Rehabilitation Equipment Market

Rehabilitation Equipment Market Share & Trends Analysis Report By Product Type (Mobility Equipment, Daily Living Aids, Exercise Equipment, Therapy Equipment) By End User (Hospitals & Clinics, Rehabilitation Centers, Home Care Settings, Physiotherapy Centers, Nursing Homes) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

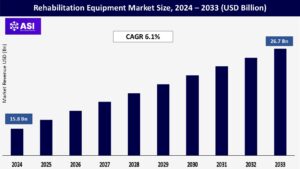

CAGR: 6.1%

Last Updated : March 7, 2026

The global Rehabilitation Equipment Market was valued at approximately USD 15.8 billion in 2024 and is projected to reach USD 26.7 billion by 2033, growing at a CAGR of 6.1% during the forecast period (2025–2033).

Rehabilitation equipment is an incredible service as it can aid in restoring functional mobility and improved quality of life for a person recovering from an injury, surgical intervention, a stroke or those with chronic conditions. Rehabilitation equipment consists of mobility assistive devices like wheelchairs and walkers, daily living assistive devices, body support systems and therapeutic machines used in physical and occupational rehabilitation.

This equipment is incredibly important to use with both inpatient and outpatient clients and in residential/homecare settings. Rehabilitation equipment can cover all age groups from the aging population to individuals who have lifelong disabilities. Currently, the biggest market catalysts are the growing aging population, the rising incidence of neurological and musculoskeletal disorders, and a growing focus on post-acute care or rehabilitation at home.

There are also new advances in rehabilitation technology such as robotic rehabilitation systems and smart therapy devices that are also a strong contributor plus we have evolving healthcare infrastructure in developed economies and a stronger support of reimbursement.

The ever-increasing global aging population is considered the central driving force behind the rehabilitation equipment market. Aging, in general, is associated with higher levels of musculoskeletal disorders, strength and balance impairments, post-stroke disabilities, and chronic conditions that limit mobility and function in the activities of daily living.

For example, it is projected that between 2022 and 2050, the number of persons aged 65 years or older will increase from 771 million to over 1.6 billion, representing almost 16% of the total global population according to the United Nations. As geriatric conditions become more prevalent, there has been a substantial increase in demand for mobility aids, such as walkers and powered wheelchairs, body support products, and home-based rehabilitation resources (Farah et al., 2022).

For example, the Invacare Corporation, a leading manufacturer of rehabilitation equipment, signals growing demand for lighter weight and ergonomically designed mobility support devices, from aged consumers in the North American and European markets.

In countries such as Japan, where more than 28% of the population is aged 65 years or older, there is an unprecedented accelerated increase in resources allocated for aged rehabilitation support products and services. The global economic and demographic paradigm shift continues identifying a greater need for reliable, user-friendly, and economical rehabilitation intervention for aging people.

The rising prevalence of stroke, traumatic brain injuries, and neurodegenerative conditions such as Parkinson’s disease and multiple sclerosis is driving increased demand for rehabilitation equipment. When it comes to disability, stroke is one of the most common causes of long-term disability around the world.

According to the World Stroke Organization, more than 12 million people each year have a stroke, and more than 60% of patients who experience a stroke will require some rehabilitation. To offset the burden of these disorders, hospitals and therapy centers are investing in modern therapeutic technologies. In 2023, Hocoma (a DIH Group company) launched a new version of the Lokomat robotic gait training system aimed at stroke and spinal cord injury patients who require gait assistance and counseling in the role of repeat motion therapy in recovery.

Also, neurorehabilitation clinics in the U.S., Germany and South Korea are increasing the use of virtual reality (VR) therapy systems, such as MindMaze and Rehametrics, when working with patients recovering from neurological disorders. This trend is creating increased demand for advanced exercise and adaptive exercise equipment as well as assistive devices and therapy supports required for long-term rehabilitation treatments.

One of the primary constraints that hampers the growth of the rehabilitation equipment market is the high cost of technological advanced equipment and the lack of adequate reimbursement in many areas. Robotic rehabilitation systems, computer-assisted gait trainers, and motorized therapeutic devices have better recovery outcomes, but they also have a cost. For example, robotic exoskeletons like the EksoNR from Ekso Bionics can easily exceed USD 100,000.

The high cost makes these devices impossible for many clinics and out of reach for individual users or smaller rehabilitation centres, particularly in developing economies. As a specific example, insurance companies often provide limited or no coverage for certain rehabilitation products, particularly for equipment that is used for home use, such as mobility scooters, hoists, or bathing aids.

In some countries, like India, Brazil, and parts of Africa, any government funding or private insurance would rarely consider funding rehabilitation tools, unless they consider an item is entirely essential after surgery. This limits access to a variety of rehabilitation tools for middle- to lower-income patients. Even in the United States, for example, Medicare will not consider certain assistive technology for home use and because of limited coverage will dissuade a homecare agency in selecting or recommending a technology.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Mobility Equipment Daily Living Aids Exercise Equipment Therapy Equipment

|

| By End User |

Hospitals & Clinics Rehabilitation Centers Home Care Settings Physiotherapy Centers Nursing Homes |

| Key Players |

Invacare Corporation Sunrise Medical LLC Medline Industries, LP Drive DeVilbiss Healthcare GF Health Products, Inc. Hill-Rom Holdings, Inc. (a part of Baxter International) Carex Health Brands (Apex Global) Ottobock SE & Co. KGaA Arjo AB Dynatronics Corporation Ekso Bionics Holdings, Inc. Hoveround Corporation Leckey (part of Sunrise Medical) Permobil AB Pride Mobility Products Corp. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Mobility Equipment is expected to dominate the traffic accident reporting market with the largest share in 2024, increasing rapidly with the increase in the incidence of mobility impairments linked to aging, stroke, spinal injuries, and debilitating chronic diseases like arthritis. Manual and powered wheelchairs, mobility scooters, and more basic mobility aids like walkers are being used increasingly by hospitals, home care and elderly care facilities.

Rapid developments in technology are creating opportunities for innovation in the product market (e.g. foldable electric wheelchairs, smart scooters), and demand is rising rapidly in developed markets. Daily Living Aids is the fastest growing segment of the trafffic accident reporting market, which is being driven by the rising demand for independent living with support from tools for elderly patients and chronically ill patients.

Daily Living Aids include tools for toileting aids, grooming, and eating, and importantly under this category there are tools designed for patients with cognitive impairments or patients with gross or fine motor dexterity. The growth of this segment is substantially driven by the rising trend towards home care and aging in placeBody Support Devices have undergone moderate growth and continuing trends of growth as body support devices become in higher demand for more patient handling in clinical and residential environments.

They fall into three categories: hoists, transfer slings, and therapeutic cushions (for preventing pressure ulcers and positioning patients safely). Hospitals and long-term care facilities used this market segment heavily in the last few years as they focus on preventing caregiver injury and improving patient safety. The rehabilitation segment, termed therapy equipment, is still in the process of gaining acceptance and adoption levels are rising as physiotherapy clinics and rehabilitation clinics embrace the continued processes of recovery and have adopted many of the therapy devices.

Some devices that fall into the rehab equipment category are continuous passive motion devices (CPM), resistance training, electrotherapy, and others. The growing demand of this segment can be traced back to the faster growing number of stroke survivors, sports injuries, and post surgical cases that need rehabilitation. The addition of robotics and virtual reality (VR) into therapy devices improves recovery outcomes and are appealing to patients and clients.

In 2024, hospitals & clinics will dominate the end user segment, as they are the main provider for patients undergoing post-operative and trauma rehabilitation. Hospitals & clinics have cutting-edge equipment and physical therapy equipment to treat patients, along with rehabilitation units, especially for tertiary and multi-specialty hospitals.

Rehabilitation Centers are also starting to be an important end user segment due to the increasing number of facilities focused on rehabilitation services, for physical, neurological, and occupational specialty areas. Rehabilitation centers provide long-term rehabilitation services and are utilizing more of the new technologies in rehabilitation, including robotic therapy and gait training.

Home Care Settings are the fastest-growing end users based on the understanding that healthcare is trending toward decentralized care, the aging population, and affordability of home-based rehabilitation devices. Patients prefer rehabilitation and recovery in their own home environment, along with mobility assist devices, daily living devices, and lightweight therapy devices.

Physiotherapy Centers still enjoy high volume demand, especially in urban areas and outpatient contexts. They not only receive patients recovering from injuries and sports related injuries but are also utilized by patients undergoing orthopedic rehabilitation, which typically requires targeted exercises and stimulation equipment.

Nursing homes will also be expanding their rehabilitation procedures, since they care for similar long-term patients with mobility issues as well as chronic conditions. The demand for hoists, wheelchairs, and adaptive equipment continues to increase with investment levels, particularly in markets like the U.S., Germany, and Japan which have a large number of aging populations.

North America has held the leading market share of 38.5% in 2024, due to its leading health care infrastructure, currently high uptake of assistive technologies, and growing elderly population.

The U.S. continues to be the leading contributor, with emphasis on post-acute care, home-based rehabilitation, and innovation in technological therapy equipment. Numerous market player companies, such as Invacare Corporation, Hill-Rom Holdings, and Sunrise Medical agree with view the rehabilitation approach of patient care heading to home-based care; improving facilities, and patient outcomes.

Moreover, favorable reimbursement policies and lack of resources for patients needing rehabilitation based on chronic illnesses for example stroke, arthritis, orthopedic injuries, also drive the ability of hospitals and home care patients to access the needed rehabilitation devices.

Europe is an important market bolstered by the graying population and funding for long-term care facilities. There is also adequate support to transit the case of geriatric patients, through public health systems for example Germany, France UK Italy, Sweden giving enough ability to provide mobility aids, therapy equipment and some daily living aids.

According to Eurostat the proportion of the population aged 65+ was over 21% of the EU population in 2023. There is needed rehabilitation services, which are impacting the large proportion of hospital patients with chronic illnesses and needed continuous rehabilitation.

In addition to government-funded programs to home and community based rehabilitation programs there is also affordable necessary tools are easily accessible in the home care rehabilitation space, in view of the decreasing adult population, that assists the ways the adult consumer gets access to key rehabilitation devices and tools today. Europe’s focus on preventative health care, quality of life and community will continue to grow this market.

The fastest growth is focusing on the Asia-Pacific region, which is projected to have a CAGR of 7.9% throughout the whole forecast period because of ongoing urbanization; a growing healthcare infrastructure; and a growing base of aging populations. China, India, Japan, and South Korea are driving this growth. Japan has one of the most significant segments of elderly citizens, and their government has focused funding towards assistive and rehabilitative technologies.

In India and China, the increasing burden of neurological diseases, orthopedic injuries, and incidences of stroke have increased the demand for physiotherapy and home-based care. The growing awareness of therapy solutions has empowered physiotherapists with higher disposable incomes;, along with the entrance of local manufacturers into the marketplace, has expedited this market growth.

Latin America and the Middle East & Africa have moderate growth as they continue to enhance their healthcare infrastructure and educate the public about health-related issues. Brazil, Mexico, South Africa, and the UAE are experiencing growing demands for rehabilitation services due to the ongoing rise of non-communicable diseases and road traffic injuries.

Government-funded initiatives, such as enhancing disability care and importing assistive devices, are bolstering the development of these two markets. Unfortunately, longer-term growth rates remain low in several areas of the Latin America region and Middle East & Africa region of the world due to challenges including irregularities to healthcare access, low penetration of insurance, and limited funding of services in rural areas.

The market was valued at USD 15.8 billion in 2024.

The market is projected to grow at a CAGR of 6.1% from 2025 to 2033.

The Mobility Equipment hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Invacare Corporation, Sunrise Medical LLC and Medline Industries, LP

1.1 Summary

1.2 Research methodology

2.1 Particulate Adjuvants

2.2 Aluminum-Based Adjuvants

2.3 Toll- Like Receptor Agonists

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Rehabilitation Equipment Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Rehabilitation Equipment Market, By End User

6.1 North America Rehabilitation Equipment Market, By Country

6.1.1 Rehabilitation Equipment Market, By Product Type

6.1.2 Rehabilitation Equipment Market, By End User

6.2 U.S

6.2.1 Rehabilitation Equipment Market, By Product Type

6.2.2 Rehabilitation Equipment Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping