Polyethylene Terephthalate Market

Polyethylene Terephthalate Market & Trends Analysis Report, By Product Type (Opaque ABS, Transparent ABS, Virgin PET, PET Recycled), By Application (Bottles, Films & Sheets, Food Packaging, Others), By End-Use Industry (Beverage, Food, Pharmaceuticals, Personal Care & Cosmetics, Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

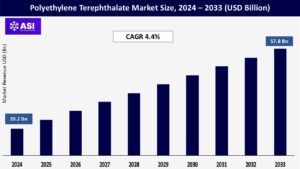

CAGR: 4.4%

Last Updated : February 6, 2026

The global polyethylene terephthalate (PET) market size was valued at approximately USD 39.2 billion in 2024, and is projected to reach USD 57.8 billion by 2033, growing at a CAGR of 4.4% during the forecast period (2025–2033).

PET is a highly recyclable and durable thermoplastic widely used in packaging, textiles, and consumer goods. Its key properties, clarity, strength, chemical resistance, and lightweight nature make it ideal for beverage bottles, food packaging, and industrial applications. The increasing emphasis on sustainability, demand for recyclable materials, and growing beverage consumption are primary growth drivers for the PET market.

The greatest end-use market for PET is the beverage sector, which uses it extensively to package fruit juices, carbonated soft drinks, energy drinks, and bottled water. PET is the perfect material for single-use and portable packaging because of its low weight, superior clarity, resistance to shattering, and affordability.

Globally, bottled beverage consumption has increased due to factors such as urban population growth, rising disposable incomes, and growing health consciousness, which has greatly increased PET demand.

The industry is strongly moving toward sustainable alternatives like recycled PET (rPET) in response to growing environmental concerns and changing government rules about plastic waste. By using more recycled materials in their packaging, companies in the food, beverage, and personal care industries are supporting global sustainability goals.

PET continues to present environmental problems despite its great recyclability, since many areas lack proper waste management and recycling facilities. When plastic is improperly disposed of, it pollutes landfills, rivers, and seas, attracting regulatory attention and putting more pressure on companies. This affects PET’s reputation and encourages manufacturers and customers to look for other packaging options.

The manufacture of PET is mostly dependent on petrochemical derivatives made from crude oil, such as Purified Terephthalic Acid (PTA) and Monoethylene Glycol (MEG).

The economics of PET production and price competitiveness are directly impacted by abrupt changes in crude oil prices, which lead to fluctuating raw material costs. Because of this instability, producers face difficulties with pricing strategies

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Opaque ABS Transparent ABS Virgin PET PET Recycled |

| By Application |

Bottles Films & Sheets Food Packaging Others |

| By End-Use Industry |

Beverage Food Pharmaceuticals Personal Care & Cosmetics Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Polyethylene Terephthalate Market is segmented by Product Type (Opaque ABS, Transparent ABS, Virgin PET, PET Recycled), By Application (Bottles, Films & Sheets, Food Packaging, Others), By End-Use Industry (Beverage, Food, Pharmaceuticals, Personal Care & Cosmetics, Others).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Due to its extensive use in consumer items, construction materials, and automotive components, opaque ABS leads the market. It is preferred because of its superior mechanical strength, robustness, and processing simplicity, which make it appropriate for injection molding and other production techniques. Its widespread use is further facilitated by its affordability and adaptability.

The market share of transparent ABS is lower but still substantial. It is mostly utilized in products like cosmetic packaging, display screens, and some medical equipment that need to be both durable and optically clear. Despite being more costly than opaque alternatives, its useful qualities and visual attractiveness enable specialized, high-value applications.

Because of its strength, clarity, and extensive use in high-performance packaging and bottle manufacturing, virgin PET is the industry standard. When mechanical and optical performance are crucial, it is recommended.

Because of efforts to promote the circular economy, recycled PET is becoming more popular. Technological developments are increasing their use in high-end and food-grade applications, despite potential performance and color limits.

This is the dominant application segment, with PET extensively used for packaging mineral water, carbonated beverages, juices, and personal care liquids like shampoos and lotions. Its lightweight, impact resistance, clarity, and recyclability make it the preferred material for both single-use and reusable bottles.

PET films and sheets are employed in flexible packaging, thermoformed containers, and electronic applications. Their high tensile strength, dimensional stability, and resistance to heat and moisture make them ideal for packaging food products, electronics, and industrial components.

PET trays, containers, and clamshells are widely used for packaging ready-to-eat meals, fresh produce, and bakery items. Key benefits include excellent oxygen and moisture barrier properties, transparency, and microwave compatibility, making PET a preferred choice for modern food packaging solutions.

This category covers a wide range of applications including PET fibers in textiles, components in automotive and electrical sectors, and niche uses in 3D printing and household goods. Continuous innovation is expanding PET’s footprint across diverse industrial domains.

The beverage industry remains the largest end-use sector for PET, leveraging its lightweight, shatter-resistant, and transparent properties for packaging bottled water, carbonated soft drinks, juices, and energy beverages. The material’s ability to maintain product integrity and extend shelf life underpins its widespread adoption.

PET is extensively used in packaging applications for meats, dairy, bakery products, and ready-to-eat meals. Its excellent visibility, hygiene standards, and resistance to moisture and contaminants make it ideal for maintaining freshness and ensuring food safety throughout the supply chain.

In the healthcare and pharmaceutical sectors, PET is valued for its chemical inertness, clarity, and ability to withstand sterilization processes. It is commonly used in blister packs, medical vials, pill containers, and protective packaging for sensitive drugs and equipment.

PET’s aesthetic appeal, rigidity, and clarity make it a preferred packaging choice for personal care items such as shampoos, conditioners, lotions, and creams. The growing demand for convenient, portable, and visually appealing packaging supports market growth in this segment.

This includes a wide array of applications across textiles (as PET fibers), automotive parts, electronics, and agriculture. The versatility and adaptability of PET are expanding its reach into non-traditional and emerging industrial sectors.

China and India, two of the world’s largest manufacturers and consumers, are at the top of the Asia-Pacific PET market. Key drivers in the region include the rapidly growing packaging industry, growing urbanization, and rising consumption of packaged foods and beverages in bottles. Government programs to increase manufacturing and recycling capabilities also contribute to market expansion.

Great improvements in recycling infrastructure and customer preferences for eco-friendly packaging are driving the steady demand in North America. Recycled PET (rPET) is becoming increasingly popular in the US market as big firms pledge to use packaging that is environmentally friendly.

With a focus on the circular economy, Europe is leading the way in environmental and regulatory activities. The extensive use of rPET is being fueled by EU regulations requiring recycled content in packaging and lowering single-use plastics. Around the region, there is a lot of innovation in environmentally friendly packaging options.

Growth in Latin America is sluggish, especially in nations like Brazil and Mexico. PET packaging is becoming more popular, particularly in the bottled water and soft drink sectors, as a result of rising urbanization, expanding beverage consumption, and growing environmental consciousness.

Due to factors like growing middle-class populations, increasing urbanization, and expanding packaged food and beverage consumption, the Middle East and Africa region presents new growth prospects. The growth of the PET market is also being aided by foreign investments and infrastructure development in the packaging sector, especially in the GCC nations.

The market value of polyethylene terephthalate in 2024 is USD 39.2 billion.

The global polyethylene terephthalate market is projected to grow at a CAGR of 4.4%.

The Bottles application segment dominates the polyethylene terephthalate market.

The Asia-Pacific region is expected to witness the fastest growth.

The major players in the polyethylene terephthalate market are Indorama Ventures, Alpek, Reliance Industries, Sinopec, Far Eastern New Century.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Polyethylene Terephthalate Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Polyethylene Terephthalate Market, By Application

5.3 Polyethylene Terephthalate Market, By End-Use Industry

6.1 North America Polyethylene Terephthalate Market , By Country

6.1.1 Polyethylene Terephthalate Market, By Product Type

6.1.2 Polyethylene Terephthalate Market, By Application

6.1.3 Polyethylene Terephthalate Market, By End-Use Industry

6.2 U.S.

6.2.1 Polyethylene Terephthalate Market, By Product Type

6.2.2 Polyethylene Terephthalate Market, By Application

6.2.3 Polyethylene Terephthalate Market, By End-Use Industry

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping