Pulse Oximeter Market

Pulse Oximeter Market Share & Trends Analysis Report, By Product Type (Fingertip Pulse Oximeters, Handheld Pulse Oximeters, Bedside/Desktop Pulse Oximeters, Wrist-Worn Pulse Oximeters, Wearable Pulse Oximeters), By Sensor Type (Disposable Sensors, Reusable Sensors), By Technology Type (Conventional, Smart/Connected), By End-User (Hospitals & Clinics, Home Care Settings, Ambulatory Surgical Centers, Emergency Medical Services (EMS), Others (e.g., sleep clinics, military healthcare)) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIITR1000

CAGR: 7.0%

Last Updated : March 17, 2026

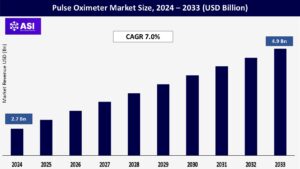

The global pulse oximeter market was valued at approximately USD 2.7 billion in 2024 and is projected to reach USD 4.9 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 7.0% during the forecast period of 2025–2033.

The global pulse oximeter market is growing steadily, fueled by a mix of important healthcare trends. As respiratory illnesses become more common and the global population continues to age, there’s a rising need for reliable, easy-to-use monitoring tools. At the same time, more people are turning to home healthcare, creating strong demand for accessible devices like pulse oximeters. With ongoing improvements in technology, these devices are becoming more accurate, user-friendly, and connected, making them an increasingly vital part of modern healthcare.

One of the most powerful forces driving the pulse oximeter market is the growing number of people affected by chronic respiratory conditions. Diseases like COPD, asthma, pneumonia, sleep apnea, cystic fibrosis, and lung cancer are becoming more widespread across the globe. These conditions often require patients to regularly monitor their blood oxygen levels to manage symptoms and avoid complications. Pulse oximeters have become vital tools in this effort, not just in hospitals, but also for home use, where patients can keep a close eye on their health. As these diseases continue to rise, the demand for pulse oximeters is increasing in parallel.

To put things into perspective, the World Health Organization estimated that over 392 million people were living with COPD in 2023 alone, a clear sign of the scale and urgency of the need for effective monitoring solutions.

The pulse oximeter has come a long way from being a basic hospital tool. Thanks to continuous innovation, today’s devices are more accurate, easier to use, and packed with advanced features that make them indispensable in both clinical and everyday settings. Manufacturers are tackling common challenges like getting accurate readings regardless of skin tone, movement, or poor circulation through smarter algorithms and better sensors. Devices are also becoming smaller and more convenient, with fingertip models, wristbands, and even smart rings that monitor your blood oxygen levels without getting in the way.

Wireless connectivity is another game-changer. Bluetooth and Wi-Fi-enabled oximeters now sync effortlessly with smartphones and cloud platforms, making it easier to track and share health data in real-time. Some even use artificial intelligence to analyze patterns and offer predictive insights, helping users and healthcare providers spot potential problems early.

Newer models are going a step further with multi-wavelength sensors that can detect abnormal forms of hemoglobin, providing a more complete picture of a person’s oxygenation status. All these advancements are making pulse oximeters not just more powerful, but more accessible and appealing to a wide range of users, from doctors to everyday people managing their health at home.

Despite their growing popularity, pulse oximeters still face important limitations, some of which can have serious consequences for patient care. One of the most significant concerns is the issue of accuracy in individuals with darker skin tones. Studies have shown that these devices often overestimate oxygen saturation levels in such patients, a problem known as “occult hypoxemia,” where dangerously low oxygen levels go undetected. This can lead to delayed or incorrect treatment decisions, undermining both patient safety and confidence in the technology. Although recent developments like the FDA’s new guidance in January 2025 and the launch of advanced products such as Nonin’s TruO2 OTC in December 2024 aim to address this issue, it remains a serious concern for clinicians and patients alike.

Other factors can also affect accuracy, including low blood flow due to conditions like shock or hypothermia, patient movement during readings, and interference from dark nail polish or artificial nails. Additionally, standard pulse oximeters struggle to distinguish between normal and abnormal forms of hemoglobin, such as those found in carbon monoxide poisoning or methemoglobinemia, which can lead to misleadingly high readings.

These limitations not only reduce the reliability of pulse oximeters but also contribute to hesitation in their wider adoption, especially in high-risk or underserved populations often requiring the use of more advanced, costly devices to ensure dependable results.

Bringing a new pulse oximeter or any medical device to market is no easy feat. Companies must navigate a complex web of regulatory approvals from authorities like the FDA in the United States, the EMA in Europe, and similar bodies in other regions. These processes are thorough for good reason, but they’re also time-consuming and costly. Manufacturers are required to conduct extensive clinical trials, meet strict quality and safety standards, and go through detailed approval procedures, all of which demand significant investment in research, development, and compliance. For smaller companies, these hurdles can be especially challenging, often resulting in delayed product launches or even halting innovation altogether.

Adding to the difficulty is the fact that regulatory requirements vary widely from country to country, making it harder and more expensive for manufacturers to enter global markets. These regulatory complexities, while essential for patient safety, can act as a major barrier to entry for new players and slow down the availability of newer, more advanced pulse oximeters in many parts of the world.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Fingertip Pulse Oximeters Handheld Pulse Oximeters Bedside/Desktop Pulse Oximeters Wrist-Worn Pulse Oximeters Wearable Pulse Oximeters |

| By Sensor Type |

Disposable Sensors Reusable Sensors |

| By End User |

Hospitals & Clinics Home Care Settings (fastest-growing segment) Ambulatory Surgical Centers Emergency Medical Services (EMS) Others (e.g., sleep clinics, military healthcare) |

| By Technology Type |

Conventional Smart/Connected

|

| Key Players |

Masimo Corporation Medtronic plc Koninklijke Philips N.V. GE HealthCare Nonin Medical Inc. Nihon Kohden Corporation ICU Medical, Inc. Contec Medical Systems Co., Ltd. Drägerwerk AG & Co. KGaA Smiths Medical (now part of ICU Medical) Criticare Systems Spacelabs Healthcare Promed Co. Welch Allyn Co. Omron Corporation Opto Circuits Ltd. Meditech Equipment Co. Ltd. CareFusion Corp. (now part of BD) |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Pulse Oximeter Market is categorized by product type, by sensors, by technology type and by end-user. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. The pulse oximeter market is a dynamic sector driven by the increasing prevalence of respiratory and cardiovascular diseases, a growing geriatric population, and the rising demand for home care and remote patient monitoring solutions.

The market for pulse oximeters is evolving rapidly, with portable devices leading the charge as more people turn to home-based healthcare and take a proactive interest in monitoring their health. Among these, fingertip pulse oximeters have become especially popular, gaining widespread use during the COVID-19 pandemic as a simple yet effective way for individuals to keep track of their oxygen levels. Handheld models, on the other hand, remain a staple in hospitals and clinics thanks to their reliability, portability, and usefulness in fast-paced medical environments. Wearable pulse oximeters, such as those found in smartwatches and fitness bands, are emerging as one of the fastest-growing segments, appealing to tech-savvy consumers who want real-time health data on the go.

Meanwhile, traditional tabletop or bedside pulse oximeters continue to play a crucial role in hospitals, particularly in intensive care units, surgical theaters, and emergency rooms, where continuous and highly accurate monitoring is essential. Together, these different types of devices reflect a growing trend: the integration of pulse oximetry into everyday health routines and critical care alike.

Pulse oximeters rely on sensors, or probes, that emit and detect light to measure oxygen saturation in the blood, and the market for these sensors is broadly divided into disposable and reusable types. Disposable sensors currently dominate the market, accounting for as much as 75% of the total share in some reports. Their widespread use is largely driven by the need for strict hygiene and infection control, especially in hospitals and clinics. Designed for single-patient use, these sensors eliminate the risk of cross-contamination, making them particularly vital in high-risk environments such as operating rooms, intensive care units, emergency departments, and even in home care settings where patients with chronic conditions require frequent monitoring. Their growth is fueled by increased awareness of infection prevention, a rise in surgical procedures, and the expanding role of home-based healthcare.

Reusable sensors, while holding a smaller share, remain significant in the market. They are often favored for their long-term cost efficiency, particularly in settings where one device is used repeatedly by the same patient. These sensors are commonly found in general hospital wards, outpatient clinics, and select home care scenarios where sterilization protocols can be managed effectively.

Alongside these segments, the technology itself is rapidly advancing. Sensors are becoming smaller and more discreet, making them easier to integrate into wearable devices like smartwatches and rings. At the same time, ongoing research is improving their accuracy in challenging conditions such as low blood flow, patient movement, and varying skin tones. Innovations in materials are also making sensors more comfortable, durable, and skin-friendly. Additionally, there is a growing trend toward multi-parameter sensors that can monitor not just oxygen saturation but also other vital signs like temperature and heart rate variability, all in a single, compact device.

Pulse oximeters today are evolving beyond their traditional role, and the market can be broadly divided based on the level of technology and connectivity built into the device. Conventional or stand-alone devices still hold the largest share of the market. These include many familiar models, such as fingertip, handheld, and tabletop pulse oximeters that display real-time oxygen saturation and pulse rate readings but typically don’t connect to other systems. Their popularity comes from being affordable, easy to use, and reliable, making them a go-to choice in hospitals, clinics, and homes, particularly in settings where basic, cost-effective monitoring is essential. On the other hand, smart or connected pulse oximeters represent the fastest-growing segment. These modern devices come equipped with Bluetooth or Wi-Fi connectivity, allowing users to transmit their data to smartphones, tablets, or cloud-based platforms. Many integrate with mobile apps to track health trends, send alerts, and even offer AI-powered insights.

This category includes a wide range of wearables like smartwatches and fitness bands that offer SpO2 monitoring. The rise of remote patient monitoring, telemedicine, and home healthcare has significantly fueled the growth of connected devices. They’re especially useful for individuals managing chronic conditions, recovering from illness, or simply taking a proactive approach to their health. As a result, they’re increasingly being adopted in home care, long-term care facilities, and telehealth platforms.

From a broader perspective, the technology is trending toward greater integration with artificial intelligence for predictive analysis, seamless connectivity with electronic health records and wellness platforms, and user-friendly designs that cater to everyday consumers. At the same time, data privacy and security are becoming more important, prompting stricter scrutiny from regulators, particularly as these devices shift from clinical tools to mainstream consumer products. Together, these trends are reshaping the pulse oximeter landscape, making it smarter, more connected, and increasingly central to modern healthcare.

The pulse oximeter market serves a wide range of end-users, each with distinct needs and usage environments, reflecting the device’s versatility across the healthcare spectrum. Hospitals and clinics remain the largest consumers of pulse oximeters, where accurate and continuous monitoring of oxygen saturation is critical. From intensive care units and emergency departments to neonatal wards and surgical theaters, these devices are an essential part of daily patient management. The high volume of patients, combined with the need for precise, medical-grade monitoring, drives strong demand in these settings.

Hospitals also benefit from integration with broader hospital systems, including electronic health records and multi-parameter monitors, enhancing data flow and clinical efficiency. Meanwhile, home care has emerged as the fastest-growing segment, spurred by the rising burden of chronic conditions like COPD and heart failure, an aging population, and the increasing shift toward remote healthcare. Patients now have access to compact, easy-to-use pulse oximeters especially fingertip and wearable models that allow them to monitor their oxygen levels from the comfort of home. This is not only cost-effective but also empowering, enabling patients to stay proactive in managing their health.

The COVID-19 pandemic further accelerated this trend, normalizing remote monitoring and expanding the use of connected devices that can transmit health data directly to care providers. Ambulatory surgical centers (ASCs) and outpatient facilities also represent a significant portion of the market. With more procedures being done outside of traditional hospitals, these centers rely on portable and reliable pulse oximeters to ensure patient safety during surgeries, sedation, and recovery. Their focus is on equipment that is quick to deploy, easy to transport between procedure rooms, and equipped with alarms and data storage for comprehensive monitoring. Beyond traditional healthcare, pulse oximeters are finding use in a variety of other areas. Emergency medical services depend on them for rapid, on-the-spot assessments in ambulances or at accident scenes.

In sports and fitness, athletes and enthusiasts use them to monitor oxygen levels during intense workouts or high-altitude training, while in aviation, pulse oximeters are used by pilots and passengers in unpressurized aircraft to safeguard against hypoxia. Academic and research institutions also use them in studies focused on respiratory health and physiological monitoring. Across all these segments, the broader trend is clear: the market is steadily moving towards smarter, more accurate, and connected devices. Whether in hospitals or homes, the focus is shifting from reactive treatment to proactive and personalized care, with pulse oximeters playing a key role in this transformation.

The pulse oximeter market varies widely across different regions, shaped by local healthcare systems, population health trends, and levels of technological advancement. North America continues to lead the market, thanks to its well-established healthcare infrastructure, high prevalence of chronic respiratory conditions, and strong adoption of advanced medical technologies.

However, it’s the Asia-Pacific region that’s emerging as the fastest-growing market. With its large and aging population, increasing awareness of health issues, and expanding access to healthcare services, countries in this region are rapidly embracing pulse oximetry, especially in home and community settings. Across the globe, one trend remains consistent: a growing demand for portable, easy-to-use, and connected pulse oximeters. Whether it’s for managing chronic illness, supporting remote care, or simply promoting proactive health tracking, these devices are becoming central to modern, patient-centered care everywhere.

North America stands as the dominant force in the global pulse oximeter market, a position it’s expected to maintain in the years ahead. This leadership is rooted in a combination of strong fundamentals and forward-thinking innovation. The region benefits from a highly developed healthcare system, with a dense network of hospitals, clinics, and surgical centers that rely on pulse oximeters for routine and critical care. Chronic respiratory and cardiovascular diseases—like COPD, asthma, and congenital heart defects—are widespread, further driving the need for reliable oxygen monitoring across all levels of care. An aging population also plays a significant role. As more seniors face health challenges that require consistent monitoring, demand for user-friendly, home-based pulse oximeters continues to grow.

North America’s early embrace of digital health technologies has accelerated this shift, with connected devices and remote monitoring now commonplace in both clinical and home settings. Policies have helped, too. Organizations like the Centers for Medicare & Medicaid Services (CMS) offer favorable reimbursement frameworks that support wider adoption, especially for home healthcare. Additionally, the presence of major global manufacturers in the region ensures that innovation stays at the forefront, from devices that integrate with telehealth platforms to those addressing long-standing issues like accuracy disparities across different skin tones. Altogether, North America’s pulse oximeter market reflects a mature yet dynamic ecosystem, one where advanced technology, proactive healthcare delivery, and policy support combine to keep it at the cutting edge of patient monitoring.

Europe represents a significant portion of the global pulse oximeter market, supported by a robust healthcare foundation and a growing need for chronic disease management. With a high prevalence of respiratory conditions such as COPD across many countries, the demand for reliable oxygen monitoring tools continues to rise. Europe’s aging population further adds to this need, as older adults are more likely to require ongoing health monitoring. The region benefits from well-established, universally accessible healthcare systems, which make it easier for pulse oximeters to be adopted in both clinical and home settings.

European regulatory standards, known for their rigor, help ensure that devices meet high safety and quality benchmarks building strong public and professional trust. In line with broader digital health trends, there’s also growing interest in smart, connected pulse oximeters that integrate with health apps and remote monitoring systems. As a result, Europe is seeing a steady shift toward more portable, user-friendly devices, with an emphasis on early detection, at-home care, and equitable accuracy across diverse patient populations.

The Asia-Pacific region is quickly emerging as the fastest-growing market for pulse oximeters, driven by a powerful mix of demographic, economic, and healthcare trends. With massive and aging populations in countries like China and India, the region is facing a rising tide of chronic and infectious diseases. This has created a pressing need for accessible, reliable health monitoring tools, especially ones that can be used outside traditional hospital settings.

Healthcare infrastructure across the region is undergoing a significant transformation. Governments and private stakeholders are investing heavily in expanding medical services, especially in rural and underserved areas. At the same time, a growing middle class is becoming more health-conscious and tech-savvy, fueling demand for personal health devices like fingertip and wearable pulse oximeters.

The COVID-19 pandemic also catalyzed a lasting shift towards remote care and telemedicine, making pulse oximeters an essential tool for home monitoring. This shift is being supported by national initiatives aimed at improving healthcare access and encouraging the adoption of smart medical technologies. Additionally, countries such as India are ramping up local manufacturing, producing affordable, high-quality devices that meet both domestic and regional demand.

As a result, the Asia-Pacific market is not only expanding rapidly, but it’s evolving. There’s a noticeable trend toward compact, connected, and user-friendly pulse oximeters that suit the needs of both urban professionals and rural families alike. With China and India leading the charge, the region is poised to become a global hub for growth and innovation in oxygen monitoring solutions.

The Middle East and Africa region is steadily gaining traction in the global pulse oximeter market, thanks to a combination of rising healthcare investments and a growing recognition of the importance of vital sign monitoring. Governments across several countries are putting more resources into modernizing healthcare facilities and expanding access to medical technologies. Respiratory conditions remain a pressing concern in the region, fueled by widespread smoking, air pollution, and genetic factors, all of which drive the need for reliable oxygen monitoring solutions.

Awareness is also on the rise, both among healthcare professionals and the general public, about the value of continuous health tracking. Additionally, the growth of medical tourism in countries like the UAE and Saudi Arabia is pushing demand for advanced, hospital-grade equipment. At the same time, there’s a parallel increase in demand for portable and home-use pulse oximeters, as chronic disease management and interest in home-based care continue to evolve. Markets like South Africa and Saudi Arabia are emerging as key contributors, shaping the region’s expanding role in the global landscape.

The market was valued at USD 2.7 Billion in 2024.

The market is projected to grow at a CAGR of 7.0% from 2025 to 2033.

conventional technology segment holds the largest market share.

North America region is expected to witness the highest growth rate.

Major players include Medtronic, Masimo, Philips, GE Healthcare, Nonin Medical, and Nihon Kohden.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Pulse Oximeter Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Pulse Oximeter Market,By Sensors Type

5.3 Pulse Oximeter Market, By End User

5.4 Pulse Oximeter Market,By Technology Type

6.1 The Dental Radiography Market, By Country

6.1.1 Pulse Oximeter Market,By Sensors Type

6.1.2 Pulse Oximeter Market, By End User

6.1.3 Pulse Oximeter Market,By Technology Type

6.2 U.S.

6.2.1 Pulse Oximeter Market,By Sensors Type

6.2.2 Pulse Oximeter Market, By End User

6.2.3 Pulse Oximeter Market,By Technology Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping