainability. This financial hurdle is arguably the most significant restraint on the global oncology market, threatening to widen the gap between medical advancement and real-world accessibility.

Another key restraint in the oncology drugs market is the revenue erosion faced by pharmaceutical companies as patents on blockbuster cancer drugs expire. Once these exclusivity periods end, the market often sees a flood of lower-cost generic and biosimilar alternatives, which quickly erode the sales of the original branded drugs. While this shift is beneficial from a public health standpoint making treatments more affordable and accessible it places immense pricing pressure on the original manufacturers.

The entry of biosimilars increases competition and reduces profit margins, especially for well-established therapies that once dominated the market. As a result, even though the overall demand for cancer treatments continues to grow, the market value of individual drug classes may stagnate or decline, limiting the financial incentive for companies to reinvest in similar therapies. This dynamic is reshaping how companies approach oncology R&D and market strategies moving forward.

| Report Metric | Details |

|---|---|

| By Drug Type |

Targeted Therapy Drugs Monoclonal Antibodies (mAbs) Tyrosine Kinase Inhibitors (TKIs) Other Small Molecule Inhibitors Immunotherapy (Biologic Therapy) Drugs Immune Checkpoint Inhibitors (PD-1, PD-L1, CTLA-4 inhibitors) CAR T-cell Therapy Oncolytic Viruses Cancer Vaccines Cytokines Chemotherapy Drugs Alkylating Agents Antimetabolites Plant Alkaloids Antitumor Antibiotics Platinum-based Drugs Hormonal Therapy Drugs Aromatase Inhibitors Anti-estrogens (SERMs, SERDs) Anti-androgens Other Drug Classes: (e.g., Radiopharmaceuticals, Angiogenesis Inhibitors, Proteasome Inhibitors) |

| By Cancer Type |

Lung Cancer (Non-Small Cell Lung Cancer, Small Cell Lung Cancer) Breast Cancer (HR+, HER2+, Triple-Negative) Colorectal Cancer Prostate Cancer Blood Cancers: Leukemia Lymphoma (Hodgkin’s, Non-Hodgkin’s) Multiple Myeloma Gastrointestinal Cancers (Stomach, Esophageal, Liver, Pancreatic) Bladder Cancer Kidney Cancer Ovarian Cancer Head & Neck Cancer Cervical Cancer Skin Cancer (Melanoma, Non-melanoma) Brain Tumors Other Rare Cancers |

| By Therapy type |

Targeted Therapy Immunotherapy Chemotherapy Hormonal Therapy Combination Therapies (integrating multiple modalities) |

| By Route of Administration |

Injectable (Intravenous, Subcutaneous, Intramuscular) Oral Other Routes |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

| Key Players |

Pfizer Inc. Amgen Inc. Novartis AG GSK plc Eli Lilly and Company AstraZeneca PLC AbbVie Inc. Ono Pharmaceutical Company Johnson and Johnson Astellas Pharma Inc. Bayer Healthcare F. Hoffmann-La Roche Ltd. Bristol-Myers Squibb Company Merck & Co., Inc. Takeda Eisai Sanofi |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Oncology Cancer Drugs Market is categorized by drug type, by cancer type, by therapy type and by distribution channel. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. The market is typically segmented across several key dimensions to provide a comprehensive understanding of its dynamics.

Targeted Therapy and Immunotherapy are truly revolutionizing how we fight cancer. Imagine treatments that are like smart bombs, specifically hitting cancer cells while largely leaving healthy ones alone. That’s the beauty of Targeted Therapy. Its precision not only makes it incredibly effective but also significantly cuts down on the harsh side effects often associated with traditional treatments. This focus on precision is exactly why it holds the biggest slice of the market pie right now. Then there’s Immunotherapy, which is perhaps the most exciting and rapidly expanding frontier in cancer care.

Instead of fighting cancer directly, these remarkable drugs, including innovations like checkpoint inhibitors and CAR-T therapies, essentially ‘wake up’ and empower your body’s own immune system to become the ultimate cancer-fighting army. This approach is gaining immense traction because it harnesses the body’s natural defenses, leading to more effective and sometimes even long-lasting responses. Now, while these cutting-edge therapies are taking center stage, we can’t forget about Chemotherapy. It’s the long-standing warrior in the cancer fight, and it still plays a vital role, especially in parts of the world with fewer resources. In low- and middle-income countries, it remains a go-to option due to its established effectiveness and often lower cost.

However, in more developed regions, where patients have access to newer, less toxic alternatives, its usage is gradually, but steadily, seeing a decline. Hormonal Therapy also remains a steady and crucial pillar in specific cancer battles. For certain cancers like breast and prostate cancer, where hormones play a key role in growth, these therapies act by blocking or reducing hormone levels, offering a well-established and stable treatment path.

Finally, for many around the globe, the cost of these life-saving drugs is a huge concern. This is where Biosimilars and generic oncology drugs come into play. They are becoming increasingly important, especially in emerging markets, because they offer more affordable and accessible versions of effective treatments. This makes a real difference in ensuring that more people can get the vital care they need, breaking down financial barriers to health.

When we look at the different types of cancer driving the drug market, it’s clear that Breast Cancer truly stands out as the largest and most impactful segment. This isn’t surprising, given how common it is, combined with the incredibly proactive and widespread screening programs that help detect it early. This constant flow of new diagnoses ensures a consistent and significant demand for effective treatments. Close behind, Lung Cancer also commands a substantial portion of the market. Its widespread prevalence is a key factor, but what’s really propelling its segment are the incredible strides made in therapies.

The advent of highly precise targeted treatments and innovative immunotherapies has revolutionized how we combat lung cancer, offering new hope and driving significant investment in this area. Beyond these two major players, other cancers like Colorectal Cancer, Prostate Cancer, and the various Blood Cancers (such as leukemia and lymphoma) are also vital contributors to the oncology drug market. Their continued importance is largely due to the ongoing, relentless pace of innovation, which constantly brings forth new and improved treatment options, ensuring these segments remain strong and dynamic.

Finally, we’re seeing exciting growth in what might be considered “other” segments, including cancers like melanoma, ovarian cancer, and liver cancers. The momentum in these areas is largely fueled by the transformative power of personalized medicine. This approach allows treatments to be tailored specifically to an individual’s unique cancer profile, leading to more effective outcomes and opening up entirely new avenues for drug development.

The oncology drugs market is increasingly defined by diverse treatment modalities that reflect the evolution of cancer care toward more personalized and effective approaches. Targeted therapies have gained prominence by focusing on specific genetic mutations or proteins that drive cancer growth, allowing for more precise treatment with fewer side effects. Meanwhile, immunotherapy is reshaping the landscape by harnessing the body’s immune system to recognize and attack cancer cells offering durable responses in certain cancers. While newer approaches gain ground, chemotherapy continues to play a vital role, especially in advanced-stage cancers, often forming the backbone of treatment regimens.

Hormonal therapies are widely used for hormone-sensitive cancers like breast and prostate cancer, helping to slow or stop the disease by interfering with hormone production or activity. Increasingly, clinicians are adopting combination therapies, integrating multiple treatment modalities to improve outcomes, reduce resistance, and tailor treatments more closely to individual patient needs. This trend toward personalized, multimodal treatment is shaping the future of oncology care.

In the oncology drugs market, the route of administration plays a crucial role in treatment effectiveness, patient comfort, and healthcare delivery. Injectable therapies including intravenous (IV), subcutaneous (under the skin), and intramuscular injections remain the most common method of administering cancer drugs, particularly for advanced treatments like chemotherapy, immunotherapy, and targeted biologics. These are often delivered in clinical settings under medical supervision, ensuring precise dosing and monitoring.

However, there’s a growing shift toward oral oncology drugs, driven by their convenience, improved patient adherence, and the ability to take medications at home, which reduces hospital visits and enhances quality of life. This trend is especially visible in targeted therapies and hormonal treatments. While still a smaller portion of the market, other routes such as topical applications or localized delivery systems are being explored for specific cancers or in supportive care. Overall, the choice of administration route is becoming an important factor in treatment planning, balancing clinical efficacy with patient-centered care.

The distribution of oncology drugs is evolving to meet the growing demand for accessibility, convenience, and specialized care. Hospital pharmacies continue to dominate the market, as many cancer treatments especially injectables like chemotherapy and immunotherapy are administered in clinical or inpatient settings under close medical supervision. These facilities are essential for managing complex treatment protocols and monitoring patient responses.

At the same time, retail pharmacies, including specialty pharmacies, are playing an increasingly important role, particularly in the dispensing of oral oncology drugs and supportive care medications. Specialty pharmacies are equipped to handle high-cost, high-complexity cancer therapies and provide critical services such as counseling and insurance support.

Meanwhile, online pharmacies are gaining traction, offering patients greater convenience and often better pricing on maintenance medications, especially for long-term treatments. While still a smaller part of the market, the online channel is expected to grow steadily, driven by the rising adoption of telemedicine and home-based cancer care.

A closer look at the global oncology cancer drugs market reveals clear regional differences in size, growth, and challenges. What’s consistent across the board, though, is the market’s overall upward momentum driven by rising cancer rates and ongoing breakthroughs in drug development. North America continues to lead the way, both in terms of market share and pharmaceutical innovation. Meanwhile, the Asia-Pacific region is emerging as a major growth engine, thanks to its large population base and rapidly advancing healthcare infrastructure. In Latin America and the Middle East & Africa (MEA), the market is beginning to gain traction. These emerging regions show promising potential, but face hurdles like limited access to treatment and affordability of cancer drugs.

North America, particularly the United States, remains the largest and most dominant market for oncology drugs globally, with its market value expected to reach around USD 64.5 billion in 2024. This strong position is driven by several key factors, including high investments in research and development, as the region is home to many leading pharmaceutical and biotech companies at the forefront of developing advanced treatments like targeted therapies, immunotherapies, and precision medicine.

The region’s well-established healthcare infrastructure and high healthcare spending further support the adoption of cutting-edge, often expensive cancer treatments. A high prevalence of cancers, especially lung and breast cancer continues to fuel demand for oncology drugs. In addition, North America benefits from a favorable regulatory environment, with streamlined drug approval pathways such as accelerated approvals that help bring new therapies to market faster.

The market is also marked by a strong focus on personalized medicine, supported by advances in genomics and molecular diagnostics. Dominant trends in the region include the growing adoption of targeted therapies and immunotherapies, along with a rising emphasis on individualized treatment approaches. However, challenges remain, particularly related to the high cost of therapies and the complexities involved in reimbursement processes.

Europe holds a significant position in the global oncology drugs market, with an estimated market size of USD 54.79 billion in 2024, projected to grow to USD 81.26 billion by 2029 at a CAGR of 8.20%. Some forecasts suggest even faster growth over the longer term, with a CAGR of 15.8% from 2025 to 2034, positioning Europe as one of the fastest-growing regions. This growth is largely driven by the continent’s aging and sizable population, which has led to a rising number of cancer cases, around 3.9 million new cases in 2018, expected to reach over 6 million by 2040.

The region is also witnessing rapid adoption of advanced treatments such as targeted therapies, immunotherapies, and personalized medicine, which are improving survival outcomes. Strong research and development efforts, backed by both pharmaceutical companies and government funding, continue to fuel innovation. Countries like Germany, the UK, France, Italy, and Spain are key players, supported by well-developed healthcare systems and growing awareness around early cancer detection.

Moreover, government policies particularly in countries like Germany are becoming increasingly supportive of oncology drug development and access. However, the region faces challenges, notably the high cost of oncology treatments, which can strain public health budgets and limit affordability in some countries, along with strict regulatory hurdles that can slow down the approval of new drugs.

The Asia-Pacific (APAC) region is widely recognized as the fastest-growing market for oncology drugs, with growth expected to continue at a strong compound annual rate over the coming years. This surge is being driven by a rising cancer burden across the region, fueled by lifestyle changes, aging populations, and environmental factors.

Countries like China, India, and those in Southeast Asia are making significant strides in improving healthcare infrastructure, expanding access to advanced medical facilities, and investing heavily in early diagnosis and treatment. At the same time, growing disposable incomes are allowing more patients to afford modern cancer therapies, while government initiatives focused on awareness, screening, and support programs are further boosting demand.

The region’s cost advantages also play a key role clinical trials in countries like India can be 40–50% cheaper than in Western nations, making APAC an attractive destination for pharmaceutical R&D. Additionally, there’s a strong emphasis on generics and biosimilars, which help make treatments more affordable and widely accessible. China is expected to dominate in market share, while Japan continues to lead in advanced research and innovation, and India sees rapid growth in both patient numbers and clinical trial activity. Despite the momentum, the region faces challenges such as the high cost of innovative therapies, fragmented healthcare systems in some countries, and a complex, varied regulatory environment.

The Middle East and Africa (MEA) region represents a developing oncology drugs market with promising growth potential, especially in the Middle East. The cancer burden in the region is rising steadily, driven by factors such as changing lifestyles, an aging population, and better diagnostic capabilities. As awareness grows and the need for effective, cost-efficient treatments increases, countries across the region are investing in upgrading healthcare infrastructure.

Governments are playing a pivotal role, launching ambitious healthcare transformation initiatives and public awareness campaigns such as breast cancer awareness efforts in the UAE to promote early detection and treatment. The adoption of advanced therapies, including innovative immunotherapies like checkpoint inhibitors, is accelerating, particularly in GCC countries such as Saudi Arabia, the UAE, and Kuwait. Among them, Saudi Arabia is projected to see the highest growth in breast cancer drug adoption.

Despite these advancements, the region faces several challenges, including uneven healthcare infrastructure, especially in parts of Africa, limited access to high-cost treatments, and the widespread use of generics and biosimilars, which, while improving affordability, can also impact market growth in some premium segments. Nevertheless, MEA remains a region with strong long-term potential as healthcare systems continue to evolve and access to care improves.

The oncology cancer drugs market was valued at USD 206.125 billion in 2024.

The oncology cancer drugs market is projected to grow at a CAGR of 18.3% from 2025 to 2033.

The Targeted drugs segment holds the largest oncology cancer drugs market share.

Asia-Pacific region is expected to witness the highest growth rate.

The oncology cancer drugs market’s major players include F. Hoffmann-La Roche Ltd., AbbVie Inc., Novartis AG, Pfizer Inc., and Bristol-Myers Squibb Company.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Oncology Cancer Drugs Market, By Drug Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Oncology Cancer Drugs Market, By Cancer Type

5.3 Oncology Cancer Drugs Market, By Therapy Type

5.4 Oncology Cancer Drugs Market, By Route of administration

5.5 Oncology Cancer Drugs Market, By Distribution Channel

6.1 North America Oncology Cancer Drugs Market, By Country

6.1.1 Oncology Cancer Drugs Market, By Drug Type

6.1.1 Oncology Cancer Drugs Market, By Cancer Type

6.1.1 Oncology Cancer Drugs Market, By Therapy Type

6.1.2 Oncology Cancer Drugs Market, By Route of Administration

6.1.3 Oncology Cancer Drugs Market ,By Distribution Channel

6.2 U.S.

6.2.1 Oncology Cancer Drugs Market, By Drug Type

6.2.1 Oncology Cancer Drugs Market, By Cancer Type

6.2.1 Oncology Cancer Drugs Market, By Therapy Type

6.2.2 Oncology Cancer Drugs Market, By Route of Administration

6.2.3 Oncology Cancer Drugs Market ,By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping