Petroleum Liquid Feedstock Market

Petroleum Liquid Feedstock Market & Trends Analysis Report, By Type (Naphtha, Gas Oil, Others), By End-Use (Petrochemical Industry, Refineries, Others), By Application (Ethylene Production, Propylene & Benzene Derivatives, Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

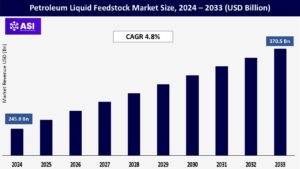

CAGR: 4.8%

Last Updated : February 6, 2026

The global Petroleum Liquid Feedstock Market size was valued at approximately USD 245.8 billion in 2024, and is projected to reach USD 370.5 billion by 2033, growing at a CAGR of 4.8% during the forecast period (2025–2033).

These feedstocks, primarily naphtha and gas oil, are essential raw materials for the petrochemical industry, enabling the production of ethylene, propylene, and other key compounds. Market growth is fueled by increasing demand for plastics, chemicals, and transportation fuels across emerging economies and rising investments in downstream processing infrastructure.

The use of petroleum liquid feedstocks is driven by expanding demand for polymers and specialty chemicals worldwide, especially in the Asia-Pacific region.

For the production of base chemicals like ethylene, propylene, and benzene, which are necessary building blocks for plastics, synthetic rubbers, and resins, these feedstocks are vital. The need for feedstock is being significantly increased by ongoing petrochemical growth projects in the Middle East, China, and India.

In developing nations, the demand for consumer goods, automotive products, construction materials, and packaging, all of which rely significantly on petrochemical derivatives, is expanding due to rapid industrialization and the expansion of the middle class.

The use of petroleum liquid feedstocks in the manufacturing and infrastructure sectors is rising dramatically as a result of this economic momentum, especially in nations like Brazil, India, and Southeast Asia.

The market pricing of petroleum liquid feedstocks is extremely sensitive to changes in the price of crude oil globally since these feedstocks are directly produced from crude oil.

The availability of feedstock, prices, and overall production planning for downstream businesses can all be significantly impacted by factors like OPEC+ production decisions, geopolitical conflicts, and interruptions in global supply chains.

Rising environmental concerns, tightening emission laws, and worldwide decarbonization pledges are prompting sectors to move away from fossil-based feedstocks.

The demand for traditional petroleum liquid feedstocks is long-term threatened by the growing use of biobased and renewable alternatives, particularly in developed economies.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Naphtha Gas Oil Others |

| By End-Use |

Petrochemical Industry Refineries Others |

| By Application |

Ethylene Production Propylene & Benzene Derivatives, Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Petroleum Liquid Feedstock Market is segmented by Type (Naphtha, Gas Oil, Others), By End-Use (Petrochemical Industry, Refineries, Others), By Application (Ethylene Production, Propylene & Benzene Derivatives, Others).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Naphtha – Leading Segment: Because naphtha is widely used in steam cracking processes to produce ethylene, propylene, and other olefins, it has the largest market share. High demand from petrochemical crackers in Asia, particularly in China and India, where capacity expansions are ongoing, is a major factor supporting the segment.

Gas Oil: In order to create important fuels and feedstocks, gas oil is mostly utilized in fluid catalytic cracking (FCC) and hydrocracking facilities. As refinery integration increases and efforts to optimize product yield efficiency increase, so does its demand.

Others (Condensates, Reformates): Feedstocks used in specialized or niche applications, such as reformates and condensates, fall under this category. Refinery configurations, regional availability, and particular end-use requirements all influence their demand.

Petrochemical Industry – Largest Consumer: The petrochemical industry dominates feedstock consumption, with demand driven by rising global plastic usage and expanding chemical trade. Key end users include large integrated petrochemical companies and standalone chemical manufacturers, particularly in Asia-Pacific and the Middle East.

Refineries: Integrated refining complexes are increasingly optimizing their configurations to produce higher-value petrochemical feedstocks such as naphtha and gas oil. This strategic shift enhances profit margins and supports downstream chemical production.

Others (Energy Sector, Export-Oriented Plants): This category includes merchant suppliers catering to third-party facilities, energy-sector applications, and export-oriented plants supplying feedstocks to petrochemical hubs across regions like Northeast Asia and Europe.

Ethylene Production – Dominant Application: Since ethylene is a basic monomer used to make plastics, solvents, antifreeze, and detergents, it remains the largest application segment. Naphtha is the main feedstock for steam crackers in Asia, especially in China and India, which contributes significantly to the production of ethylene.

Propylene & Benzene Derivatives: For the production of polypropylene, styrene, phenol, and other derivatives, propylene and benzene are essential intermediates. These chemicals support a strong demand for feedstock and are crucial in consumer electronics, packaging, automotive, and construction applications.

Others (Toluene, Xylene, Butadiene): Toluene, xylene, and butadiene are utilized in the manufacturing of synthetic rubber and specialty chemicals. The expansion of diverse downstream industries like adhesives, paints, synthetic fibers, and elastomers is driving a steady increase in demand.

Asia-Pacific accounted for over 45% of the market share in 2024, led by countries like China, India, Japan, and South Korea. The region’s dominance is driven by the presence of large-scale petrochemical complexes, surging demand for plastics, and supportive industrial policies. Continuous investments in refinery and petrochemical integration further strengthen its position as the global demand center.

Representing approximately 24% of global consumption, North America benefits from advanced refinery infrastructure and abundant shale gas-derived liquids. The United States is a major contributor, with its high domestic production of ethylene and favorable feedstock economics driving market growth.

Europe holds around 18% of the market share, led by Germany, France, and the Netherlands. While the region has a mature petrochemical sector, it is progressively shifting toward low-carbon and sustainable feedstock alternatives due to strict environmental regulations and decarbonization targets.

This region is witnessing rapid infrastructure expansion, particularly in Saudi Arabia and the UAE, where state-owned enterprises are investing in integrated refinery-petrochemical projects. The strategy aims to reduce reliance on crude exports and increase value-added downstream output.

A developing market with moderate growth potential, Latin America is led by Brazil and Argentina. Ongoing government initiatives to modernize refining infrastructure and expand petrochemical capacity support the region’s long-term growth prospects.

The current market size of the Petroleum Liquid Feedstock Market is USD 245.8 billion in 2024.

The expected CAGR from 2025 to 2033 of Petroleum Liquid Feedstock Market is 4.8%.

The Asia-Pacific, with over 45% share, dominates the Petroleum Liquid Feedstock Market.

The major applications are Ethylene, propylene, benzene, toluene, and xylene production.

ExxonMobil, Shell, Reliance Industries, Saudi Aramco, TotalEnergies, and Chevron

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Petroleum Liquid Feedstock Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Petroleum Liquid Feedstock Market, By End-Use

5.3 Petroleum Liquid Feedstock Market, By Application

6.1 North America Petroleum Liquid Feedstock Market , By Country

6.1.1 Petroleum Liquid Feedstock Market, By Type

6.1.2 Petroleum Liquid Feedstock Market, By End-Use

6.1.3 Petroleum Liquid Feedstock Market, By Application

6.2 U.S.

6.2.1 Petroleum Liquid Feedstock Market, By Type

6.2.2 Petroleum Liquid Feedstock Market, By End-Use

6.2.3 Petroleum Liquid Feedstock Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping