Single-Use Medical Device Reprocessing Market

Single-Use Medical Device Reprocessing Market Share & Trends Analysis Report, By Device Class (Class I Devices (e.g., laparoscopic graspers, scalpels, tourniquet cuffs),Class II Devices (e.g., pulse oximeter sensors, compression sleeves, catheters, guidewires)), By Application(General Surgery, Anesthesia, Arthroscopy & Orthopedic Surgery, Cardiology, Gastroenterology, Gynecologic, Urology, Others), By End User(Hospitals, Ambulatory Surgical Centers, Clinics & Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

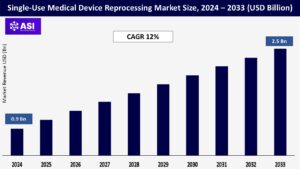

CAGR: 12%

Last Updated : August 21, 2025

The global Single-Use Medical Device Reprocessing Market was valued at approximately USD 0.9 billion in 2024 and is projected to reach USD 2.5 billion by 2033, growing at a CAGR of 12% during the forecast period (2025–2033).

The Single-Use Medical Device Reprocessing Market pertains to the segment of healthcare that focuses on the sterilization, testing, and reuse of medical devices originally labeled for single use. These include devices like compression sleeves, catheters, surgical instruments, and electrophysiology catheters. The primary use is to lower hospital costs and reduce medical waste by safely reprocessing certain devices without compromising patient safety. Key properties of this market include stringent regulatory oversight (particularly by agencies like the FDA), validated sterilization processes, rigorous testing for functional integrity, and compliance with standards like ISO 13485. Reprocessed devices must meet the same safety and performance standards as new devices. This market is gaining traction due to growing environmental concerns, increasing healthcare cost pressures, and strong evidence of cost-effectiveness and safety when performed by certified reprocesses.

Hospitals and healthcare providers are under intense pressure to reduce operating costs while maintaining high standards of care. Reprocessing single-use devices offers a significant cost-saving opportunity often allowing for reductions of 30–50% compared to the cost of new devices. This financial benefit is a strong driver, especially in developed markets where healthcare costs are rising, and in resource-constrained settings where budget optimization is essential.

There is a growing focus on sustainability in healthcare. Medical waste is a major environmental concern, and single-use devices contribute significantly to this problem. Reprocessing reduces the volume of biohazard waste and lowers the carbon footprint associated with the production of new devices. As hospitals, governments, and accrediting bodies set sustainability goals, the adoption of reprocessed devices is being increasingly supported, further driving market growth.

Reprocessing single-use medical devices is subject to strict regulatory scrutiny, especially in regions like Europe and some parts of Asia where such practices are either prohibited or heavily regulated. Even in the United States, where the FDA has established a clear pathway for reprocessing, manufacturers must adhere to rigorous testing, validation, and labeling standards.

Additionally, legal liabilities and hospital concerns about potential patient safety risks (real or perceived) can create hesitation among healthcare providers to adopt reprocessed devices. This regulatory complexity and fear of litigation act as a barrier to widespread acceptance and slow market expansion.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Device Class |

Class I Devices (e.g., laparoscopic graspers, scalpels, tourniquet cuffs) Class II Devices (e.g., pulse oximeter sensors, compression sleeves, catheters, guidewires) |

| By Application |

General Surgery Anesthesia Arthroscopy & Orthopedic Surgery Cardiology Gastroenterology Gynecologic Urology Others |

| By End User |

Hospitals Ambulatory Surgical Centers Clinics Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Single-Use Medical Device Reprocessing Market is segmented by Device class, Application and End User. Each factor plays a crucial role in reducing healthcare costs, promoting environmentally sustainable practices, and supporting the safe and effective reuse of high-quality medical devices in alignment with evolving hospital efficiency and waste reduction goals.

The market is categorized into Class I and Class II devices. Class I devices, such as laparoscopic graspers, scalpels, and tourniquet cuffs, are generally considered low-risk and are widely reprocessed due to their relatively simple design and low likelihood of compromising patient safety when properly sterilized.

However, the bulk of the market is held by Class II devices, which include more moderate-risk instruments such as pulse oximeter sensors, compression sleeves, electrophysiology catheters, guidewires, and more. These devices are more technologically advanced and require rigorous validation and quality assurance during the reprocessing cycle, but they offer substantial cost savings to healthcare providers and are therefore gaining wide acceptance in clinical practice.

The market spans General Surgery, Anesthesia, Arthroscopy & Orthopaedic Surgery, Cardiology, Gastroenterology, Gynaecology, Urology, and Others. General surgery is the leading application segment due to the high procedural volume and frequent use of reprocessable devices like graspers, scissors, and suction tips. Cardiology follows closely, particularly due to the increasing use of high-cost single-use devices such as electrophysiology catheters and diagnostic leads, which are now commonly reprocessed under strict regulatory compliance. Orthopaedic and arthroscopic procedures represent another significant area, where tools like shavers and burrs are reprocessed to minimize equipment cost.

Similarly, anesthesia, gastroenterology, and gynecology segments are seeing growth as hospitals seek to reduce waste and lower supply chain costs across a broader range of specialties. Urology and other specialties are also adopting reprocessed devices, especially in institutions committed to green healthcare initiatives and sustainability goals.

The market is segmented into Hospitals, Ambulatory Surgical Centers (ASCs), Clinics, and Others. Hospitals remain the largest end-user segment due to their higher patient volumes, broad surgical portfolios, and greater budgetary focus on cost containment. These institutions often have partnerships with third-party reprocessors or in-house reprocessing units, allowing them to standardize practices and ensure compliance with FDA and ISO regulations.

Ambulatory Surgical Centers are emerging as a fast-growing segment, driven by the shift toward day-care surgical procedures and a need for cost-effective device management without compromising safety. Clinics and other outpatient facilities also contribute to the market, especially in high-density urban regions where minimally invasive procedures are performed routinely and resource efficiency is critical.

North America, led by the U.S., is the largest and most mature market for device reprocessing. Strict FDA oversight ensures safety, and cost-saving pressures drive hospitals to adopt reprocessing on a large scale. Sustainability goals and established third-party reprocessors support robust market growth.

Europe has a mixed regulatory landscape, with some countries like Germany and the Netherlands allowing reprocessing under strict controls, while others, such as France, restrict or ban it. Still, rising environmental concerns and cost-efficiency goals push market growth where permitted.

The Asia-Pacific region is in the emerging phase, with growing interest in reprocessing to lower healthcare costs and reduce medical waste. India, Japan, and Australia are seeing gradual adoption, but the lack of clear regulatory frameworks and standardization hinders faster expansion.

Adoption in Latin America is moderate but growing, especially in Brazil, where healthcare providers are under budget constraints and are exploring reprocessing as a viable cost-reduction strategy. However, regulatory and cultural challenges remain barriers to wider uptake.

Reprocessing in this region is still limited. While hospitals in the UAE and Saudi Arabia are showing some interest, African nations face challenges in sterilization infrastructure and regulatory oversight, which slows adoption. Awareness campaigns and donor-funded programs could help introduce best practices over time.

The Single-Use Medical Device Reprocessing market was valued at USD 0.9 billion in 2024.

The market is projected to grow at a CAGR of 12% from 2025 to 2033.

Class I Devices hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Stryker Corporation, SterilMed, Inc. and Medline Industries, LP.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Single-Use Medical Device Reprocessing Market, By Device Class

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Single-Use Medical Device Reprocessing Market, By Application

5.3 Single-Use Medical Device Reprocessing Market, By End User

6.1 North America Single-Use Medical Device Reprocessing Market, By Country

6.1.1 Single-Use Medical Device Reprocessing Market, By Device Class

6.1.2 Single-Use Medical Device Reprocessing Market , By Application

6.1.3 Single-Use Medical Device Reprocessing Market, By End User

6.2 U.S.

6.2.1 Single-Use Medical Device Reprocessing Market, By Device Class

6.2.2 Single-Use Medical Device Reprocessing Market, By Application

6.2.3 Single-Use Medical Device Reprocessing Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping