Plasma Fractionation Market

Plasma Fractionation Market size, share, & trends analysis report by product type (Immunoglobulins, coagulation factor concentrates, Albumin, protease inhibitors, Other plasma- derived products) by Application(Immunology, Haematology, Neurology, Critical Care and Trauma, Infection Diseases, Pulmonology and Genetic Disorders) by End User (Hospital and Clinics, Clinical Research Organization, Academic and Research Institutes, Biopharmaceutical Companies ) Industry analysis report, regional outlook growth potential, price trends, competitive market share & forecast 2025-2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIPHR1009

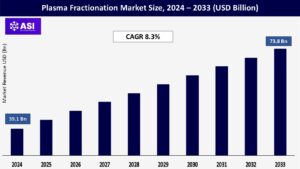

CAGR: 8.3%

Last Updated : July 17, 2025

The global Plasma Fractionation Market was valued at around USD 39.1 billion in 2024 and is anticipated to reach USD 73.8 billion by 2033 with a CAGR of 8.3% over the forecast period (2025–2033).

A critical biotechnological process employed to fractionate plasma into its constituent constituents—e.g., albumin, coagulation factors, and immunoglobulins—used therapeutically in diverse rare and chronic conditions is plasma fractionation. Plasma-derived products are crucial in the management of alpha-1 antitrypsin deficiency, hemophilia, and immunological deficiencies. These biologics are infused into patients requiring long-term replacement therapy, and fractionation makes them very safe and of high purity. Long-term treatment and diagnosis are facilitated by plasma fractionation, primarily for complicated hematological and immunological diseases. Fractionation generates life-saving proteins with unmatched therapeutic effectiveness through highly regulated biochemical steps, mainly for those patients suffering from impaired immune response or genetic disorders.

The key driver of growth in the plasma fractionation market is the rising number of instances of hemophilia, immunodeficiency disorders, and other rare blood diseases worldwide. According to the World Health Organization (WHO), millions of individuals around the world have primary immunodeficiency disorders (PIDs), most of which require immunoglobulin therapy produced from plasma fractionation for the remainder of their lives. For example, an estimated 400,000 individuals around the world are afflicted with hemophilia, and demand will rise further as access and diagnosis become better in developing countries.

The market for immunoglobulins in neurological and autoimmune conditions like Guillain-Barré syndrome and chronic inflammatory demyelinating polyneuropathy (CIDP) is growing, which will increase the pool of patients. The application of plasma-derived therapies is increasing due to enhanced diagnostic centers and increased knowledge, resulting in rise in treatment and diagnosis. In addition, novel indications for plasma proteins and the inclusion of these treatments in national health plans are widening market demand. Growing disease burden, along with increasing healthcare infrastructure, particularly in Asia-Pacific and Latin America, is majorly driving the plasma fractionation market ahead.

Technological advancements in plasma fractionation and growth in the number of plasma collection centers are essential drivers of growth in the market. Improvements in purification techniques—e.g., chromatography and nanofiltration—have improved the yield and safety of plasma-derived products, minimizing the risk of viral transmission and enhancing therapeutic effectiveness.

Examples include firms like Grifols and CSL Behring, which have invested in AI-driven automation and next-generation fractionation plants in recent years, maximizing manufacturing efficiency. At the same time, the expanding plasma donation network, especially in the U.S., Europe, and developing markets such as Brazil and India, guarantees the availability of raw plasma essential to fulfill increasing needs. The Plasma Protein Therapeutics Association (PPTA) records a year-round rise in plasma collections to cater to global demands. Governments are also encouraging plasma self-sufficiency through supportive policies and financing infrastructure, lessening dependence on imports. These advances combined reinforce the plasma supply chain, accommodating the increasing demand for plasma-derived therapies globally.

The market for plasma fractionation is strongly constrained by strict regulatory needs and an inelastic supply of human plasma. Regulatory bodies like the U.S. FDA and the European Medicines Agency apply strict rules on plasma collection, manufacturing, and product safety to avoid contamination and provide safety to patients.

They include elaborate, expensive, and time-consuming processes of approvals, which cause product delays and higher operating costs. Further, the process of fractionation of plasma is very specialized with the use of sophisticated facilities and the need for strict compliance with Good Manufacturing Practices (GMP), which discourages new entrants and innovation in the marketplace.

A further fundamental challenge is the reliance on human plasma donations, which are restricted and frequently not enough to keep pace with increasing worldwide demand. Plasma gathering is capital-intensive, involving well-organized donor facilities and strict screening, limiting plasma supply. Ethical issues and prohibitions on donor payment in most nations affect plasma availability further.

The COVID-19 pandemic brought this vulnerability into focus, interrupting donation campaigns and fueling shortages of supply. These supply limitations, combined with growing demand for plasma-derived medicines, form a major bottleneck that confines the plasma fractionation market’s overall growth.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Immunoglobulins coagulation factor concentrates Albumin protease inhibitors |

| By Application |

Immunology Haematology Neurology Critical Care and Trauma Infection Diseases Pulmonology and Genetic Disorders |

| By End User |

Hospital and Clinics Clinical Research Organization Academic and Research Institutes Biopharmaceutical Companies |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Immunoglobulins take the largest position in the plasma fractionation market with an estimated share of 43.2% in 2024 due to the growing incidence of immunodeficiency diseases, autoimmune disorders, and neurological diseases like chronic inflammatory demyelinating polyneuropathy (CIDP).

The increasing application of intravenous (IVIG) and subcutaneous (SCIG) immunoglobulin treatments, particularly in the U.S. and Europe, is the major growth driver. Coagulation Factor Concentrates such as Factor VIII and Factor IX are critical for controlling bleeding conditions like hemophilia A and B. This market is growing consistently because of increasing diagnostic rates as well as improved access to recombinant drugs.

Albumin is experiencing growing demand in critical care, liver cirrhosis, and treatment of hypoalbuminemia. High acceptance in China and emerging markets plays an important part in market growth. Protease Inhibitors and Other Plasma-Derived Products (such as α1-antitrypsin) constitute a lesser but vital part of the marketplace. They are essential for the management of uncommon genetic and pulmonary diseases and are projected to experience expanding adoption with increased understanding and diagnostic advancements.

Immunology is the leading application segment on account of widespread use of immunoglobulins in the treatment of primary and secondary immunodeficiencies. As awareness increases and access to diagnosis improves, this segment is likely to retain robust growth. Hematology derives support from steady demand for coagulation factors to treat hemophilia and von Willebrand disease.

Development of recombinant and plasma-derived therapies continues to underpin this segment. Neurology is a rapidly growing segment due to the application of IVIG in the treatment of neurological autoimmune conditions such as Guillain-Barré syndrome and CIDP. Increased prevalence and enhanced treatment protocols are fueling the growth of the segment. Plasma-derived albumin and coagulation factor products depend on Critical Care and Trauma in ICUs, particularly for trauma management and volume replacement.

Hospital and trauma center demand is poised to increase steadily. Infectious Diseases, Pulmonology, and Genetic Disorders are new fields where plasma-derived therapies are being utilized more and more, such as in diseases such as α1-antitrypsin deficiency, COVID-19 complications, and rare hereditary diseases.

Hospitals and Clinics are the market leaders, accounting for 62.5% in 2024, following their access to sophisticated plasma therapies for immunodeficiency, bleeding disorders, and critical care. They are primary centers of administration for plasma-derived therapies.

Clinical Research Organizations (CROs) are finding favor as they hold a central position in developing and testing new plasma products. The increase in clinical trials in haematology and immunology favours this segment. Academic and Research Institutions add to innovation and fundamental research in plasma fractionation technologies and disease pathways. With growing public and private funding, their influence on long-term market development will rise.

Biopharmaceutical Companies are the main players in manufacturing, R&D, and commercialization of plasma-derived therapies. Continued investment in plasma collection facilities, product development, and entry into emerging markets is consolidating this segment’s market share.

North America dominates the plasma fractionation market with 41.2% in 2024, due to high penetrations of sophisticated healthcare infrastructure, high levels of awareness regarding plasma-derived therapies, and the dominant presence of key players such as Grifols, CSL Behring, and Takeda.

The United States dominates both plasma collection and consumption with the collection of more than 40 million liters of plasma per annum, facilitating bulk fractionation and export. Growing incidence of immunodeficiency diseases, hemophilia, and neurological disorders, coupled with high healthcare expenditures and reimbursement, maintains market leadership in the region.

Europe is a major market with Germany, Austria, France, and the UK being influential countries in plasma collection and fractionation. The region enjoys a strong regulatory environment and favorable national plasma programs. In 2023 alone, Germany gathered over 7 million liters of plasma, utilized primarily for local production.

Expansion is bolstered by increasing prevalence of rare conditions and stringent government drives encouraging self-reliance in plasma-derived medicines. Additionally, the area’s growing demographic of elderly citizens and rising demand for immunoglobulin and coagulation treatments are driving steady demand.

Asia-Pacific is the region with the highest growth rate in the plasma fractionation market and is estimated to grow at 8.3% during the period 2025–2033. Nations such as China, India, Japan, and South Korea are experiencing high growth through enhanced healthcare expenditure, rising diagnostic rates, and encouragement by governments for plasma donation and fractionation facilities.

China, for example, is developing domestic plasma collection capacity with public-private partnerships to lower dependence on imports. Japan’s sophisticated medical system and increasing elderly population also propel demand for albumin and immunoglobulin treatments. Regulatory issues and constricted donor bases continue to be major obstacles in certain Southeast Asian countries, nonetheless.

Latin America and MEA represent developing markets with moderate growth in plasma fractionation, which is stimulated by healthcare investment increases, growing incidence of infectious and chronic diseases, and expanded use of plasma therapies. Brazil and Mexico dominate the Latin American market, while South Africa, Saudi Arabia, and the UAE are the primary drivers in the MEA region.

Despite increased demand, underdeveloped plasma collection infrastructure, low reimbursement systems, and economic imbalances hinder full market potential. Strategic partnerships and global donor programs can offset such gaps during the forecast period.

The market was valued at USD 39.1 billion in 2024.

The market is projected to grow at a CAGR of 8.3 % from 2025 to 2033.

Immunolglobulins segment hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include CSL Behring, Grifols S.A., Takeda Pharmaceutical Company Limited, Octapharma AG, Kedrion S.p.A.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Plasma Fractionation Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Plasma Fractionation Market, By Application

5.3 Plasma Fractionation Market, By End User

6.1 North America Plasma Fractionation Market, By Country

6.1.1 Plasma Fractionation Market, By Product Type

6.1.2 Plasma Fractionation Market, By Application

6.1.3 Plasma Fractionation Market, By End-User

6.2 U.S.

6.2.1 Plasma Fractionation Market, By Product Type

6.2.2 Plasma Fractionation Market, By Application

6.2.3 Plasma Fractionation Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping