Sepsis Diagnostics Market

Sepsis Diagnostics Market Share and Trend Analysis, By Technology (Molecular Diagnostics, Immunoassay, Microbiology, Flow Cytometry, Biomarkers), By Application (Bacterial Sepsis, Fungal Sepsis, Viral Sepsis), By End User (Hospitals, Pathology & Reference Laboratories, Research Laboratories) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

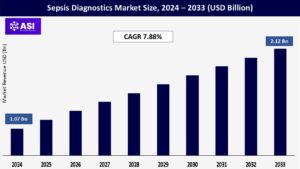

CAGR: 7.88%

Last Updated : April 2, 2026

The global sepsis diagnostics market size was valued at USD 1.07 billion in 2024 and is projected to reach USD 2.12 billion by 2033, expanding at a compound annual growth rate CAGR of 7.88% during the forecast period (2025–2033).

Sepsis diagnosis relies on various technologies and methods utilized to recognize and treat sepsis at an early stage, a disease that is lethal due to an overreaction of the body to infection. Sepsis arises when an immune reaction to infection results in tissue and organ damage, which, if left undiagnosed and untreated in good time, may result in organ failure and death.

Market demand is fueled by the increasing rate of sepsis globally, increased hospital-acquired infections, and sustained innovation in the diagnostics platforms. New diagnostic products of sepsis include blood culture media, molecular diagnostics, immunoassays, and biomarker tests that enable healthcare professionals to diagnose sepsis at an early stage and enhance patient outcomes by allowing timely intervention.

Artificial intelligence and machine learning applications in diagnostic devices are revolutionizing the diagnosis of sepsis with better and faster results that direct tailored treatment protocols.

An increase in hospital-acquired infection (HAI) rate is one of the key market drivers for the diagnosis of sepsis. HAIs infect millions of patients every year, and sepsis is a frequent complication that occurs. The chance of sepsis formation is most specifically greatest among patients of long-term hospitalization, critical care patients, and patients with immunocompromised states.

The COVID-19 pandemic increased the stakes even more, where the patients who were infected with the virus were at a greater chance of developing sepsis, and therefore, it became imperative that rapid diagnostic tests be available. Clinics all over the globe are spending considerable amounts of money on advanced diagnostic devices and enforcing rigid infection control measures to counter the growing wave of HAIs.

Sepsis inflicts more than a million patients yearly in the United States alone and kills hundreds of thousands, showing the importance of early diagnosis and treatment. Increasing HAIs’ burden is propelling healthcare professionals to develop new sepsis diagnosis solutions with faster and more precise results, thus triggering market growth.

Technological progress in sepsis diagnostics is revolutionizing the market and bringing unprecedented growth. Use of machine learning and artificial intelligence technology can be applied in diagnostic platforms to accelerate the speed and accuracy of diagnosing sepsis to an extent that health workers can identify patterns and predict the development of sepsis before clinical symptoms.

Molecular diagnostic technology, such as PCR and next-generation sequencing, has revolutionized pathogen detection by initiating a reduction in detection time from days to hours, thereby enabling earlier therapeutic interventions.

Point-of-care diagnostic device technologies have had particularly strong effects, enabling diagnostic capability to extend to bed and emergency room locations where timely information can direct life-and-death treatment.

Biomarker-based diagnosis has also expanded, with novel biomarkers more sensitive and specific in diagnosing sepsis compared to conventional markers. More and more companies are engaged in the creation of rapid diagnostic or point-of-care technologies that involve little or no staff regarding healthcare interaction, escaping the absence of skilled manpower while presenting precise diagnoses.

Such forms of technological advancements anywhere lead to sepsis diagnosis at an earlier point in time, more precise antimicrobial therapy, and improved patient outcomes, fueling continued investment and market growth.

Although the advantages to be gained from newer sepsis diagnostic technology are numerous, their cost is a very real barrier to mass deployment, particularly in regions of low resources. Molecular diagnostic platforms, due to diagnostic accuracy and speed, are too costly to install in the first instance and also come with maintenance and reagent costs.

This cost is most hard-hitting for developing countries and small health centers with minimal budgets for health. The cost element also includes the price of high-technology laboratory buildings and personnel trained to use sophisticated equipment and interpret complex test results.

Two, reimbursement issues in most healthcare systems discourage providers from buying the technologies since there is doubt about the return on investment. The economic gap between the developing and developed world also plays a role in creating the capability imbalance in managing sepsis.

Although point-of-care technologies can help conserve expenditures by reducing laboratory processing demands, most of these technologies remain costlier, and their accessibility is limited. The economic barrier hinders market penetration to a large extent in developing economies as well as rural health care environments, where sepsis causes the highest burden, but for which available economic resources are the worst.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Molecular Diagnostics Immunoassay Microbiology Flow Cytometry Biomarkers |

| By Application |

Bacterial Sepsis Fungal Sepsis Viral Sepsis |

| By End User |

Hospitals and Specialty Clinics Pathology and Reference Laboratories Research Laboratories Academic Institutes Contract Research Organizations |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Sepsis diagnostics market is technologically divided into biomarkers, molecular diagnostics, immunoassay, microbiology, and flow cytometry. Micro biology technology dominates the market at present with close to half the overall revenue because microbial culture is still the gold standard for sepsis diagnosis.

The procedure supplies end-to-end information on the bacterial strains and drug resistance, which is necessary for the optimized treatments depending upon the patient. The most rapidly expanding field is molecular diagnostics, which has the ability to detect pathogens quickly and effectively from clinical specimens.

Methods like PCR, next-generation sequencing, and others make it possible to detect bacterial, viral, and fungal DNA or RNA within hours using conventional methods, whereas earlier this took days. Immunoassay technology is able to detect rapidly particular antigens or antibodies that are responsible for the sepsis, and flow cytometry gives a glimpse of the activation and activity of immune cells during sepsis.

Biomarker tests such as procalcitonin and C-reactive protein tests are becoming the clinician’s first choice since they are able to detect both the presence and extent of inflammation and hence assist in the differentiation of sepsis from other illnesses.

Integration of these technologies with artificial intelligence and machine learning is also increasingly improving the speed and precision in diagnosis, revolutionizing sepsis care in hospitals worldwide.

Sepsis diagnostics market is segregated by application into bacterial sepsis, fungal sepsis, and viral sepsis, and out of these, bacterial sepsis has the largest market share in a greater percentage due to more frequency of occurrence and a greater mortality rate. Bacterial sepsis is further divided into gram-positive bacteria and gram-negative bacteria, both of which need special investigation to yield appropriate therapy.

The segment of bacterial sepsis is very much in demand due to the global burden of bacterial infection as well as the emergence of organisms resistant to antibiotics, and these need to be found in order to give effective therapy. Fungal sepsis, though less frequent, is becoming more prevalent, particularly among immunocompromised patients, and needs several diagnostic tests.

Viral sepsis has become more prominent since the COVID-19 pandemic, as it was realized that viral infections can cause sepsis by various mechanisms, and therefore, diagnostics were necessary to distinguish between pathogen types.

The multiplexing use is an indication of clinical requirement for pathogen-specific therapeutic agents and treatment, and therefore, technological advancement in multiplex technology has made it possible to detect varied pathogens simultaneously. Clinicians are gradually appreciating the fact that the etiologic pathogen responsible for sepsis must be identified at an early stage so as to guide focused treatment with improved outcome and reduced antimicrobial resistance.

This requirement is pushing and transforming research towards more comprehensive diagnostic platforms to detect the causative organism and its antimicrobial susceptibility pattern in a timely fashion.

Sepsis diagnostics market is divided based on end user into reference and pathology laboratories, research laboratories, contract research organizations, academic institutions, specialty hospitals, and clinics.

Specialty clinics and hospitals are the premium segment as they are exposed to the largest number of cases of sepsis and need immediate diagnostic solutions in intensive care units and emergency wings. These types of labs are now converting to point-of-care diagnostic solutions that facilitate quicker diagnosis and treatment initiation, leading to better outcomes in time-critical cases.

Pathology and reference laboratories are the most rapidly increasing segment, driven by growth due to the outsourcing of advanced diagnostic testing and their ability to provide high-volume testing with advanced technology and sophistication.

These laboratories can perform more advanced tests, such as molecular diagnosis and biomarker testing, not yet established in smaller facilities. Academic and research institutions play central roles in creating and calibrating novel diagnostic techniques, with ongoing development in the area.

The end-user perspective diagnoses the complex nature of sepsis diagnosis, where diverse healthcare environments apply complementary capabilities during diagnosis. The movement towards converged health systems is making the exchange of such end users’ data easier and is enabling more organized and coordinated sepsis care pathways.

North America is dominating the world in sepsis diagnostics market with the largest percentage because of high sepsis prevalence and well-established healthcare infrastructure. The United States is the biggest market for sepsis diagnostics in North America because of the absence of stringent reimbursement policies and government support for the research and prevention of sepsis.

Strong adoption rates for next-generation diagnostic tools and emphasis on early diagnosis and treatment of sepsis patients are seen in the region.

The second-largest European sepsis diagnostic market is fueled by stringent regulations for guaranteed testing procedures and rising healthcare expenditure. The UK is developing increasingly with the support of government programs to facilitate research into antimicrobial resistance and sepsis treatment.

The research in Europe and greater awareness campaigns have expedited the market with sepsis receiving topmost priority in healthcare.

Asia Pacific will be the most rapidly expanding sepsis diagnostics market with growth fueled by infectious disease incidence expansion, increasing healthcare awareness, and expenditures on healthcare in Japan, India, and China.

Expansion in the region is also facilitated by expanding internationalization of diagnostic firms as well as partnerships between local healthcare systems and strategic ones. Upgradation of healthcare infrastructure and public health anti-sepsis programs are providing humongous opportunities for expansion of the market.

LAMEA region, encompassing Latin America, the Middle East, and Africa, is gradually moving ahead in the sepsis diagnostics market. Brazil, Mexico, and Argentina are paving the way for Latin America’s growth through higher healthcare investment and rising awareness about sepsis management.

The Middle East, on the other hand, is bestowed with healthcare infrastructure expansion in the Gulf countries spurred by government policies. Whereas in the majority of Africa, access to high-tech diagnosis technology is limited by economic and infrastructural limitations, increased international partnerships and public health programs are increasingly enhancing diagnostic capacity, and as a result, LAMEA presents a potential market growing in size.

The global Sepsis Diagnostics Market was valued at USD 1.07 billion in 2024.

The market is projected to grow at a CAGR of 7.88 % from 2025 to 2033.

Microbiology hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include bioMérieux SA, Thermo Fisher Scientific Inc., Abbott Laboratories, Becton Dickinson and Company (BD), Roche Diagnostics, Danaher Corporation, T2 Biosystems, Luminex Corporation, Bruker Corporation, CytoSorbents Corporation.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Sepsis Diagnostics Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Sepsis Diagnostics Market, By Application

5.3 Sepsis Diagnostics Market, By End User

6.1 North America Sepsis Diagnostics Market, By Country

6.1.1 Sepsis Diagnostics Market, By Technology

6.1.2 Sepsis Diagnostics Market, By Application

6.1.3 Sepsis Diagnostics Market, By End User

6.2 U.S.

6.2.1 Sepsis Diagnostics Market, By Technology

6.2.2 Sepsis Diagnostics Market, By Application

6.2.3 Sepsis Diagnostics Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping