Polycarbonate Market

Polypropylene Market & Trends Analysis Report, By Type (Virgin Polycarbonate, Recycled Polycarbonate), By Grade (General Purpose Grade 1, Retardant to Flames, Grade of Optical), By Application (Automotive, Electronics and Electrical, Building, Health Care Equipment, Packaging & Consumer Products)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

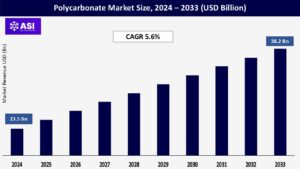

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 5.6%

Last Updated : February 6, 2026

The global Polycarbonate Market size was valued at approximately USD 23.5 billion in 2024, and is projected to reach USD 38.2 billion by 2033, growing at a CAGR of 5.6% during the forecast period (2025–2033).

Polycarbonate is a high-performance thermoplastic known for its outstanding impact resistance, optical clarity, and flame-retardant properties. These attributes make it a versatile material widely utilized across industries such as automotive, electronics, medical devices, and construction.

The need for fuel efficiency and lower emissions is driving the automotive industry’s transition to lightweight and durable materials, which is greatly increasing demand for polycarbonate.

Polycarbonate is perfect for components like connectors, switches, housings, and display panels in the electronics industry because of its exceptional electrical insulation qualities, dimensional stability, and thermal resistance.

Polycarbonate sheets and panels are being used more and more in the building industry for soundproofing barriers, skylights, roofing, and facades.

Long-term performance benefits are provided by its optical clarity, durability, and UV resistance. In areas that are rapidly urbanizing, such as the Middle East and Asia-Pacific, where infrastructure development is accelerating, this trend is especially pronounced.

Bisphenol A (BPA), which has come under fire for possible health and environmental hazards, is commonly used in the production of polycarbonate. Manufacturers are under pressure to provide safer, biobased substitutes due to regulatory limitations and partial bans on BPA-based products, especially in areas like the European Union and North America. Market growth may be impeded by this regulatory environment unless innovation keeps up with the demands of sustainability.

Because petrochemical feedstocks are the source of essential raw chemicals like BPA and phosgene, their costs are susceptible to changes in crude oil prices and interruptions in the worldwide supply chain. For smaller or regional firms with less pricing power, volatility in these material costs can increase manufacturing costs and reduce profit margins.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Virgin Polycarbonate Recycled Polycarbonate |

| By Grade |

General Purpose Grade 1 Retardant to Flames Grade of Optical |

| By Application |

Automotive Electronics and Electrical Building Health Care Equipment Packaging & Consumer Products |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Polycarbonate Market is segmented by Type (Virgin Polycarbonate, Recycled Polycarbonate), By Grade (General Purpose Grade 1, Retardant to Flames, Grade of Optical), By Application (Automotive, Electronics and Electrical, Building, Health Care Equipment, Packaging & Consumer Products).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

The biggest segment is virgin polycarbonate.

Virgin-grade polycarbonate is the material of choice for high-performance industrial, automotive, and medical applications because of its exceptional mechanical strength, optical clarity, and chemical resistance.

Recycled Polycarbonate: The Sector with the Fastest Growth

Recycled polycarbonate is quickly becoming more popular in non-essential applications, including consumer electronics, home goods, and office equipment, thanks to circular economy initiatives and sustainability concerns. This trend is being further accelerated by enhanced recycling technologies and regulatory backing.

By General Purpose Grade 1

This grade’s cost-effectiveness and performance balance make it widely utilized in consumer items, packaging, and electronic enclosures.

Retardant to Flames

This grade, which is intended to satisfy fire safety requirements such as UL 94, is crucial for electrical components, lighting systems, and automobile interiors, where safety compliance is crucial.

Grade of Optical

Optical-grade polycarbonate, which is used in eyeglass lenses, medical devices, LED lighting, and optical media, is distinguished by its remarkable clarity and resilience to impact.

The Leading Segment: Automotive

Polycarbonate is utilized in dashboards, interior trim pieces, headlamp lenses, and glazing panels where impact resistance, light weighting, and design flexibility are essential.

Electronics and Electrical

Battery housings, switches, circuit breakers, and lighting systems are among the applications that make use of polycarbonate’s insulating qualities, flame resistance, and dimensional stability.

Building

Because of its UV resistance, durability, and light transmission, polycarbonate is frequently utilized in residential, commercial, and industrial construction projects for roofing sheets, glazing panels, and acoustic barriers.

Health Care Equipment

Polycarbonate is appropriate for use in medical housings, fluid delivery systems, and surgical instruments due to its impact strength, biocompatibility, and sterilizability.

Packaging & Consumer Products

Polycarbonate, which is frequently found in reusable bottles, kitchenware, DVDs, and transparent packaging, offers mass consumer goods durability, clarity, and design versatility.

In 2024, Asia-Pacific had more than 47% of the world market for polycarbonate. China, India, South Korea, and Japan are at the forefront, driven by their robust automotive, electronics, and construction sectors. The region’s supremacy is further cemented by the existence of sizable manufacturing centers, reduced production costs, and robust export capacities.

The United States leads North America with over 21 percent of the worldwide market, thanks to its strong R&D expenditure, technical innovation, and sophisticated manufacturing infrastructure. High-end industries like consumer electronics, medical gadgets, and aircraft are heavily represented in the region.

Demand is primarily driven by Germany, France, and the Netherlands, and Europe accounts for about 19% of the global market. With the increasing use of recycled and bio-based polycarbonate materials under stringent environmental restrictions, the region is leading the way in sustainability projects.

The market in Latin America is steadily growing thanks to the expansion of auto manufacturing in nations like Brazil and Mexico. Regional growth is significantly influenced by growing urbanization, consumer electronics, and the need for long-lasting building materials.

The construction and packaging industries are seeing an increase in demand in this developing region. The adoption of polycarbonate products is being fueled by government infrastructure investments and advancements in healthcare standards, especially in South Africa, the United Arab Emirates, and Saudi Arabia.

The current size of the polycarbonate market IS USD 23.5 billion in 2024.

The projected CAGR from 2025 to 2033 is 5.6%.

The Asia-Pacific (47% share in 2024) holds the largest market share.

The key end-use industries are Automotive, electronics, construction, healthcare, and consumer goods.

The polycarbonate market players are Covestro, SABIC, LG Chem, Mitsubishi Engineering-Plastics, and Teijin.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Polycarbonate Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Polycarbonate Market, By Grade

5.3 Polycarbonate Market, By Application

6.1 North America Polycarbonate Market , By Country

6.1.1 Polycarbonate Market, By Type

6.1.2 Polycarbonate Market, By Grade

6.1.3 Polycarbonate Market, By Application

6.2 U.S.

6.2.1 Polycarbonate Market, By Type

6.2.2 Polycarbonate Market, By Grade

6.2.3 Polycarbonate Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping