Polyethylene Market

Polyethylene Market & Trends Analysis Report, By Product Type (HDPE, LDPE, LLDPE), By Application (Packaging, Construction, Automotive, Electrical & Electronics, Others), By End-Use Industry (OEMs, Aftermarket, Manufacturers)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

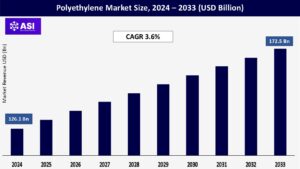

CAGR: 3.6%

Last Updated : February 6, 2026

The global polyethylene (PE) Market size was valued at approximately USD 126.1 billion in 2024, and is projected to reach USD 172.5 billion by 2033, growing at a CAGR of 3.6% during the forecast period (2025–2033).

Polyethylene, a versatile thermoplastic polymer, is widely used across industries due to its chemical resistance, flexibility, durability, and ease of processing. PE is classified into HDPE (High-Density), LDPE (Low-Density), and LLDPE (Linear Low-Density), each with unique properties that support a wide range of applications, including packaging, consumer products, and piping.

Growth is driven by rising demand for sustainable and lightweight materials in packaging and construction. However, environmental concerns and recycling challenges pose constraints.

Polyethylene is the cornerstone of the global flexible packaging industry. Its lightweight, non-toxic, durable, and moisture-resistant characteristics make it ideal for manufacturing films, bags, containers, and wraps.

The rapid expansion of e-commerce, increasing demand for convenience packaging, and rising urban consumption—especially in developing nations—are propelling the need for cost-effective and resilient packaging materials, significantly boosting PE consumption.

High-Density Polyethylene (HDPE) is widely used in construction-related applications such as water and gas piping systems, cable insulation, protective barriers, and geomembranes.

Its high chemical resistance, long service life, and flexibility under varying environmental conditions make it a preferred material in infrastructure projects. Accelerated urbanization and increased government spending on infrastructure development in regions like Asia-Pacific and the Middle East are major contributors to the rising demand for polyethylene in this sector.

Technically, polyethylene can be recycled, but in practice, recycling rates are still low because of issues like inadequate waste segregation, contamination, and a lack of infrastructure, especially in developing nations.

Stricter laws, like the EU’s prohibitions on single-use plastics, and heightened public scrutiny are the results of growing environmental concerns about plastic pollution. This may affect the market for PE in the long run by driving producers and consumers toward substitute materials like bioplastics and compostable polymers.

Ethylene, a petrochemical feedstock obtained from natural gas and crude oil, is the precursor to polyethylene. Production costs and profit margins are therefore directly impacted by changes in the price of crude oil, geopolitical crises, and supply chain interruptions. Because of this volatility, PE manufacturers’ pricing and sourcing methods are more complicated.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

HDPE (High-Density Polyethylene) LDPE (Low-Density Polyethylene) LLDPE (Linear Low-Density Polyethylene) |

| By Application |

Packaging Construction Automotive Electrical & Electronics Others |

| By End-Use Industry |

OEMs Aftermarket Manufacturers |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Polyethylene Market is segmented by Product Type (HDPE, LDPE, LLDPE), By Application (Packaging, Construction, Automotive, Electrical & Electronics, Others), By End-Use Industry (OEMs, Aftermarket, Manufacturers).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

HDPE is characterized by its high strength-to-density ratio, rigidity, and excellent chemical resistance. It is extensively used in blow molding applications such as bottles, drums, fuel tanks, as well as in pressure piping systems, geomembranes, and industrial containers. Its durability and performance in demanding environments make it the largest product segment.

LDPE is valued for its flexibility, clarity, and ease of processing. It is primarily used in film applications, including plastic bags, shrink wraps, and agricultural coverings. Its low melting point and softness make it ideal for lightweight, single-use products and protective packaging.

LLDPE offers a balance of strength, puncture resistance, and flexibility. It is widely used in stretch and shrink films, industrial liners, flexible tubing, and packaging applications where toughness and elongation are critical. Its ability to be blended with other grades enhances its versatility.

Packaging is the dominant application for polyethylene, especially in the form of films used for food packaging, carry bags, stretch and shrink wraps, and personal care product packaging. The growing consumption of packaged foods, healthcare supplies, and the continued boom in e-commerce and retail are major drivers for PE demand in this segment.

In the construction sector, PE is utilized for water and gas pipelines, vapor barriers, insulation layers, and geomembranes. Its resistance to moisture, chemicals, and UV radiation, along with long service life, makes it ideal for both residential and industrial infrastructure applications.

Polyethylene is increasingly used in automotive components such as fuel tanks, bumpers, fender liners, under-hood parts, and cable insulation. As the automotive industry shifts toward lightweight and energy-efficient vehicles—particularly electric vehicles (EVs)—PE’s role continues to grow.

PE’s excellent dielectric strength and thermal resistance make it suitable for wire and cable insulation, connector housings, semiconductors, and appliance components. Growth in electrification and consumer electronics fuels demand in this segment.

This category includes applications in agriculture (e.g., mulch films, greenhouse coverings), household goods (storage containers, toys), and medical products (disposable tubing, specimen containers). The versatility and safety of PE enable its use across diverse, niche sectors.

The main end-use market is made up of OEMs, who employ polyethylene in a variety of sectors such as electronics, construction, automotive, and packaging. The requirement for scalable, reliable, and high-quality material solutions that can be incorporated into large production lines for final products is what drives their demand.

The need for polyethylene in maintenance, repair, and refill applications is included in the aftermarket segment. Reusable packaging in consumer goods, agricultural sheet replenishments, and the repair of construction components are important topics. PE is a desirable material in this market because of its cost-effectiveness and flexibility.

Polyethylene is used by small and medium-sized businesses to make consumer goods, tools, industrial containers, and custom-molded items. PE is appropriate for specialized and low-to-medium volume production due to its adaptability, simplicity in molding, and compatibility with a wide range of design specifications.

Asia-Pacific is the largest and fastest-growing region in the global polyethylene market. China and India are at the forefront in both consumption and production, driven by rapid industrialization, urban population growth, and rising demand for packaged goods, construction materials, and automotive components. Expanding manufacturing capacity and government support for infrastructure development further strengthen the region’s position.

The North American market shows stable growth, supported by demand in industrial applications, packaging, and construction. The U.S. leads in the production and export of PE resins, with significant investments in both mechanical and chemical recycling technologies. Innovations in sustainable plastic processing are contributing to long-term market sustainability.

Europe is witnessing moderate growth due to stringent environmental and sustainability regulations. The push for circular economy practices is accelerating the adoption of recycled and bio-based polyethylene, especially in consumer goods and packaging. Regulatory pressures are also encouraging material innovation and alternative feedstock development.

Latin America is seeing steady growth, led by expanding urbanization and a rising middle-class population. Countries like Brazil and Mexico are driving PE demand through increased consumption of packaged products and investments in residential and commercial construction. The region also benefits from growing agricultural film and flexible packaging markets.

This region offers emerging opportunities fueled by rapid infrastructure development, industrialization, and population growth. Investments in petrochemical complexes and domestic plastic manufacturing—especially in Gulf Cooperation Council (GCC) countries—are boosting local PE production and consumption. The rising demand for packaged food and clean water solutions also supports market expansion.

The market value of polyethylene in 2024 is USD 126.1 billion.

The global polyethylene market is projected to grow at a CAGR of 3.6%.

The Packaging application segment dominates the polyethylene market.

The Asia-Pacific region is expected to witness the fastest growth.

The major players in the polyethylene market are ExxonMobil, SABIC, LyondellBasell, Dow, INEOS.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Polyethylene Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Polyethylene Market, By Application

5.3 Polyethylene Market, By End-Use Industry

6.1 North America Polyethylene Market , By Country

6.1.1 Polyethylene Market, By Product Type

6.1.2 Polyethylene Market, By Application

6.1.3 Polyethylene Market, By End-Use Industry

6.2 U.S.

6.2.1 Polyethylene Market, By Product Type

6.2.2 Polyethylene Market, By Application

6.2.3 Polyethylene Market, By End-Use Industry

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping