Pet Oral Care Products Market

Pet Oral Care Products Market Share and Trend Analysis, By Formulation Type (Dental Chews, Toothpaste, Mouthwash/Rinse, Toothbrushes, Veterinary Products), By Indication (Dogs, Cats, Other Animals), By End User (Households (Individual Consumers), Veterinary Clinics, Pet Grooming Salons Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 5.4%

Last Updated : April 6, 2026

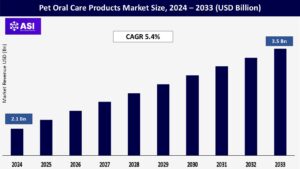

The global pet oral care products market size was worth USD 2.1 billion in 2024 and is expected to reach USD 3.5 billion by 2033 at a CAGR of 5.4% for the forecast period (2024–2033).

To avoid plaque, tartar deposits, and periodontal disease, pet oral care involves maintaining pets’ healthy teeth through specific products such as toothpaste, toothbrushes, dental chews, water additives, and oral rinses.

Neglect of oral hygiene has a direct correlation with systemic disease risks, such as liver, kidney, and cardiovascular disease, that shorten lifespans and increase veterinary costs. It is therefore important. To minimize these risks, veterinarians recommend annual professional cleanings and daily preventive care such as brushing or feeding enzymatic dental chews.

The growing application of these approaches is due to the growing awareness and desire among pet owners for fast, delicious solutions that can be accommodated within their busy lifestyles, like flavored toothpaste or water supplements that reduce plaque.

As a reaction to trends like pet humanization, where owners give high importance to quality-based, health-oriented care that is on par with human standards, innovations focus on natural ingredients and pet-friendly formulations.

Coverage of the teeth is increasingly being provided by insurance providers, emphasizing its status as a requirement for medical care, and educational promotions across online media and veterinary guidance further mainstream oral health habits. This unified approach aims to ensure pets’ long-term well-being and quality of life by bringing owner education together with scientifically formulated products.

Pets have joined the family circle as a result of the worldwide boom in the number of pets, particularly among millennials and Gen Zers, which has raised the demand for advanced medical procedures such as dental treatment.

Pets are now owned by over 70% of US households, and since their owners value longevity and quality of life, their expenditure on premium health products has gone up greatly. This cultural shift, termed “pet humanization,” is a mirror of human health trends as owners seek products that are both functional and pet-friendly, such as mint-flavored toothpaste, finger brushes made from silicone, and dental toys.

Increased disposable incomes and urbanization create the ability to purchase specialized products that adhere to human-grade wellness levels, such as ultrasonic toothbrushes or organic dental chew. By drawing attention to the fact that if left untreated, plaque can lead to life-threatening illnesses such as sepsis or heart disease, social media and pet influencer campaigns increase awareness.

As an illustration, studies have found that animals with poor oral health are 30% more likely to contract systemic infections. Today, businesses focus predominantly on ease of use through water additives or dissolveable oral strips that simplify everyday tasks for busy owners.

Product innovation, health-consciousness prevention, and emotional bonding all join forces to drive market growth, particularly in North America and Europe, where premiumization forces are at work.

Since dental diseases occur in 80% of animals aged more than three, the most widespread being periodontal disease, veterinary endorsement remains an important factor in market growth. Diseases such as gingivitis and tooth resorption are common and may pass unnoticed until they induce pain, loss of teeth, and secondary infection in organs such as the liver and kidneys.

Dental checkups are being given priority at clinics because, per veterinary associations, 70% of cats and 50% of dogs have signs of dental disease by two years of age. With frequent use, experts now suggest specifically targeted products that can lower plaque by as much as 60%, including enzymatic gels, chlorhexidine rinses, and prescription dental diets.

Veterinarian-branded association has legitimized products such as Vetradent and Greenies, causing owner confidence to grow. In addition, pet dental extractions and cleanings are now under pet insurance, which reduces financial hesitation.

In the developing world, clinics stock affordably priced products such as bamboo toothbrushes or herbal dental powders, and veterinary outreach programs teach owners how to brush. Oral health is today an institution of modern pet medicine as a result of the synergy between clinical expertise, increasing disease prevalence, and easily affordable solutions, encouraging adoption across socioeconomic levels.

Because they are expensive and have uneven penetration, premium pet oral care products, such as veterinarian-recommended enzymatic toothpaste and dental chews, have significant adoption hurdles. Such items are often viewed as luxuries in cost-conscious regions of India, Brazil, and Southeast Asia, where basic necessities receive greater emphasis than oral hygiene.

Middle-class pet owners are dismayed that a single clinically proven dental chew might be three to five times more expensive than ordinary supplies. Even in advanced markets, pet owners opt for generic products because of economic pressures, increasing the periodontal disease risk.

Other challenges to emerging economies are fragmented distribution systems, limited access to veterinarians, and cultural attitudes that give low priority to oral health. In Sub-Saharan Africa, for example, fewer than 20% of dog owners utilize specialized products; rather, they utilize ineffective substitutes, such as hard kibble.

Trust is eroded by local, cheap substitutes without scientific backing. To enhance affordability, brands are introducing trial-sized packaging, tiered pricing, and partnerships with clinics.

Meanwhile, attempts are underway to alter attitudes via grassroots education and localized dissemination, stressing the linkages between preventable diseases and oral health. Millions of animals will be in jeopardy of preventable ailments if they are not addressed by systemic measures to decrease costs and improve awareness.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Formulation |

Dental Chews Toothpaste Mouthwash/Rinse Toothbrushes Veterinary Products Other Product Types (e.g., wipes, gels, water additives) |

| By Application |

Dogs Cats Other Animals |

| By End User |

Households (Individual Consumers) Veterinary Clinics Pet Grooming Salons |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

As dental chews bring in 36% of total revenue in 2024, they lead the worldwide pet oral care market. Their status as a treat and functional benefit, such as reducing plaque with chewing action, is the reason for their popularity. Pets find the taste of chicken or peanut butter, and their teeth are scrubbed by rough textures.

For enhanced effectiveness, many products now include additional vitamins, enzymes, or breath-freshening agents. Another significant class is toothpaste for pets, specifically designed to be swallowed safely. Rather than employing hazardous chemicals, these products combat bacteria with enzymes or natural agents such as parsley or neem.

Along with brushes that fit different mouth sizes, beef or fish flavors encourage brushing acceptance in pets. Because they offer low-effort solutions for challenging-to-brush pets, oral rinses and water additives are increasingly popular. Added to water or applied to gums, they reduce bacteria and bad breath.

Ergonomic handles maximize the user’s grasp, and manual toothbrushes remain necessary for deep cleaning. High-strength gels and other professional products are employed by veterinary clinics for serious dental issues. Fast hygiene solutions are offered by ancillary items such as dental wipes or sprays, which complete a comprehensive line of products.

In 2024, dogs will comprise 66% of the pet oral care market, and they will dominate the application segment. This is prompted by the high incidence of periodontal disease among dogs, since studies have shown that over 80% of dogs have dental issues when they reach the age of three.

Preventive treatment is accorded high priority by the owners, a factor that makes owners keen to develop breed-specific measures. And while soft-bristled brushes are suitable for small dogs with sensitive gums, bigger breeds need chews that are extra-tough and will not be broken by serious chewing.

When playing, dental toys with ridges and grooves also help reduce plaque. Cats achieve gingivitis or periodontitis in 90% of them by age four and thus represent a notable secondary percentage. Alternatives like enzymatic gels on gums or abrasive-textured kibble that clean teeth during meals have developed due to their resilience against traditional brushing.

Taking advantage of cats’ enjoyment of strong-smelling odors, fish-flavored toothpaste, and lickable dental treats boosts compliance. The exotic pet niche market, birds, reptiles, and rabbits, is increasing steadily. Water additives are utilized by birds to minimize bacterial buildup in their oral cavities, while small mammals that are subject to overly long teeth, like guinea pigs, make use of chews that are composed of fibrous hay.

Reptilian owners are seeking more sprays that have been advocated by veterinarians in order not to incur mouth infections. Though smaller than dog and cat markets, this segment is growing as more individuals keep exotic pets and as specialty products are spread more widely by internet pet communities and veterinary communications.

Pet owners integrate oral health into their daily practices to prevent expensive veterinary visits, and homes remain the largest end-user market. The accessibility of dental chews, toothpaste, and water additives makes them appealing, and subscription boxes ensure consistent availability.

To spur sales, stores make dental products available in combinations with food or toys. At checkups, veterinary clinics also play a critical role by providing professional-strength products such as prescription toothpaste or chlorhexidine rinses.

As a means of building trust through expert guidance, clinics often pair product sales with dental cleanings or procedures. By incorporating activities such as using pet-safe toothpaste or antimicrobial sprays when grooming, grooming salons assist. Leverage their customers’ trust, and some salons market travel-sized oral hygiene kits to maximize sales.

Pet stores allot dental products ample shelf space, supported by in-store demonstrations or educational displays highlighting the long-term health benefits. As pet ownership by the middle class rises and veterinary infrastructure increases, growth opportunities exist in Asian and Latin American emerging markets.

Moreover, social media promotions and workshops organized by veterinarians raise awareness, particularly in regions where preventive dental care was previously overlooked. Market penetration is also hastened by cross-channel cooperation, including sales of veterinarian-approved products through retail outlets.

North America leads the world in the pet oral care market with sophisticated veterinary care, strong consumer education, and high pet ownership (70% of US homes have pets). High-end product success, such as dental chews and enzyme toothpaste, is driven by trends toward pet humanization.

Subscription models and veterinarian-recommended brands drive sales. The increase in demand for grain-free and organic dental treats finds expression in Canada. While price consciousness across lower-income groups hinders premium products’ adoption, regulatory focus on pet well-being, along with comprehensive retail infrastructure, further cements geographical leadership.

Pet-holding homes amount to 50% here, with Germany, the UK, and France at the helm. Stringent EU regulations ensure the safety of products, making consumers more confident about using water additives and dental chews. Environmental consumers demand natural ingredients and eco-friendly packaging.

The market in Eastern Europe grows slowly via online pet care platforms, but is behind because of less disposable income. Senior dental care is more in demand because the region has an aging pet population, and partnerships between veterinarians and retailers increase market penetration.

Asia Pacific is growing rapidly, particularly in China and Japan, where there is growing pet ownership in urban areas. Middle-class expansion in Southeast Asia and India drives demand for affordably priced products such as simple brushes and dental wipes. Availability is enhanced through websites such as JD.com and Chewy, but pet dental care resistance remains cultural.

With ultra-high-tech products such as ultrasonic toothbrushes, Japan leads the way in technical innovation. In spite of challenges such as poor veterinary infrastructure and counterfeit products in rural regions, the increasing popularity of pet insurance indicates long-term potential.

Expansion is uneven within Latin America, the Middle East, and Africa. With increasing middle-class pet ownership and dental services provided by veterinary clinics, Brazil and Mexico are the champions of Latin America. The acceptance of high-end products is hindered by financial insecurity, which prefers cheap chews.

Urbanization and expat needs are propelling activity in the Middle East, most notably the United Arab Emirates and Saudi Arabia. Market depth is constrained by low awareness. With little product availability beyond South Africa, Africa remains in its early stages. Both regions rely on imports, but in a bid to transcend financial and cultural hurdles, there are local brands beginning to spring up.

The market was valued at USD 2.1 billion in 2024.

The market is projected to grow at a CAGR of 5.4% from 2025 to 2033.

Chews hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Mars, Virbac, Purina.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Pet Oral Care Products Market, By Formulation

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Pet Oral Care Products Market, By Application

5.3 Pet Oral Care Products Market, By End User

6.1 North America Pet Oral Care Products Market, By Country

6.1.1 Pet Oral Care Products Market, By Formulation

6.1.2 Pet Oral Care Products Market, By Application

6.1.3 Pet Oral Care Products Market, By End User

6.2 U.S.

6.2.1 Pet Oral Care Products Market, By Formulation

6.2.2 Pet Oral Care Products Market, By Application

6.2.3 Pet Oral Care Products Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping