Oxo Alcohol Market

Oxo Alcohol Market Size, Market Share & Trends Analysis Report By Type (Isobutanol, 2-Ethylhexanol, n-Butanol, Others), By Application (Plasticizers, Acetates, Glycol Ethers, Solvents, Adhesives, Others), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2032

Report Code : ASICMR1015

CAGR: 5.2%

Last Updated : February 2, 2026

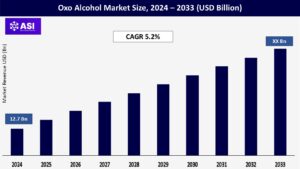

The global oxo alcohol market was valued at approximately USD 12.7 billion in 2024 and is projected to reach USD XX billion by 2033, growing at a steady CAGR of 5.2% during the forecast period (2026–2033).

Oxo alcohols are widely used in producing plasticizers, solvents, adhesives, and other industrial applications due to their versatility, chemical stability, and excellent solvency properties. The increasing demand for plasticizers in the construction and automotive industries and the growing use of solvents in paints and coatings is driving market growth.

Key growth drivers include the expansion of end-use industries, advancements in production technologies, and the rising demand for sustainable and bio-based oxo alcohols, contributing to the steady expansion of the oxo alcohol market size.

Oxo alcohols, particularly 2-ethylhexanol, are extensively used in the production of plasticizers such as phthalates, which are essential for manufacturing flexible PVC products. The construction industry’s increasing demand for PVC in pipes, cables, and flooring, along with the automotive sector’s need for lightweight and durable materials, is propelling the oxo alcohol market. According to the International Energy Agency (IEA), global construction activity is expected to grow by 3.5% annually, while automotive production is projected to rise by 4% annually, further boosting demand and supporting sustained oxo alcohol market growth.

Oxo alcohols such as n-butanol and isobutanol are key ingredients in solvents used in paints, coatings, and inks. The growing construction and automotive industries, along with increasing urbanization, are driving the demand for high-performance coatings, thereby fueling the oxo alcohol market.

Innovations in oxo alcohol production, including the development of bio-based and sustainable manufacturing processes, are enhancing market growth. For instance, the U.S. Department of Agriculture (USDA) has invested in research programs focused on bio-based chemicals, including oxo alcohols, to reduce dependency on fossil fuels. These innovations are expected to accelerate oxo alcohol market growth over the forecast period.

The Oxo Alcohol Market faces significant challenges due to volatility in raw material prices and stringent environmental regulations, which are impacting market stability and growth. The production of oxo alcohols heavily relies on petrochemical feedstocks such as propylene and syngas, making the market highly susceptible to fluctuations in crude oil prices. Supply chain disruptions, geopolitical tensions, and economic uncertainties further exacerbate price volatility, creating challenges for manufacturers to maintain competitive pricing and profitability. This instability in raw material costs can hinder market growth, particularly for small and medium-sized enterprises with limited financial resilience.

In addition to raw material price volatility, the oxo alcohol market is grappling with stringent environmental regulations. Regulatory restrictions on the use of certain plasticizers, such as phthalates, due to their potential health and environmental risks, pose significant challenges. Phthalates, which are widely used in flexible PVC applications, have come under scrutiny for their potential adverse effects on human health and the environment.

Governments and regulatory bodies worldwide are implementing stricter guidelines to limit the use of hazardous chemicals, compelling manufacturers to invest in the development of eco-friendly alternatives. While this shift toward sustainable solutions presents long-term opportunities, it also increases production costs and requires significant R&D investments in the short term.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Isobutanol 2-Ethylhexanol n-Butanol Others |

| By Application |

Plasticizers Acetates Glycol Ethers Solvents Adhesives Others |

| Key Players |

BASF SE Dow Inc. Eastman Chemical Company LG Chem Arkema Group ExxonMobil Chemical Evonik Industries AG Mitsubishi Chemical Corporation OXEA GmbH Perstorp Holding AB |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

2-Ethylhexanol is the dominant segment in the oxo alcohol market share, accounting for over 32.9% of the global share in 2024. It is primarily used in the production of plasticizers, especially for flexible PVC applications. Flexible PVC is widely used in construction (pipes, cables, flooring) and automotive (interiors, wiring) industries, making 2-ethylhexanol a vital component in these sectors.

n-Butanol is gaining significant traction due to its extensive use in solvents, coatings, adhesives, and industrial cleaners. It is a versatile chemical with excellent solvency properties, making it ideal for applications in the paints & coatings industry.

Isobutanol is projected to witness significant growth during the forecast period, driven by its application in biofuels and as a solvent in industrial processes. It is increasingly being used as a biofuel additive due to its high energy content and compatibility with existing fuel infrastructure. Its use in the production of coatings, inks, and resins also contributes to its rising demand.

The Oxo Alcohol Market is segmented by application into plasticizers, solvents, adhesives, glycol ethers, acetates, and others, with each segment playing a critical role in driving demand across various industries. Plasticizers held the largest market share in 2024, primarily due to their extensive use in the production of flexible PVC, which is widely utilized in construction, automotive, and consumer goods. The growing demand for lightweight, durable, and flexible materials in these industries has been a key driver of this segment.

For instance, flexible PVC is essential for manufacturing pipes, cables, flooring, and automotive interiors, making plasticizers the dominant application of oxo alcohols. The construction and automotive sectors, in particular, are expected to continue fueling this demand, with global construction activity projected to grow at a CAGR of 3.5% and automotive production rising by 4% annually.

Solvents are another significant application segment, expected to register steady growth over the forecast period. Oxo alcohols such as n-butanol and isobutanol are widely used as solvents in paints, coatings, inks, and industrial cleaners. The expansion of the paints and coatings industry, driven by increasing construction activities and automotive production, is a major growth driver for this segment. Additionally, the rising demand for high-performance and eco-friendly solvents is further boosting the market.

Adhesives and glycol ethers are emerging as key application segments, driven by advancements in adhesive formulations and the growing demand for eco-friendly chemicals. Oxo alcohols are used in the production of industrial and consumer adhesives, including construction adhesives, automotive adhesives, and packaging adhesives. The adoption of lightweight materials in the automotive and construction industries is contributing to the growth of this segment. Similarly, glycol ethers, which are derived from oxo alcohols, are widely used in paints, coatings, cleaning products, and printing inks. The increasing demand for high-performance and environmentally friendly chemicals in these applications is driving the growth of glycol ethers.

Other applications, such as acetates, are also gaining traction, particularly in pharmaceuticals, cosmetics, and food additives. The development of high-purity and bio-based oxo alcohols for specialized applications is expected to further drive growth in this segment.

North America accounted for 22.5% of the global oxo alcohol market share in 2024, driven by strong demand from the construction, automotive, and paints & coatings industries. The U.S. is a key contributor, with significant investments in bio-based oxo alcohol production.

Europe held xx% of the market share in 2024, supported by stringent environmental regulations and the region’s focus on sustainable chemical production. Germany and France are major markets, particularly for plasticizers and solvents.

Asia-Pacific is projected to register the highest CAGR of 6.5% during the forecast period, driven by rapid industrialization, urbanization, and infrastructure development. China and India are leading markets, with China dominating due to its large-scale manufacturing and construction activities. These factors are expected to significantly increase the oxo alcohol market size across the Asia-Pacific region.

Middle East and Africa are emerging markets, with increasing investments in petrochemical production and infrastructure projects. Saudi Arabia and the UAE are key contributors. Ongoing investments are supporting the gradual expansion of the oxo alcohol market size in these emerging economies.

Latin America is witnessing steady growth, with Brazil and Mexico leading the market due to their expanding automotive and construction sectors.

The global oxo alcohol market was valued at approximately USD 12.7 billion in 2024.

The market is projected to grow at a steady CAGR of 5.2% during the forecast period from 2026 to 2033.

2-Ethylhexanol is the dominant type, accounting for over 32.9% of the global market share in 2024, primarily due to its use in plasticizers for flexible PVC products.

North America, Europe, and Asia-Pacific are key regions, with Asia-Pacific expected to register the highest CAGR of 6.5% due to rapid industrialization, urbanization, and infrastructure development.