Pharmaceutical Plastic Bottles Market

Pharmaceutical Plastic Bottles Market Share & Trends Analysis Report, By Material (Polyethylene (PE), Polyethylene terephthalate (PET), Polyvinyl chloride (PVC), Polypropylene (PP), and Others), By Product Type (Packer Bottles, Dropper Bottles, Solid Containers, Liquid Bottles, Nasal Spray Bottles, and Others), By Capacity (Below 100 ml, 101 ml – 250 ml, and Above 250 ml) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

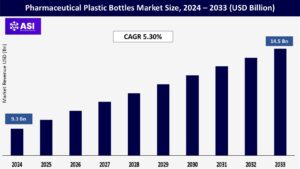

CAGR: 5.30%

Last Updated : August 22, 2025

The global Pharmaceutical Plastic Bottles Market was valued at approximately USD 9.3 billion in 2024 and is projected to reach USD 14.5 billion by 2033, growing at a CAGR of 5.30% during the forecast period (2025–2033).

The pharmaceutical plastic bottles market centers on the design, production, and distribution of durable plastic containers tailored for the secure handling and storage of medicinal products such as pills, syrups, and creams. These bottles are primarily crafted from materials like HDPE, PET, and PP due to their excellent chemical resistance, moisture protection, strength, and lightweight nature. They play a critical role in maintaining medication efficacy, ensuring accurate dosing, and adhering to strict health and safety guidelines. Common features include child-proof caps, tamper-proof seals, and UV-resistant coatings to protect sensitive formulations. Widely adopted across pharmaceutical companies, hospitals, and retail pharmacies, these containers are fundamental in safeguarding drug integrity and promoting safe, user-friendly application and distribution.

The increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer is growing demand for more effective and patient-centric drug delivery systems. With over 537 million adults globally living with diabetes, healthcare systems are turning to innovations like continuous-release insulin pumps. These technologies enhance dosing precision, reduce complications, and have shown to decrease hospital stays by up to 22%, improving both patient outcomes and healthcare cost efficiency. Concurrently, the biologics market is undergoing rapid expansion, with a projected annual growth rate of 9.9%.

This growth underscores the need for specialized drug carriers to protect complex biologic therapies, such as monoclonal antibodies, peptides, and gene-based treatments. Encapsulation technologies such as lipid nanoparticles (LNPs), initially popularized through mRNA COVID-19 vaccines have proven crucial in enhancing the stability and delivery efficiency of sensitive biologics, boosting therapeutic effectiveness by as much as 40%. These dual forces are not only reshaping pharmaceutical development priorities but also accelerating innovation in delivery platforms, such as injectable hydrogels, microneedle patches, and smart inhalers. As treatment regimens become more personalized and complex, drug delivery technologies must evolve to ensure targeted, stable, and efficient therapeutic action, ultimately driving better health outcomes and reducing system-wide burdens.

The evolution of drug delivery is being propelled by a powerful combination of cutting-edge technologies and robust investments in research and development. Technologies such as implantable MEMS devices and polymeric nanoparticles are enabling real-time, precision drug administration, with glucose-sensitive insulin implants alone contributing to an expected nanotech drug delivery market value of $136.8 billion by 2030. These innovations have shown to improve chronic disease outcomes by up to 35%. Simultaneously, increased R&D spending—totaling $238 billion globally in 2022—has driven high-impact partnerships such as Moderna and Catalent’s collaboration in lipid nanoparticle production. These alliances aim to scale manufacturing capacity for advanced therapeutics, including cancer and rare disease treatments, while also accelerating development timelines by 25%. Together, these forces are not only enhancing therapeutic efficacy but also transforming the commercial and regulatory landscape of modern drug delivery.

Different regulatory agencies have different requirements for combination products, such as drug-eluting stents or smart inhalers. For example, the FDA’s 505(b)(2) procedure for drug-device combinations delays launches by up to three years because it requires 18–24 months more safety data than for single-use medications (Straits Research, 2022). As evidenced by the recent delays for a new transdermal pain patch, new Medical Device Regulation (MDR) guidelines in Europe now require 30% more clinical endpoints to approve polymeric matrix implants. Asian-Pacific regulators, on the other hand, frequently demand localized trials, requiring businesses to duplicate research in markets like India and Japan.

Budgets were strained by these issues: after receiving approval in the EU, one company spent $12 million to revalidate a microneedle flu vaccine for Southeast Asia. According to a survey, 45% of manufacturers stated that regulatory uncertainty was the biggest barrier to the adoption of next-generation delivery technology, indicating that such complexities deter investment in high-risk innovation.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Material |

Polyethylene (PE) Polyethylene terephthalate (PET) Polyvinyl chloride (PVC) Polypropylene (PP) Others |

| By Product Type |

Packer Bottles Dropper Bottles Solid Containers Liquid Bottle Nasal Spray Bottles Others |

| By Capacity |

Below 100 ml, 101 ml – 250 ml Above 250 ml |

| Key Players |

Gerresheimer AG Amcor Plc Berry Global Inc. AptarGroup, Inc. Comar, LLC Drug Plastics Group O.Berk Company Alpha Packaging Pretium Packaging Weener Plastics Group Origin Pharma Packaging RPC Group Plc |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Pharmaceutical Plastic Bottles Market is segmented by Material, Product type and Capacity. Each segment plays a vital role in improving packaging efficiency, maintaining product integrity, and meeting industry standards in the pharmaceutical plastic bottles market.

The pharmaceutical plastic bottles market uses different types of plastic depending on the kind of medicine being stored. Polyethylene (PE) is one of the most common plastics. The stronger type, called HDPE, is great for holding tablets and capsules because it keeps out moisture and protects the medicine from damage. The softer type, LDPE, is used for items like dropper and squeeze bottles. PE is popular because it’s cheap, flexible, and works well with many types of medicine. Polyethylene Terephthalate (PET) is another widely used plastic.

It’s clear, strong, and doesn’t break easily, which makes it perfect for storing liquid medicines like syrups. PET also helps protect medicine from air and moisture, keeping it fresh. It’s light and safe to use both at home and in hospitals. Polyvinyl Chloride (PVC) is a plastic that’s clear and resists chemicals, but it’s not used as much because it’s bad for the environment and hard to recycle. Still, it’s used in some cases where you need to clearly see the medicine inside. Polypropylene (PP) is good for bottles that need to be heated or sterilized, like nasal sprays or eye drops. It’s strong, resists chemicals, and is used for both the bottles and their caps. There are also other materials like polystyrene, which is mostly used in labs, and bioplastics like PLA, which are made from plants and are better for the environment. These greener plastics are becoming more popular as companies look for eco-friendly packaging.

The pharmaceutical plastic bottles market is divided into different types of bottles, each made for specific medicines and uses. Packer bottles are mostly used for tablets and capsules. They have tight lids that keep out moisture and dirt, making them good for both over-the-counter and prescription medicines. Dropper bottles are used for medicines for the eyes, ears, and for kids. These bottles let you give the right amount of medicine easily and are made from soft plastics like LDPE or PP so you can squeeze them gently. Solid containers are made for powders and tablets. They are usually made from strong plastics like HDPE or PP that keep moisture away and keep the medicine safe.

Liquid bottles hold syrups and liquid medicines. PET plastic is often used because it’s clear, strong, and doesn’t break easily. These bottles often come with measuring caps or dispensers to help give the right dose. Nasal spray bottles are specially made for sprays that go in the nose. They need to work with spray pumps and be easy to clean. Polypropylene (PP) is used because it is strong and keeps the medicine safe from leaks or germs. The ‘Others’ group includes bottles for creams, injectable medicines (not made of glass), and sample bottles. These come in different shapes and materials depending on what they need to hold.

The pharmaceutical plastic bottles market is divided into different sizes to fit different medicine needs. Bottles smaller than 100 ml are mainly used for kids’ medicines, eye drops, nasal sprays, or samples. These small bottles are common in hospitals and clinics and are good for giving exact small doses and are easy to carry. Bottles that hold between 101 ml and 250 ml are usually for syrups, liquid medicines, and treatments that last a medium amount of time.

They are easy to carry but also hold enough medicine, so they are popular for many over-the-counter liquid medicines. Bottles bigger than 250 ml are mostly used for bulk medicines or in hospitals and clinics. These large bottles work well for long treatments or for families who need many doses. Because they are big, they are made from strong materials and have tight lids to keep the medicine safe.

North America plays a key role in the pharmaceutical plastic bottles market. With a strong healthcare system, high medical spending, and many leading pharmaceutical companies, the region especially the U.S. sees strong demand for over-the-counter drugs and advanced packaging. Strict FDA regulations encourage the use of safe and environmentally friendly plastic bottles.

Europe has a mature and steadily growing market. Nations like Germany, the UK, and France are leading the shift toward recyclable and sustainable packaging. European Union regulations on plastic use are pushing pharmaceutical companies to adopt greener alternatives.

Asia-Pacific is expanding rapidly in this market. Increased drug production in countries like India and China, along with growing healthcare access, is driving demand. Rising populations and government healthcare programs are also contributing. While packaging standards vary, improvements are being made.

Latin America shows moderate growth, with Brazil and Mexico at the forefront due to rising use of common medicines and improved healthcare access. However, challenges such as economic fluctuations and less strict environmental policies may slow down progress. Still, awareness of sustainable packaging is increasing.

Though smaller in size, this market is growing steadily. Increased healthcare infrastructure, government funding, and population growth especially in countries like the UAE, Saudi Arabia, and South Africa are driving demand. Limited local manufacturing and uneven regulation remain challenges, but foreign investments are helping the market advance.

The pharmaceutical plastic bottles market was valued at USD 9.3 billion in 2024.

The market is projected to grow at a CAGR of 5.30% from 2025 to 2033.

The Polyethylene (PE) holds the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Gerresheimer AG, Amcor Plc and Berry Global Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Pharmaceutical Plastic Bottles Market, By Material

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Pharmaceutical Plastic Bottles Market, By Product Type

5.3 Pharmaceutical Plastic Bottles Market, By Capacity

6.1 North America Pharmaceutical Plastic Bottles Market, By Country

6.1.1 Pharmaceutical Plastic Bottles Market, By Material

6.1.2 Pharmaceutical Plastic Bottles Market, By Product Type

6.1.3 Pharmaceutical Plastic Bottles Market, By Capacity

6.2 U.S.

6.2.1 Pharmaceutical Plastic Bottles Market, By Material

6.2.2 Pharmaceutical Plastic Bottles Market, By Product Type

6.2.3 Pharmaceutical Plastic Bottles Market, By Capacity

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping