Pharmacogenomics Market

Pharmacogenomics Market Share and Trend Analysis By Technology (Polymerase Chain Reaction (PCR), DNA Sequencing, Microarray, Electrophoresis, Mass Spectrometry. Others), By Application (Drug Discovery, Tailored Treatment, Oncology. Pain Management, Others), By End-User (Hospitals, Research Institutes, Pharmaceutical Companies, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

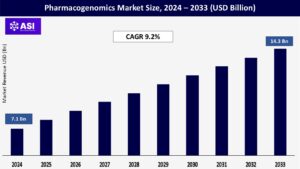

CAGR: 9.2%

Last Updated : April 3, 2026

The global pharmacogenomics market size was valued at USD 7.1 billion in 2024 and is projected to reach USD 14.3 billion by 2033, growing at a CAGR of 9.2% during the forecast period (2025–2033).

Pharmacogenomics enhances drug efficacy and safety by customizing medical interventions to a patient’s genetic profile. It decreases trial-and-error prescribing, minimizes side effects, and improves patient adherence by examining genetic variations that affect drug metabolism and response. As a result, precision medicine is increasingly dependent on it.

Determining the best patient groups for clinical trials, it also helps with drug development. Although it has been connected to cancer, it also helps with pain management, cardiology, and psychiatry. Genetic testing is becoming more accurate and widely available thanks to developments in data tools, portable testing, and DNA analysis.

Thus, genetic infrastructure is being invested in by pharmaceutical companies, researchers, and hospitals. In order to guarantee that treatments meet patient needs, regulators are also revising guidelines to incorporate genetic testing into routine care. Therefore, pharmacogenomics is transforming healthcare, offering safer, cost-effective treatments while strengthening trust in modern medicine.

As healthcare moves away from one-size-fits-all treatments, pharmacogenomics is emerging as a key component of personalized medicine. By examining a patient’s genetic composition, physicians can forecast how they will react to particular medications, enabling more accurate dosage and fewer adverse effects.

Genetic testing, for instance, assists in identifying patients who metabolize drugs too slowly or too quickly, preventing harmful or ineffective treatments. In order to expedite the approval of targeted therapies, regulatory bodies such as the FDA now advise the inclusion of genetic biomarkers in drug labels.

As a result, pharmaceutical companies have made significant investments in companion diagnostics, which are tests created in conjunction with medications to make sure they are appropriate for the right patients. These tests are also being used by labs and hospitals to lower expenses associated with trial-and-error prescribing and enhance the quality of care.

To ensure safer results, antidepressants and blood thinners, for example, now frequently require genetic testing prior to use. Because of this, collaborations between pharmaceutical companies and diagnostic companies are expanding, spurring innovation and market growth.

Pharmacogenomics is a vital tool in contemporary healthcare since patients also benefit from shorter treatment durations and decreased hospitalization risks. The need for individualized approaches will continue to grow as chronic diseases necessitate long-term care, establishing pharmacogenomics as a major market driver.

The need for pharmacogenomics is being driven by the rise in chronic diseases such as diabetes, heart disease, and cancer worldwide. These disorders frequently result in unpredictable outcomes due to intricate interactions between drug responses and genetics.

For instance, genetic factors greatly influence the effectiveness of chemotherapy, and improper dosage can result in serious toxicity. In a similar vein, genetic testing is necessary to guarantee that cardiovascular medications like clopidogrel function as intended.

With chronic diseases causing 86% of global deaths, healthcare systems face pressure to adopt precision tools that reduce hospitalizations and costs. This is addressed by pharmacogenomic testing, which makes customized treatments possible that reduce side effects and enhance adherence.

These days, hospitals incorporate genetic screening into standard care, such as cancer patients’ pre-treatment testing or psychiatric medication dosage modifications. Data demonstrating that tailored strategies lower emergency visits and readmissions lend credence to this change.

Pharmacogenomics-guided treatment, for example, has been shown to reduce adverse drug events by 30 to 50 percent. Its cost-saving potential is also being recognized by governments and insurers, which will result in expanded insurance coverage for tests.

Pharmacogenomics is essential for effective, patient-centered care as the need for precision medicine increases due to aging populations and rising rates of chronic illness.

Pharmacogenomics is becoming quicker, less expensive, and more widely available thanks to developments in genetic testing technology. Multiple genes can now be analyzed simultaneously by next-generation sequencing (NGS), which offers thorough insights into drug metabolism and risks.

Clinics can perform genetic analyses on-site, cutting down on wait times, with the use of portable devices and point-of-care testing kits. For instance, rural hospitals can obtain testing without depending on distant labs thanks to handheld sequencers. In the meantime, AI-powered data tools evaluate medical and genetic records to forecast medication reactions, assisting physicians in making prompt, evidence-based decisions.

Test accuracy has increased thanks to these advancements, which is important in high-risk fields like oncology where a false positive could postpone life-saving care. Additionally, businesses are creating integrated systems that simplify workflows for healthcare providers by combining lab equipment, software, and reagents.

Adoption has increased in medical facilities, research facilities, and even pharmacies, where pharmacists provide advice on medication safety based on genetic data. Additionally, testing is now possible for routine care due to declining DNA sequencing costs, which are currently less than $1,000 per genome.

Pharmacogenomics will become commonplace as technology advances, guaranteeing that treatments are both efficient and cost-effective. These developments not only accelerate market expansion but also give patients and healthcare professionals the ability to make well-informed, individualized decisions.

Pharmacogenomic testing has many advantages, but one of the biggest challenges is still its high cost. Complex data analysis tools, specialized chemicals, and advanced genetic testing equipment come with a hefty upfront cost that frequently exceeds smaller labs’ and hospitals’ budgets.

Many medical facilities find it difficult to pay for these costs, especially those in rural or underdeveloped areas, which restricts their capacity to provide testing. Inconsistencies in insurance coverage exacerbate the problem even more.

For instance, some U.S. insurers deny claims due to a lack of long-term cost-effectiveness data, while others cover certain tests for diseases like depression or cancer. Long-term delays in test adoption occur because insurers in developing countries usually require comprehensive pharmacoeconomic studies before granting coverage.

Because patients in nations like India cannot afford to pay out-of-pocket without insurance support, clinics there frequently refrain from providing pharmacogenomic services entirely. Millions of people lack access to specialized treatments because providers are deterred from incorporating testing into standard care by this financial uncertainty.

Further impeding market expansion are labs in underprivileged areas that struggle to pay for equipment maintenance or employee training. Pharmacogenomics runs the risk of becoming exclusively available to wealthy patients or geographic areas in the absence of subsidies or uniform reimbursement guidelines, thereby exacerbating healthcare inequalities worldwide.

For example, a study conducted in Sub-Saharan Africa discovered that because of financial constraints, less than 5% of clinics offer genetic testing. These disparities show how urgently governments, insurers, and manufacturers must work together to reduce costs and increase coverage in order to guarantee that everyone has fair access to the developments in precision medicine.

Navigating unclear regulations and interpreting genetic data present additional challenges. Large volumes of genetic data are produced by modern tests, which must be analyzed by qualified specialists using sophisticated software.

Smaller labs frequently lack the equipment and skilled personnel necessary to handle this complexity, which can cause mistakes or delays. For example, using antiquated equipment, a rural clinic may miscalculate a patient’s genetic risk for adverse drug reactions.

Additionally, there are no universal standards for interpreting test results, which leads to inconsistent prescription practices among physicians. Regional differences in regulatory requirements for test approval and validation are significant. Global access may be slowed if a test that has been approved in Europe is subjected to years of review in Asia.

Another layer of complexity is added by privacy concerns. Patients and physicians are concerned about the storage and sharing of genetic data, particularly in areas with lax data protection regulations. For instance, a Brazilian hospital may postpone testing due to concerns about data breaches.

Innovation is stifled by the uncertainty these ethical conundrums and regulatory gaps cause for businesses investing in new tests. Pharmacogenomics will take longer to become a standard component of healthcare until governments create more standardized and transparent regulations.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Polymerase Chain Reaction (PCR) DNA Sequencing Microarray Electrophoresis Mass Spectrometry Others |

| By Application |

Drug Discovery Tailored Treatment Oncology Pain Management Others |

| By End User |

Hospitals Research Institutes Pharmaceutical Companies Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Pharmacogenomics examines how genetic factors affect drug response using a variety of technologies. A fundamental technique is the Polymerase Chain Reaction (PCR), which amplifies particular DNA segments to find variations such as SNPs connected to drug metabolism. It is a mainstay in clinical labs due to its speed, accuracy, and affordability.

Precision medicine techniques are made possible by DNA sequencing, especially Next-Generation Sequencing (NGS), which provides deeper insights by analyzing entire genomes to find both common and uncommon genetic variations.

By simultaneously analyzing thousands of genetic markers, microarray technology enhances these techniques and facilitates the identification of biomarkers and extensive research. Even though it is less sophisticated, electrophoresis is still useful for confirming PCR results by separating DNA fragments and evaluating polymorphisms.

By determining molecular masses, mass spectrometry provides an additional layer of analysis for proteins and metabolites, exposing interactions within drug pathways. Innovation in genetic testing is being driven by emerging technologies like digital PCR and nanopore sequencing, which further improve sensitivity and speed.

Pharmacogenomics has a wide range of uses in the medical field. It speeds up the creation of safer, more focused treatments in drug discovery by identifying genetic targets and response variability. In order to improve efficacy and minimize side effects, tailored treatment uses genetic data to personalize drug selections and dosages.

Pharmacogenomics plays a key role in oncology by identifying tumor mutations and drug resistance indicators, which improves the precision of cancer treatment. Genetic insights into drug metabolism and pain perception help manage pain by improving the choice of analgesics.

Additionally, genetic testing is used in infectious diseases, cardiology, and psychiatry to improve drug selection and dosage. These uses demonstrate how pharmacogenomics is changing treatment paradigms in a variety of specialties.

The adoption of pharmacogenomics is driven by key end users. In order to improve patient outcomes, decrease adverse reactions, and customize treatments, hospitals incorporate genetic testing into clinical workflows.

Through studies and trials, research institutes take the lead in investigating genetic-drug interactions and advancing precision medicine. Pharmacogenomic data is used by pharmaceutical companies to stratify patient populations, optimize clinical trials, and create more successful targeted therapies.

Contract research organizations (CROs) and diagnostic labs provide testing services and R&D knowledge to support the ecosystem. Collectively, these users highlight how pharmacogenomics is increasingly being used in healthcare to connect genetic research with practical clinical and business applications.

With a 36.2% market share in 2024, North America is in the lead thanks to strong R&D expenditures, high healthcare spending, and advantageous reimbursement practices. Because of its strong pharmaceutical partnerships, advanced clinical adoption, and initiatives like the FDA’s push for biomarker integration in drug development, the United States leads the world.

Supported by centralized healthcare systems and growing pharmacogenomic use in cardiology and oncology, Europe holds 28%. Adoption is accelerated, especially in Germany, France, and the UK, by EU regulatory frameworks and cross-border partnerships like the EMA’s biomarker guidelines.

Asia Pacific’s 19% share is growing quickly as a result of government initiatives (like China’s precision medicine programs), the expansion of clinical trials in India, and the rise in the prevalence of chronic diseases. Australia and Japan also make contributions through their investments in cutting-edge healthcare infrastructure and research.

LAMEA (16.8%) grows at a moderate rate (~10% CAGR). Through academic collaborations and private labs, South Africa, Brazil, Mexico, and the United Arab Emirates propel advancement. Funding shortages, unequal infrastructure, and regulatory barriers are obstacles, but international partnerships and Middle Eastern medical tourism promote steady market growth.

The market was valued at USD 7.1 billion in 2024.

The market is projected to grow at a CAGR of 9.2 % from 2025 to 2033.

Oncology hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Thermo Fisher Scientific, Illumina, Inc., Qiagen N.V., F. Hoffmann La Roche AG, Abbott Laboratories and Agilent Technologies, Inc

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Pharmacogenomics Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Pharmacogenomics Market, By Application

5.3 Pharmacogenomics Market, By End User

6.1 North America Pharmacogenomics Market, By Country

6.1.1 Pharmacogenomics Market, By Technology

6.1.2 Pharmacogenomics Market, By Application

6.1.3 Pharmacogenomics Market, By End User

6.2 U.S.

6.2.1 Pharmacogenomics Market, By Technology

6.2.2 Pharmacogenomics Market, By Application

6.2.3 Pharmacogenomics Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping