Personal Mobility Devices Market

Personal Mobility Devices Market Share and Trend Analysis, By Technology Type (Manual Mobility Devices, Powered Mobility Devices, Hybrid and Smart Mobility Devices), By Application (Healthcare Facilities, Home Care, Community and Public Use, Travel and Tourism, Sports and Recreation), By End User (Elderly Individuals, People with Disabilities, Rehabilitation Patients, Institutional Users, Young and Active Users) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.89%

Last Updated : April 6, 2026

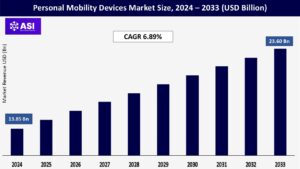

The global personal mobility devices market size was valued at USD 13.85 billion in 2024 and is projected to reach USD 23.60 billion by 2033, expanding at a compound annual growth rate CAGR of 6.89% during the forecast period (2025–2033).

Personal mobility aids (PMDs) are a broad category of aid equipment designed to enhance the quality of life and autonomy of individuals with impaired mobility. PMDs such as mobility scooters, wheelchairs, walking sticks, rollators, and other aids enable disabled individuals, the elderly, and those recovering from surgery or injury to access facilities.

Their main purpose is to enable people to move around freely and independently, either in the home, care homes, or in the community. The expanding market is driven by an aging population worldwide, rising levels of chronic illness and disability, and improved device technology.

Government incentives rising, improved health infrastructure, and rising awareness of accessibility requirements further bolstered the high level of uptake of personal mobility devices uptake. With emerging technology, PMDs are becoming more adaptive, smart-enabled, and accessible, thereby becoming more popular and utilized across all ages.

The strongest driver of the personal mobility devices market is the rapidly increasing elderly population worldwide. The longer human life lasts, the greater is the proportion of people with mobility impairment as a result of aging. Old individuals suffer from illnesses like osteoporosis, arthritis, and weaker muscles, limiting their independence of movement.

The population trend of the elderly has created a steady demand for mobility assistance devices that make older individuals independent and able to participate in the full activities of daily living. Beyond the age consideration, there is also the rising number of disabilities from chronic diseases, injury, and neurological diseases.

Stroke, spinal cord injury, and degenerative disease are increasingly affecting more patients with long-term mobility needs. Urgency for better-quality, comfortable, and effective mobility aids has created steady growth and development in the PMD industry.

As the citizens become increasingly aware of the benefits of mobility aids, patients and caregivers demand solutions that enhance the quality of life, reduce the risk of falls, and aid in rehabilitation. Overall, the effect of these trends is a robust, growing market for personal mobility devices all over the world.

The personal mobility industry has witnessed a series of technological innovations that have revolutionized user experience and product performance. Adoption of light materials technology, foldable frames, and ergonomic design has provided easier portability, comfort, and simplicity of usage for PMDs.

Incorporation of smart technology, including GPS sensors, Bluetooth sensors, and health monitoring sensors, has also contributed to the increased popularity of modern PMDs. Electric scooters and wheelchairs, for example, have been designed with more durable batteries, adjustable seats, and simple control panels with regard to varying users’ comfort and needs.

Robotics and automation are also developing, with certain products auto-leveling or sensing obstructions to ensure safety and convenience. Such technology not only improves the quality of everyday life for consumers but also heightens the likelihood of PMD use for community care, rehabilitation, and home care.

As more investment from producers is directed into R&D, the industry is seeing highly niche products being introduced for specific conditions, age, and lifestyle. The result is an exciting and diverse market with ongoing innovation driving expansion and reacting to evolving users’ needs.

While the future appears bright, the personal mobility products market carries the downside of affordability and accessibility. High-end mobility products, especially those with new technology or custom features, are prohibitively expensive and inaccessible to the majority of consumers.

Insurance coverage and government subsidies vary significantly geographically, with some possessing too few funds to obtain the equipment that they need. The problem is exacerbated even further in middle- and low-income countries through inferior healthcare infrastructure, absence of skilled professionals, and delivery logistics.

Even in industrialized economies, access is disproportionately distributed, with rural and lower socioeconomic communities usually facing longer waiting times and fewer options. Over-cost of maintenance, repair, and replacement parts are some of the cost burdens to users and caregivers.

All of these may lead to nonuse of the mobility devices, decreased independence, and decreased quality of life among affected groups. In order to overcome such impediments, policymakers, producers, and healthcare managers must collaborate to make mobility items less expensive, easier to get reimbursed for, and more available.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology Type |

Manual Mobility Devices Powered Mobility Devices Hybrid and Smart Mobility Devices |

| By Application |

Healthcare Facilities Home Care Community and Public Use Travel and Tourism Sports and Recreation |

| By End User |

Elderly Individuals People with Disabilities Rehabilitation Patients Institutional Users Young and Active Users |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Private mobility aids are segmented by type of technology and engineering of the design therefor. Motorized aids such as the classic wheelchair, walker, and cane remain in demand because they are inexpensive and simple to use.

These tools are mainly light in weight, low maintenance, and suitable for users of impaired upper body strength. Power tools such as electric wheelchairs and mobility scooters have found wide application with people with disability in mobility or endurance. The tools enable the users to enjoy more independence since they are able to travel long distances at minimal body effort.

As technology has evolved, hybrid devices that involve hand as well as power elements have been designed with the feature of versatility to serve the majority of the requirements of the users. Intelligent PMDs with sensors, networked, and automated can potentially create a new market segment, such as real-time health monitoring, navigation support, and distance control capability.

The technology of choice is dependent on preference, physical ability, and intentional use environment. With increasing innovation, the market is likely to be diversified with the new technology focusing on specific issues and widening the scope.

Personal mobility device use covers the widest use spans, demonstrating diversity in need being addressed by users. Medical application of PMDs is paramount in hospitals, rehabilitation centers, and extended care facilities to offer patients mobility, recovery, and independence.

Home care is a priority application as well, whereby technology supports patients with daily living tasks, mobility in their own homes, and reduces caregiver dependency. Public and communal spaces, such as shopping malls, parks, and terminals, increasingly accommodate accessible facilities and hire out equipment for mobility aids to make social participation and inclusion easier.

Travel and tourism usage of PMDs has also gained commonality, with tourist locations, resorts, and airports offering mobility aids to boost the tourist experience. Recreation and sports is a specialty application, with adaptive equipment specially adapted for participation in sports like wheelchair racing or basketball.

Every use environment has unique demands for device portability, durability, and customization, and so it is not easy for manufacturers to develop customized solutions that address the varied demands of more than one setting and user group.

The consumer market for personal mobility devices is broad and diverse, and encompasses all age groups and demographic populations. The most important user group are the elderly because of the commonality and frequently rising mobility disability associated with rising age.

People with congenital or acquired disabilities rely on PMDs to attain independent living and participate in everyday activities. Patients recovering from surgery, illness, or injury might use mobility aids temporarily as a part of convalescence. Caregivers and healthcare workers are also instrumental stakeholders who select and employ devices among institutionally living patients.

The market has grown over the last three years with increasing numbers of youth consumers, particularly those with sports injuries or chronic illness, seeking lifestyle-sensitive, stylish, and discreet devices.

Institutional customers such as rehabilitation clinics, nursing homes, and hospitals have also been significant players in the market, purchasing the products in bulk to assist with addressing their clients’ needs. The range of end users highlights offering a vast amount of products, features, and sizes to meet various needs and wants.

North America leads the world in the market for mobility devices for personal use due to its advanced healthcare infrastructure, wide awareness, and government-free subsidies. Huge availability of an elderly population and full insurance coverage offer growing demand for mobility scooters, wheelchairs, and walking aids.

Mass manufacturers also dominate the space, as well as distribution channels. Technology of powered mobility solutions and investments in smart assistive technology are also the reasons behind regional dominance. The Americans with Disabilities Act (ADA) laws also provide accessibility of facilities to the private and public sector, thereby increasing the use of mobility devices.

Europe boasts the largest worldwide market share of personal mobility aids because of better healthcare infrastructures as well as subsidies offered by the government on disabled and elderly persons. Advance reimbursement tactics such as in Germany, France, and the UK drive discovery of assistive devices in the continent.

Emphasis on inclusivity and quality of life drives adoption in rural and urban regions with equal vigor. Growth in the ageing population and concerted efforts of EU member states towards accessibility harmonization are the driving forces for the gradual growth of the market. Furthermore, campaigns for barrier-free environments demand high-tech, ergonomic mobility devices.

The Asia Pacific leads all other regions in personal mobility equipment market growth owing to rising healthcare spending, the expanding middle-class consumer, and rising rates of disability. Global statistics are documenting historic progress in healthcare units and legal availability in nations such as China, India, and Japan.

Urbanization and the growing number of ageing citizens are inspiring the government to spend on public mobility aid devices. Finally, technology penetration and low-cost domestic production are rendering devices economical. National health schemes and NGO schemes involving elder care and disability care fuel the growth of the market, with the Asia Pacific region emerging as a land of hope.

Middle East Africa, and Latin America is a promising market for the personal mobility devices market but is behind in the development of infrastructure and cost.

Latin America’s Brazil and Mexico are experiencing moderate growth based on the rising awareness levels of the masses as well as growing initiatives of the government and nongovernment institutions towards disability-impaired mobility support.

In the Middle East, the Gulf nations are driving accessibility in city planning and spending on healthcare to international norms. In Africa, NGOs and international health organizations are providing mobility aids regardless of economic hardship. As a whole, the region is hopeful as it slowly sees demand increasing.

The global Personal Mobility Devices Market was valued at USD 13.85 billion in 2024.

The market is projected to grow at a CAGR of 6.89 % from 2025 to 2033.

Powered personal mobility devices hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Sunrise Medical, Invacare Corporation, Pride Mobility Products Corp., Ottobock, Permobil, Medline Industries, Drive DeVilbiss Healthcare, Karman Healthcare, Hoveround Corporation, GF Health Products.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Personal Mobility Devices Market, By Technology Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Personal Mobility Devices Market, By Application

5.3 Personal Mobility Devices Market, By End User

6.1 North America Personal Mobility Devices Market, By Country

6.1.1 Personal Mobility Devices Market, By Technology Type

6.1.2 Personal Mobility Devices Market, By Application

6.1.3 Personal Mobility Devices Market, By End User

6.2 U.S.

6.2.1 Personal Mobility Devices Market, By Technology Type

6.2.2 Personal Mobility Devices Market, By Application

6.2.3 Personal Mobility Devices Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping