Opioids Market

Opioids Market Share & Trends Analysis Report, By Product Type (Oxycodone, Codeine, Methadone, Morphine, Fentanyl, etc. (Oxycodone and Fentanyl are notable for their market share and potency, respectively)), By Application (Pain Management (dominates the market), Diarrhoea Treatment, Cough Treatment, Anesthesia), By Route of Administration (Injectable, Oral) By Distribution Channel (Retail Pharmacies (largest share), Hospital Pharmacies, Others) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

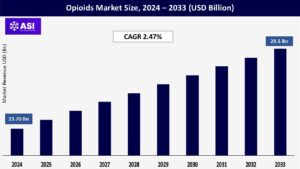

CAGR: 2.47%

Last Updated : March 27, 2026

The global opioids drugs market size was valued at approximately USD 23.70 billion in 2024 and is projected to reach USD 29.5 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 2.47% during the forecast period of 2025–2033.

The global opioids market is expected to grow steadily between 2025 and 2033, reflecting a broader shift in healthcare needs. This growth is largely fueled by the rising number of people living with chronic pain, especially as populations age and age-related conditions become more common. Additionally, as medical advancements lead to more surgical procedures being performed, there’s an increasing demand for effective post-operative pain relief. Together, these trends are driving a sustained need for opioid medications, positioning the market for continued expansion over the coming years.

As the world’s population continues to age, more people are living with chronic, often debilitating conditions like arthritis, osteoporosis, and other degenerative diseases that bring persistent pain. This demographic shift naturally fuels the demand for effective pain relief, with opioids remaining a critical option for managing severe cases. At the same time, chronic illnesses such as cancer, fibromyalgia, and neuropathic pain are becoming increasingly common, and for many patients, especially those for whom other treatments fall short, opioids offer essential relief and a better quality of life. The growing number of surgical procedures, thanks to medical advancements and improved access to healthcare, also drives the use of opioids for post-operative pain management.

Additionally, everyday life still brings accidents, sports injuries, and unexpected traumas that result in acute pain, often requiring strong analgesics during recovery. Together, these medical realities ensure that opioids continue to play a significant role in pain management, despite the broader concerns surrounding their use.

In the ongoing effort to balance effective pain relief with safety concerns, pharmaceutical innovation has focused heavily on extended-release (ER) and long-acting (LA) opioid formulations. These versions are designed to provide consistent, long-term pain control with fewer doses, making it easier for patients to stick to their treatment plans and experience more stable relief. At the same time, abuse-deterrent formulations (ADFs) have emerged as a response to the rising concerns around opioid misuse. Engineered to be harder to crush, dissolve, or inject, these formulations aim to reduce the potential for abuse while still serving patients in genuine need. For doctors and patients, ADFs offer a sense of reassurance, presenting a “safer” alternative to traditional opioids.

For pharmaceutical companies, these innovations not only align with regulatory expectations but also open doors to new patents and periods of market exclusivity, making them both a public health response and a business opportunity.

The opioid crisis has evolved into a deeply personal and societal tragedy, marked by high rates of misuse, addiction, and overdose deaths, especially in North America, where its toll is felt in homes, hospitals, and communities. Beyond the statistics, these losses have fueled widespread stigma and a growing mistrust of opioid medications. As public awareness grows through media coverage, advocacy campaigns, and the voices of those affected, society has become increasingly wary of overreliance on these drugs. This heightened scrutiny has triggered calls for safer alternatives and tighter regulations.

Meanwhile, the crisis has also rippled through the economy, reducing labor force participation and increasing healthcare costs for employers. The resulting strain on productivity and financial stability adds yet another layer of urgency, making it clear that the opioid epidemic is not just a medical issue, but a public, social, and economic one.

In response to the growing opioid crisis, governments and regulatory bodies, especially in the United States, have taken decisive steps to tighten control over how these medications are prescribed and monitored. Stricter guidelines now limit both the dosage and duration of opioid prescriptions, while also requiring doctors to closely monitor patients to help prevent misuse.

Tools like Prescription Drug Monitoring Programs (PDMPs) have become essential in tracking prescriptions across providers, making it far more difficult for individuals to obtain multiple opioid prescriptions from different sources. At the same time, there’s been a push for the development of abuse-deterrent formulations (ADFs), which are designed to reduce the potential for misuse.

While these formulations represent progress, they also come with significant research and development costs that can burden manufacturers. Adding to the complexity, regulatory agencies such as the FDA are under increasing pressure to rethink how opioids are evaluated and approved, leading to a more cautious, tightly controlled environment for new products in this space.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Oxycodone Codeine Methadone Morphine Fentanyl (Oxycodone and Fentanyl are notable for their market share and potency, respectively) |

| By Application |

Pain Management (dominates the market) Diarrhoea Treatment Cough Treatment Anesthesia |

| By Route of Administration |

Injectable Oral |

| By Distribution Channel |

Retail Pharmacies (largest share) Hospital Pharmacies Others |

| Key Players |

Johnson & Johnson Services, Inc. (Janssen Pharmaceutical Companies) Pfizer, Inc. AbbVie Inc. Hikma Pharmaceuticals PLC Sun Pharmaceutical Industries Ltd. Grünenthal Mallinckrodt Endo International Plc Teva Pharmaceutical Industries Ltd. Collegium Pharmaceutical Inc. Daiichi Sankyo Inc. Lupin Ltd. Acura Pharmaceuticals Inc. Assertio Therapeutics Inc. Biodelivery Sciences International Inc. Cipher Pharmaceuticals Inc. Egalet Corp. Kempharm Inc. Lannett Co. Inc. Viatris Inc. (formed from the merger of Mylan N.V. and Upjohn, a Pfizer division) Pernix Therapeutics Roxane (a subsidiary of Boehringer Ingelheim, though their opioid portfolio has shifted) Actavis (now part of Teva Pharmaceuticals) Watson (now part of Teva Pharmaceuticals) Lavipharm Labs Noven Aveva Nesher Ranbaxy (now part of Sun Pharmaceutical Industries) Rhodes Impax (now part of Amneal Pharmaceuticals) Aveo Pharmaceuticals |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Opioids Market is categorized by product type, by application, by route of administration, and by distribution channel. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. The opioid market is a complex landscape, highly influenced by ongoing debates surrounding pain management, addiction, and regulatory policies.

A closer look at the opioids market by drug type reveals just how complex and varied this space really is. Opioids come in many forms: natural, semi-synthetic, and synthetic, each with unique roles in medicine and, in some cases, in the opioid crisis itself. Natural opiates, like morphine and codeine, are derived directly from the opium poppy. Morphine remains a cornerstone for managing severe pain, especially in hospitals and palliative care, while codeine is more commonly used for mild to moderate pain or as a cough suppressant. Semi-synthetic opioids such as oxycodone, hydrocodone, hydromorphone, and buprenorphine are created by chemically modifying natural opiates.

Oxycodone and hydrocodone are among the most widely prescribed opioids and have played central roles in both pain management and the opioid crisis. Buprenorphine stands out for its dual use: it not only treats pain but is also a key medication for opioid use disorder (OUD). Its ability to reduce cravings and withdrawal symptoms without producing a full opioid high makes it a cornerstone of modern addiction treatment. Synthetic opioids are fully lab-made and often much more potent. Fentanyl is the most notable and widely used in hospitals for severe or cancer-related pain. However, its illicit form is driving a staggering number of overdose deaths worldwide. Methadone, another synthetic, is used both for long-term pain and as a long-acting treatment for OUD.

Tramadol is a milder synthetic option often prescribed for moderate pain, especially in settings where stronger opioids are restricted. Other highly potent synthetics like sufentanil, remifentanil, and nitazenes are used in surgical settings or, increasingly, turning up in illegal drug supplies, raising new public health concerns. Some key trends are shaping the future of these drug types.

There’s a noticeable shift toward abuse-deterrent formulations (ADFs), which are designed to make it harder to misuse opioids by crushing or injecting them. Meanwhile, oxycodone and fentanyl continue to dominate in terms of medical use and potency. And as the opioid crisis evolves, so does the demand for OUD treatment medications, with buprenorphine and methadone seeing significant growth as they become central tools in combating addiction. Altogether, this segmental view highlights not only the diversity of opioids available but also how each type plays a distinct role in both healthcare and the ongoing public health response to opioid misuse.

When it comes to how opioids are used, the market is largely shaped by the medical conditions they’re meant to treat, and pain management leads the way by a wide margin. The vast majority of opioid prescriptions are written to help patients cope with pain, though the reasons for that pain vary widely. Pain management itself can be broken down into several categories. Acute pain, like what follows surgery, injury, or dental work, often calls for short-term opioid use.

Chronic pain, such as back pain, arthritis, or nerve damage, presents a more complex challenge. While opioids have traditionally played a role here, there’s growing concern over their long-term use, especially for non-cancer-related pain. That said, cancer pain remains a vital and expanding area where opioids are considered essential for relieving the intense discomfort many patients experience during treatment or at the end of life. Another key application is anesthesia, where opioids like fentanyl and sufentanil are used during surgeries to manage pain and keep patients comfortable. As the number of surgeries performed globally continues to rise, so too does the demand for opioids in this setting.

In more specialized uses, cough suppression remains relevant, with medications like codeine and hydrocodone helping patients manage severe, persistent coughing. Opioids for diarrhea treatment, though less well-known, are also part of the picture. Medications like loperamide slow down gut movement and can help in severe cases, though they are typically used with caution due to potential misuse. Perhaps the most dynamic and fast-growing segment is opioid use disorder (OUD) treatment. With the opioid crisis affecting millions worldwide, there’s been a major push to expand access to medications like buprenorphine and methadone, which help people recover by reducing cravings and withdrawal symptoms. This part of the market is seeing rapid growth, driven by policy changes, increased awareness, and greater investment in addiction treatment.

In summary, while pain management continues to dominate the opioids market, the way it’s approached is changing, especially for long-term, non-cancer pain. At the same time, the rising use of opioids in anesthesia and the critical expansion of OUD treatment signal how the market is adapting to meet both clinical needs and public health priorities.

When it comes to how opioids are delivered to patients, the route of administration plays a big role in how the medication works, how quickly it acts, and how it fits into a patient’s daily life or treatment plan.

Oral opioids, whether in tablets, capsules, or liquid form, are by far the most common and preferred option, especially for managing chronic pain and for many opioid use disorder (OUD) treatments. Their convenience and ease of use make them especially appealing for both patients and healthcare providers, and this segment is expected to see the fastest growth moving forward. Injectable opioids, delivered through intravenous, intramuscular, or subcutaneous routes, are typically used in hospitals and emergency settings, where rapid relief is essential, such as during surgeries or for managing severe, acute pain.

Long-acting injectable versions of medications like buprenorphine and methadone are also gaining ground in OUD treatment, offering sustained benefits with fewer dosing requirements. Historically, this segment has held a large market share due to its vital role in hospital care. Transdermal patches, such as those containing fentanyl, provide a steady release of medication over time and are increasingly being used for chronic pain, especially when oral options aren’t suitable. They offer a balance of sustained relief with lower maintenance for patients.

Sublingual and buccal formulations, which dissolve under the tongue or against the cheek, are especially common for buprenorphine-based OUD treatments. These methods offer reliable absorption and are easier for many patients to take than pills or injections, making them a popular alternative. Other routes, like intranasal sprays for breakthrough cancer pain or epidural/intrathecal injections for localized pain relief, serve more niche but important roles in specialized care settings. A few major trends are shaping this landscape.

There’s growing innovation in long-acting formulations, including extended-release tablets and once-monthly injectable options that aim to improve patient compliance and reduce the risk of misuse. Meanwhile, oral and injectable forms continue to dominate the market due to their versatility and widespread use across both acute and chronic care. Overall, the delivery method is more than just a technical detail it affects everything from treatment success to patient experience, and it’s increasingly a focus for innovation in both pain management and addiction treatment.

How opioids reach patients, whether for pain relief or addiction treatment, depends a lot on the distribution channel, and each plays a unique role in shaping access and oversight. Retail pharmacies remain the biggest player in the space. These are your local drugstores where most prescription opioids are filled for outpatient use. Their accessibility and convenience make them the primary source for opioid dispensing, especially for individuals managing chronic pain at home. However, because of their central role in past overprescribing trends, retail pharmacies are now under much tighter scrutiny. Regulatory bodies are keeping a close eye on how, when, and to whom opioids are being dispensed, pushing for more responsible practices.

Hospital pharmacies are another major channel, focused on dispensing opioids for inpatients typically after surgeries, during emergency care, or for managing severe conditions. These settings rely heavily on injectable or fast-acting opioids, and use is usually closely monitored by healthcare professionals. Online pharmacies are a growing segment, offering convenience for patients, but because opioids are controlled substances, these platforms are subject to strict regulations. There’s potential here for improved access, particularly for people in remote areas, but safeguards are essential to prevent misuse.

Specialty clinics and treatment centers, especially those focused on opioid use disorder (OUD), are becoming increasingly important. Medications like methadone can only be dispensed through highly regulated treatment programs, and buprenorphine, while more flexible, is still often managed through specialized providers. The expansion of these treatment centers reflects a broader shift toward addressing addiction as a healthcare issue and ensuring people who need help can access it through trusted, regulated channels.

Overall, as the landscape evolves, we’re seeing a mix of tightened controls, especially in retail settings, alongside growing investment in addiction treatment infrastructure. It’s a balancing act: ensuring opioids remain accessible for legitimate medical needs while preventing the misuse that has fueled a global crisis.

The regional landscape of the opioids market paints a complex and often paradoxical picture. Around the world, there’s a clear and growing need for effective pain relief, but it’s accompanied by deep concerns about addiction, misuse, and public health. North America stands out as the largest market, but it also bears the brunt of the opioid crisis, prompting major investments in treatment for opioid use disorder (OUD) and a push toward safer, non-opioid alternatives.

In contrast, the Asia Pacific region is on a rapid growth trajectory, driven by its large population and expanding healthcare infrastructure. Europe maintains a more cautious balance, striving to manage pain effectively while staying alert to the dangers of illicit opioid use. Meanwhile, Latin America and the Middle East & Africa are still emerging markets, working to improve access to essential pain medications without repeating the pitfalls seen elsewhere. This global view underscores the challenge of meeting legitimate medical needs while safeguarding public health.

North America continues to dominate the global opioids market, often accounting for nearly half or even more of global revenues. This prominence is largely tied to a high prevalence of chronic pain, an advanced healthcare system, and a long history of relatively liberal opioid prescribing practices. The region’s aging population, more prone to chronic conditions, further fuels demand for pain management solutions.

However, North America also finds itself at the heart of the global opioid crisis. The widespread misuse of opioids, including the alarming rise of illicit fentanyl, has led to soaring addiction and overdose rates. In response, the region has seen a wave of reforms, stricter prescribing guidelines, enhanced monitoring programs, and a strong emphasis on abuse-deterrent formulations (ADFs) that make opioids harder to misuse. There’s also been a major push to invest in treatments for opioid use disorder (OUD), such as buprenorphine and naltrexone, alongside a growing shift toward non-opioid alternatives for managing pain.

Within the region, the United States leads both in market size and in the intensity of the crisis, driving many of the regulatory and therapeutic advancements. Canada is facing similar challenges and has adopted comparable harm reduction and treatment strategies. Mexico, while primarily known as a source and transit route for illicit opioids, is now seeing its own concerns rise over prescription opioid use, though its market dynamics remain distinct.

This complex picture reflects a region grappling with the dual need to manage pain effectively while preventing the devastating consequences of opioid misuse.

Europe holds the position as the second-largest player in the global opioids market, shaped by its ongoing need for pain management, an aging population, and a well-established healthcare system. While prescription opioids are used cautiously, the region faces significant challenges from the illicit drug landscape, particularly heroin, which remains a major issue in many areas.

In recent years, there’s also been a troubling rise in the use of diverted prescription drugs and potent new synthetic opioids like nitazenes. European countries tend to take a more cautious and controlled approach to opioid prescribing than what was historically seen in the U.S., striving to strike a careful balance between managing pain and preventing misuse. There’s a growing awareness of the risks associated with opioids, and many countries are expanding access to treatments for opioid use disorder, including methadone and buprenorphine programs.

While the medical opioid market in Europe is relatively stable, it’s far from stagnant. Policymakers and healthcare providers continue to adapt to emerging drug trends, strengthening efforts to ensure responsible prescribing and improving support for those affected by opioid-related harms. This reflects a region focused on maintaining medical access while actively responding to evolving public health risks.

The Asia Pacific region is quickly emerging as the fastest-growing market for opioids, particularly in the area of opioid use disorder (OUD) treatment. This rapid growth is driven by a combination of factors unique to the region. With a massive and still-growing population, there’s a rising demand for pain relief, especially as cases of cancer and musculoskeletal conditions become more common. At the same time, healthcare infrastructure is improving across many countries, making treatments more accessible than ever before. Economic growth is also playing a role, as higher disposable incomes in many parts of the region are allowing more people to seek medical care and access prescribed medications. In addition, Asia Pacific, especially India and China, has established itself as a powerhouse in generic pharmaceutical manufacturing, including opioids, which helps reduce costs and expand availability.

However, as access grows, so does the need for oversight. Some countries in the region are beginning to tighten regulations around opioid use to prevent misuse and mirror lessons learned from other parts of the world. Adding complexity to the picture is Myanmar, which has recently become a major producer of illicit opium, raising concerns about the impact on both regional and global illicit opioid markets. Overall, the Asia Pacific region represents a dynamic mix of opportunity and challenge as it navigates the balance between meeting legitimate medical needs and addressing the risks of opioid misuse.

The Middle East and Africa (MEA) currently represent a smaller share of the global opioids market, but momentum is building, particularly in the area of opioid use disorder (OUD) treatment. This diverse region includes countries with varying levels of healthcare infrastructure and regulation, but many are taking meaningful steps forward. Demand for pain management is rising as more people face chronic health conditions and undergo surgical procedures, creating a growing need for effective pain relief. At the same time, the region is contending with its own opioid-related challenges, especially the misuse of tramadol in parts of North and West Africa. Global trafficking routes have also made MEA vulnerable to the spread of illicit opioids.

As healthcare systems continue to develop and awareness of pain management improves, access to prescription opioids is expected to expand. While MEA’s market share remains modest compared to other regions, its trajectory suggests steady growth ahead, driven by both medical need and ongoing efforts to address misuse responsibly.

The market was valued at USD 23.7 billion in 2024.

The market is projected to grow at a CAGR of 2.47% from 2025 to 2033.

Injectables segment holds the largest market share.

North America region is expected to witness the highest growth rate.

Major players include Mallinckrodt Pharmaceuticals, Endo Pharmaceuticals Inc, Purdue Pharma LP, Pfizer, Inc., Teva Pharmaceutical Industries Limited, C.H. Boehringer Sohn Ag and Ko. Kg, AstraZeneca Plc, Sanofi S.A., Sun Pharmaceuticals, Johnson & Johnson, Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Opioids Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Opioids Market, By Application

5.3 Opioids Market, By Route of Administration

5.4 Opioids Market, By Distribution Channel

6.1 North America Opioids Market, By Country Type

6.1.1 Opioids Market, By Product Type

6.1.2 Opioids Market, By Application

6.1.3 Opioids Market, By Route of Administration

6.1.4 Opioids Market, By Distribution Channel

6.2 U.S.

6.2.1 Opioids Market, By Product Type

6.2.2 Opioids Market, By Application

6.2.3 Opioids Market, By Route of Administration

6.2.4 Opioids Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping