Online Pharmacy Market

Online Pharmacy Market Share & Trends Analysis Report, By Medicine Type (Over‑the‑Counter (OTC), Prescription Medicines), By Platform Type (Mobile, Desktop), By Product Type (Medications, Health & Wellness Nutrition, Personal Care & Essentials, Others), By Delivery Method (Home Delivery, Click‑and‑Collect), By End User (Individual Consumers, Healthcare Institutions), By Distribution Channel (Direct-to-Consumer, Partnered Retail Pharmacy Networks)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

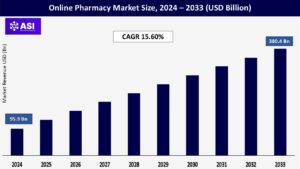

CAGR: 15.60%

Last Updated : December 3, 2025

The global Online Pharmacy Market size was valued at approximately USD 95.9 billion in 2024 and is projected to reach USD 380.4 billion by 2033, growing at a CAGR of 15.60% during the forecast period (2025–2033). The Online Pharmacy Market refers to digital platforms and e-commerce businesses that sell pharmaceutical drugs and healthcare products through websites or mobile applications.

These pharmacies offer convenience, accessibility, and often lower prices, enabling patients to order prescription and over-the-counter medications from the comfort of their homes. Key properties of online pharmacies include secure digital prescription handling, fast home delivery, privacy protection, and integration with telemedicine services.

The increasing penetration of the internet and smartphones, combined with rising consumer preference for digital health services, is significantly driving the online pharmacy market. Patients now expect seamless, on-demand access to healthcare products, just like other e-commerce offerings.

With integrated platforms combining prescription uploads, teleconsultation, and doorstep delivery, online pharmacies are bridging gaps in accessibility especially in rural and remote areas. This digital transformation is further accelerated by tech-savvy younger populations and increased trust in online transactions post-COVID-19.

The global rise in aging populations and chronic conditions such as diabetes, cardiovascular diseases, and arthritis is fueling the demand for regular medication refills.

Online pharmacies cater to this demographic by offering subscription-based models, medication reminders, and contactless delivery reducing the need for frequent pharmacy visits. This convenience factor, combined with cost savings from generic alternatives, promotes continued growth in this market.

Despite rapid growth, the online pharmacy sector faces significant regulatory hurdles that vary across regions and countries. Many nations lack clear, standardized guidelines for operating digital pharmacies, which leads to legal ambiguities and enforcement challenges.

Issues such as verifying prescriptions, preventing the sale of counterfeit or unapproved drugs, and ensuring patient data security are critical concerns. Moreover, cross-border sales of medications through online platforms can lead to violations of drug control laws. These compliance uncertainties can deter new entrants, restrict market expansion, and erode consumer trust if not properly addressed.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Medicine Type |

Over‑the‑Counter (OTC) Prescription Medicines |

| By Platform Type |

Mobile Desktop |

| By Product Type |

Medications Health & Wellness Nutrition Personal Care & Essentials Others |

| By Delivery Method |

Home Delivery Click‑and‑Collect |

| By End User |

Individual Consumers Healthcare Institutions |

| By Distribution Channel |

Direct-to-Consumer Partnered Retail Pharmacy Networks |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Online Pharmacy Market is segmented by Medicine Type, Platform Type, Product Type, Delivery Method, End User and Distribution Channels. Each factor plays a crucial role in improving healthcare accessibility, enhancing medication adherence, and streamlining the supply chain for both prescription and over-the-counter drugs.

These drivers collectively support the widespread adoption of digital pharmacy services, reduce healthcare delivery gaps, and empower patients with safer, faster, and more convenient options for managing their medical needs especially in underserved or remote areas.

OTC medicines form a significant share of the online pharmacy market due to ease of purchase without prescriptions. Products like pain relievers, cold medications, and antacids are highly demanded by consumers seeking convenience, especially during seasonal illnesses.

Prescription drugs account for higher-value sales and are increasingly supported by e-prescription technologies and doctor consultations via telehealth. This segment is growing rapidly as trust in digital prescription fulfillment rises.

Mobile With smartphone penetration and mobile app usability on the rise, the mobile platform dominates in terms of daily user interactions. Mobile apps offer features like repeat ordering, notifications, chatbots, and wallet integration, enhancing user experience.

Desktop While less dominant than mobile, desktops are still preferred for placing large or bulk orders, particularly by older consumers or institutional buyers who may require a more detailed view of products.

Medications The core of the online pharmacy market, including both prescription and OTC drugs. This segment benefits from chronic disease management, elderly care, and recurring purchases.

Health & Wellness Nutrition Includes vitamins, supplements, protein powders, and herbal remedies. Growing health awareness and preventive healthcare trends are boosting this segment. Personal Care & Essentials Items like skincare, hygiene products, and baby care essentials fall under this.

Consumers prefer ordering these items online for convenience and access to wider brands. Others Includes diagnostic tools (e.g., glucometers, thermometers) and medical devices. As consumers turn toward home-based health monitoring, this segment is gaining traction.

Home Delivery The dominant delivery model offering ultimate convenience. Fast, contactless, and often free delivery makes it attractive for both medications and wellness products, especially in urban areas.

Click-and-Collect Preferred by consumers who want flexibility to order online and pick up at a nearby partner pharmacy. This method balances convenience with immediacy, useful in urgent situations.

Individual Consumers The largest end-user group. Individuals rely on online pharmacies for recurring prescriptions, wellness products, and convenience-based purchases.

Healthcare Institutions Includes clinics, small hospitals, and elderly care centers using online pharmacies for bulk ordering or specific medicine needs. This segment is smaller but growing as B2B models evolve.

Direct-to-Consumer Online platforms that sell directly to customers via websites or apps. Dominant in the market, offering better margins, faster service, and data-driven personalization.

Partnered Retail Pharmacy Networks These involve collaborations between digital platforms and brick-and-mortar pharmacies to fulfill prescriptions faster, increase coverage, and improve trust among consumers. It is a growing model blending digital convenience with local accessibility.

North America, particularly the United States and Canada, holds a significant share of the global online pharmacy market due to its advanced digital infrastructure, high healthcare expenditure, and a well-established e-commerce ecosystem.

The region benefits from strong regulatory support for telemedicine and electronic prescriptions, which enhances patient trust in ordering medications online.

Key players such as CVS Health, Amazon Pharmacy, and Walgreens Boots Alliance are rapidly expanding their digital footprint. The increasing prevalence of chronic diseases and rising demand for home-based healthcare solutions further drive market growth in this region.

Europe is another major market, driven by a growing aging population, favorable government policies, and high internet penetration. Countries like Germany, the UK, and Sweden are witnessing a surge in e-pharmacy adoption, aided by the formalization of digital prescription systems such as Germany’s eRezept.

Strict regulations on online drug sales ensure safety and boost consumer confidence. The presence of pan-European online pharmacies and regional collaborations also supports cross-border pharmaceutical trade and service integration.

Asia Pacific is the fastest-growing region in the online pharmacy market, fueled by the expansion of digital health initiatives, rising smartphone use, and increased healthcare access in emerging economies such as India, China, and Southeast Asia.

Government programs promoting e-health platforms, along with public-private partnerships, are accelerating growth. India, in particular, has seen a boom in online pharmacies like 1mg, Netmeds, and PharmEasy, especially after the COVID-19 pandemic.

Despite regulatory challenges in some countries, increasing consumer awareness and investment in health tech startups are unlocking the region’s vast potential.

Latin America is experiencing moderate but steady growth in the online pharmacy sector. Countries like Brazil, Mexico, and Argentina are expanding their e-commerce and telemedicine frameworks, allowing online pharmacies to reach more patients, especially in urban areas.

However, limited digital infrastructure in rural zones and inconsistent regulatory policies across countries pose challenges. The market is evolving through partnerships between local pharmacies and logistics providers to enable timely medicine delivery and improve access to essential healthcare products.

The Middle East & Africa region is in the early stages of online pharmacy adoption, with growth driven by urbanization, mobile health initiatives, and a growing middle-class population. Countries like the UAE and Saudi Arabia are leading in digital health investments, where government backing and private healthcare providers are expanding online medicine services.

In Africa, progress is slower but promising, with startups leveraging mobile platforms to improve medicine distribution and address chronic shortages. However, infrastructural gaps and low digital literacy remain key barriers to broader market penetration.

The market was valued at USD 95.9 billion in 2024.

The market is projected to grow at a CAGR of 15.60% from 2025 to 2033.

Over‑the‑Counter (OTC) hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include CVS Health, Walgreens Boots Alliance and Amazon Pharmacy.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Online Pharmacy Market, By Medicine Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Online Pharmacy Market, By Platform Type

5.3 Online Pharmacy Market, By Product Type

5.4 Online Pharmacy Market, By Delivery Method

5.5 Online Pharmacy Market, By End User

5.6 Online Pharmacy Market, By Distribution Channel

6.1 North America Online Pharmacy Market , By Country

6.1.1 Online Pharmacy Market, By Medicine Type

6.1.2 Online Pharmacy Market, By Platform Type

6.1.3 Online Pharmacy Market, By Product Type

6.1.4 Online Pharmacy Market, By Delivery Method

6.1.5 Online Pharmacy Market, By End User

6.1.6 Online Pharmacy Market, By Distribution Channel

6.2 U.S.

6.2.1 Online Pharmacy Market, By Medicine Type

6.2.2 Online Pharmacy Market, By Platform Type

6.2.3 Online Pharmacy Market, By Product Type

6.2.4 Online Pharmacy Market, By Delivery Method

6.2.5 Online Pharmacy Market, By End User

6.2.6 Online Pharmacy Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping