Ophthalmic Operating Room Microscope Market

Ophthalmic Operating Room Microscope Market Share & Trends Analysis Report, By Product Type (On‑Casters, Wall‑Mounted, Table‑Top, Ceiling‑Mounted), By Application (Cataract Surgery, LASIK, Keratoplasty, Trabeculectomy, Other Ophthalmic Procedures), By End‑User (Hospitals & Clinics, Ambulatory Surgical Centers)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

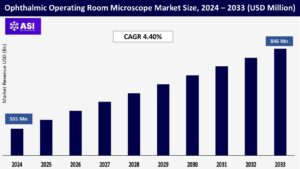

CAGR: 4.40%

Last Updated : December 16, 2025

The global Ophthalmic Operating Room Microscope Market size was valued at approximately USD 555 million in 2024 and is projected to reach USD 846 million by 2033, growing at a CAGR of 4.40% during the forecast period (2025–2033).

The Ophthalmic Operating Room Microscope Market refers to the global market for high-precision surgical microscopes specifically designed for ophthalmic (eye-related) surgeries. These microscopes provide enhanced visualization of minute structures in the eye, which is crucial during delicate procedures such as cataract surgery, retinal detachment repair, and corneal transplants.

Key uses include magnifying the surgical field, improving depth perception, and enabling surgeons to perform intricate tasks with precision. Essential properties of these microscopes include high-resolution optics, superior illumination systems (often LED or halogen), motorized zoom and focus capabilities, and ergonomic designs to reduce surgeon fatigue.

Advanced models may also offer digital imaging integration, 3D visualization, and heads-up displays. The market is driven by increasing incidences of age-related eye disorders, technological advancements, and growing demand for minimally invasive ophthalmic procedures.

One of the major drivers of this market is the growing global burden of ophthalmic disorders such as cataracts, glaucoma, age-related macular degeneration (AMD), and diabetic retinopathy. According to the World Health Organization (WHO), cataracts remain the leading cause of blindness worldwide.

As the aging population increases, especially in developed and emerging economies, the demand for ophthalmic surgeries continues to rise, which in turn fuels the need for high-quality operating room microscopes that enhance surgical precision.

The evolution of microscope technologies such as the integration of 3D visualization, heads-up displays, optical coherence tomography (OCT), and fluorescence-guided imaging has significantly improved the capabilities and outcomes of ophthalmic surgeries.

Surgeons now benefit from better ergonomics, digital integration for teaching and documentation, and automated functionalities. These technological innovations make advanced operating room microscopes more attractive, driving adoption among hospitals and specialty eye clinics.

One of the most significant restraints in this market is the high capital investment required for advanced ophthalmic operating room microscopes. These systems are often equipped with high-end technologies such as digital imaging, 3D visualization, and integrated heads-up displays, which significantly drive up their cost.

For smaller eye care centers, clinics in low- and middle-income countries (LMICs), or public healthcare institutions with limited budgets, such investments may not be feasible. Additionally, the cost of maintenance, servicing, and the need for skilled personnel to operate these microscopes can further limit adoption, especially in resource-constrained environments.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

On‑Casters Wall‑Mounted Table‑Top Ceiling‑Mounted |

| By Application |

Cataract Surgery LASIK Keratoplasty Trabeculectomy Other Ophthalmic Procedures |

| By End‑User |

Hospitals & Clinics Ambulatory Surgical Centers |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Ophthalmic Operating Room Microscope Market is segmented by Product Type, Application and End User. Each factor plays a crucial role in improving surgical precision, enhancing patient outcomes in ophthalmic procedures, and advancing the adoption of minimally invasive techniques in the treatment of vision-threatening conditions such as cataracts, glaucoma, and retinal disorders.

The market is divided into On-Casters, Wall-Mounted, Table-Top, and Ceiling-Mounted microscopes. Among these, On-Casters microscopes account for the largest market share due to their mobility, ease of use, and flexibility, making them highly suitable for multi-procedure ophthalmic operating rooms.

Ceiling-Mounted microscopes are gaining traction in technologically advanced surgical environments, offering seamless integration with other surgical equipment and enhanced visualization, though their high installation costs may limit their use to larger hospitals.

Wall-Mounted and Table-Top microscopes are more common in smaller clinical settings or for minor procedures, where space optimization and basic functionality are key requirements.

The market is segmented into Cataract Surgery, LASIK, Keratoplasty, Trabeculectomy, and Other Ophthalmic Procedures. Cataract surgery dominates the segment due to the high global prevalence of cataracts, especially among the elderly population, and the increasing preference for minimally invasive surgical techniques that demand advanced visualization tools.

LASIK surgeries represent a significant portion as well, supported by rising demand for refractive error correction and the popularity of elective eye procedures in urban areas. Meanwhile, Keratoplasty and Trabeculectomy are driven by the increasing incidence of corneal diseases and glaucoma, respectively, requiring precise microsurgical intervention.

The “Other Procedures” category, including retinal surgeries and vitrectomies, is steadily expanding due to technological advancements in ophthalmic imaging and the growing number of complex cases being treated surgically.

The market is segmented into Hospitals & Clinics and Ambulatory Surgical Centers (ASCs). Hospitals and clinics lead the segment due to their broad service offerings, greater surgical volumes, and ability to invest in advanced surgical infrastructure.

These facilities often perform complex surgeries that require high-end microscopes with superior imaging and ergonomic features. On the other hand, Ambulatory Surgical Centers are emerging as a high-growth segment owing to the rising preference for cost-effective, outpatient ophthalmic procedures, particularly in developed regions where healthcare systems are shifting toward value-based care. ASCs increasingly invest in compact, high-performance microscopes suitable for quick-turnaround procedures like cataract and LASIK surgeries.

North America dominates the market due to its well-established healthcare infrastructure, high prevalence of age-related eye diseases like cataracts and macular degeneration, and strong adoption of minimally invasive surgical techniques. The presence of leading manufacturers, technological innovation, and high surgical volumes in the U.S. and Canada drive consistent growth.

Europe holds a significant share, supported by a robust public healthcare system, increasing demand for ophthalmic surgeries, and investments in surgical technology. Countries like Germany, France, and the UK are leading adopters. Rising awareness of early eye disease diagnosis and treatment fuels adoption of high-end ophthalmic microscopes.

Asia-Pacific is the fastest-growing market, driven by a rapidly aging population, increasing cases of cataracts and diabetic retinopathy, and government-led blindness prevention initiatives. India, China, and Japan are key contributors. Expanding private healthcare and a growing number of eye care centers further support market expansion.

Growth in Latin America is steady, led by Brazil and Mexico, where urban hospitals and private clinics are adopting modern surgical microscopes. However, economic disparities and limited access in rural areas slow down market penetration.

This region is in the early growth stage, with investments in healthcare infrastructure and medical tourism in Gulf countries (UAE, Saudi Arabia) creating demand. In Africa, lack of funding and skilled professionals hampers growth, though initiatives to improve eye care access are emerging.

The ophthalmic operating room microscope market was valued at USD 555 Million in 2024.

The ophthalmic operating room microscope market is projected to grow at a CAGR of 4.40% from 2025 to 2033.

The On‑Casters hold the largest ophthalmic operating room microscope market share.

The North America region is expected to witness the highest growth rate.

Major players include Carl Zeiss Meditec AG, Leica Microsystems (Danaher Corporation) and Topcon Corporation.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Ophthalmic Operating Room Microscope Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Ophthalmic Operating Room Microscope Market, By Application

5.3 Ophthalmic Operating Room Microscope Market, By End‑User

6.1 North America Ophthalmic Operating Room Microscope Market, By Country

6.1.1 Ophthalmic Operating Room Microscope Market, By Product Type

6.1.2 Ophthalmic Operating Room Microscope Market, By Application

6.1.3 Ophthalmic Operating Room Microscope Market, By End‑User Industry

6.2 U.S.

6.2.1 Ophthalmic Operating Room Microscope Market, By Product Type

6.2.2 Ophthalmic Operating Room Microscope Market, By Application

6.2.3 Ophthalmic Operating Room Microscope Market, By End‑User Industry

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping