Regulatory Affairs Outsourcing Market

Regulatory Affairs Outsourcing Market Share & Trends Analysis Report, By Service Type (Regulatory Consulting, Regulatory Writing & Publishing, Legal Representation, Product Registration & Clinical Trial Applications, Regulatory Submission, Regulatory Operations, Other Services), By Category (Pharmaceutical Drugs, Biologics, Medical Devices, Other Industries), By Indication (Oncology, Neurology, Cardiology, Immunology, Others), By Product Stage (Preclinical, Clinical, Post-Market Authorization (PMA)), By End-User (Pharmaceutical Companies, Biotechnology Companies, Medical Device Companies)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

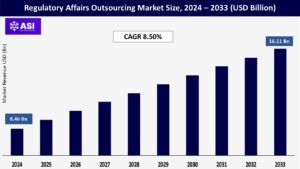

CAGR: 8.50%

Last Updated : August 21, 2025

The global Regulatory Affairs Outsourcing Market was valued at approximately USD 8.46 billion in 2024 and is projected to reach USD 16.11 billion by 2033, growing at a CAGR of 8.50% during the forecast period (2025–2033).

The Regulatory Affairs Outsourcing Market involves services provided by third-party vendors to support pharmaceutical, biotechnology, and medical device companies in complying with regulatory requirements across different regions. These services encompass regulatory strategy development, dossier preparation, submission of documents to authorities like the FDA, EMA, or CDSCO, and post-market surveillance compliance. The main use of regulatory outsourcing is to help healthcare companies navigate complex and ever-evolving regulatory landscapes efficiently, reduce operational costs, accelerate product approvals, and focus on core competencies such as R&D.

Key properties of this market include high domain expertise, real-time tracking of regulatory changes, cross-border regulatory knowledge, and integrated technology platforms for document management and submission. Outsourcing is especially prevalent among small to mid-sized companies and in emerging markets, where in-house regulatory expertise may be limited.

With continuous updates and differing regulations across regions (e.g., EU MDR, FDA regulations, CDSCO in India), staying compliant has become more complex and resource-intensive. Many life sciences companies especially small and mid-sized firms lack the in-house expertise or infrastructure to manage this complexity. As a result, they turn to regulatory outsourcing partners to ensure that products are approved on time and compliant with ever-evolving local and international standards.

In a competitive healthcare environment, speed to market is critical. Regulatory affairs outsourcing allows companies to streamline the approval process by leveraging expert partners with region-specific regulatory knowledge and experience. These vendors can navigate submission pathways, handle documentation, and respond to regulatory queries efficiently, reducing delays and allowing faster product launches, which is especially crucial in high-growth sectors like biologics, personalized medicine, and medical devices.

A major concern for companies outsourcing regulatory affairs is the risk of exposing sensitive intellectual property (IP) and confidential data to third parties. Since regulatory dossiers often contain proprietary scientific data, manufacturing processes, and clinical trial results, outsourcing increases the vulnerability to data breaches or misuse.

Additionally, not all outsourcing partners may consistently maintain quality and regulatory standards, leading to compliance risks, delays in approvals, or even rejections by regulatory bodies. This has made some companies hesitant to fully trust third-party vendors, thereby restraining market growth.

The Regulatory Affairs Outsourcing Market is segmented by Service Type, Category, Indication, Product Stage and End User. Each factor plays a crucial role in accelerating time-to-market for life-saving therapies, ensuring regulatory compliance across diverse global jurisdictions, and enabling healthcare companies to focus on innovation while maintaining high standards of safety and efficacy.

The market is divided into Regulatory Consulting, Regulatory Writing & Publishing, Legal Representation, Product Registration & Clinical Trial Applications, Regulatory Submission, Regulatory Operations, and Other Services. Among these, Regulatory Consulting holds a major share due to the increasing complexity of global regulations and the need for strategic guidance during product development and market entry.

Regulatory Writing & Publishing and Regulatory Submission are also in high demand as companies aim to ensure high-quality, error-free documentation that complies with various regulatory authorities like the FDA, EMA, and PMDA. Legal representation and clinical trial application services are particularly important for companies entering new international markets where local representation is a regulatory requirement.

The market is segmented into Pharmaceutical Drugs, Biologics, Medical Devices, and Other Industries. Pharmaceutical drugs dominate the category due to the sheer volume of products in the pipeline and the stringent regulatory processes they must undergo. However, the biologics segment is growing rapidly, driven by the rise of complex therapies such as monoclonal antibodies and gene therapies, which require specialized regulatory knowledge.

Medical devices also represent a significant share, especially with the increasing regulatory requirements introduced under frameworks like the EU MDR and IVDR, prompting many companies to seek expert support.

The market covers Oncology, Neurology, Cardiology, Immunology, and Others. Oncology leads due to the high number of cancer therapies in development and the urgency associated with fast-tracking life-saving treatments, especially under accelerated pathways. Neurology and cardiology follow closely, supported by rising global prevalence of neurodegenerative and cardiovascular diseases. Each indication demands tailored regulatory strategies, making outsourcing critical for timely and compliant submissions.

The market is divided into Preclinical, Clinical, and Post-Market Authorization (PMA) phases. The clinical stage holds the largest share, as it involves the most rigorous regulatory oversight, including trial protocols, ethics submissions, and ongoing regulatory interactions.

However, the post-market phase is gaining momentum with increased focus on pharmacovigilance, safety updates, and lifecycle management. The preclinical phase also contributes significantly, especially for companies needing regulatory guidance during early development and IND (Investigational New Drug) submissions.

The market is segmented into Pharmaceutical Companies, Biotechnology Companies, and Medical Device Companies. Pharmaceutical companies represent the largest client base due to their extensive product pipelines and the critical need to maintain regulatory compliance across multiple markets.

Biotechnology firms, often smaller in size, are increasingly relying on outsourcing to reduce costs and gain access to specialized regulatory expertise. Meanwhile, medical device companies are seeking support to navigate evolving global device regulations and streamline the approval process for both legacy and innovative devices.

North America, especially the United States, leads the regulatory affairs outsourcing market due to complex FDA regulations, a strong pharmaceutical industry, and a high number of clinical trials. Companies outsource to accelerate market entry and ensure compliance with changing regulatory frameworks.

Europe is a mature market driven by strict regulatory standards such as the EU MDR (Medical Device Regulation) and EMA’s evolving guidelines. Countries like Germany, Switzerland, and the UK have a strong presence of outsourcing service providers. Outsourcing helps firms navigate pan-European requirements more efficiently.

Asia-Pacific is witnessing explosive growth, particularly in India, China, and Singapore, due to low operational costs, skilled workforce, and growing pharmaceutical and biotech sectors. Multinational companies increasingly rely on Asia-Pacific firms for cost-effective dossier preparation, submissions, and regulatory monitoring.

Latin America shows increasing demand for regulatory outsourcing, especially in Brazil, Argentina, and Colombia, where regulatory complexity and localization challenges encourage companies to partner with local experts. Rising clinical trials and generics manufacturing boost the market.

The MEA region is gradually evolving with regulatory frameworks becoming more defined in countries like Saudi Arabia and South Africa. However, outsourcing is still limited due to a smaller base of local providers and less harmonized regulations compared to other regions.

The regulatory affairs outsourcing market was valued at USD 8.46 billion in 2024.

The market is projected to grow at a CAGR of 8.50% from 2025 to 2033.

The Pharmaceutical Drugs hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include IQVIA Inc., Parexel International Corporation and ICON plc.

1.1 Summary

1.2 Research methodology

2.1 Particulate Adjuvants

2.2 Aluminum-Based Adjuvants

2.3 Toll- Like Receptor Agonists

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Regulatory Affairs Outsourcing Market , By Application

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Regulatory Affairs Outsourcing Market, By Product Stage

6.1 North America , Regulatory Affairs Outsourcing Market, By Country

6.1.1 Regulatory Affairs Outsourcing Market , By Application

6.1.2 Regulatory Affairs Outsourcing Market, By Service Type

6.2 U.S.

6.2.1 Regulatory Affairs Outsourcing Market , By Application

6.2.2 Regulatory Affairs Outsourcing Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping