Space Battery Market

Space Battery Market Share & Trends Analysis Report, By Type (Primary Batteries, Secondary Batteries), By Chemistry (Lithium-ion, Nickel-based, Silver-zinc, Others), By Application (Satellite, Launch Vehicle, Spacecraft, Rovers, Others), By End User (Commercial, Military, Government & Space Agencies, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Technology Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

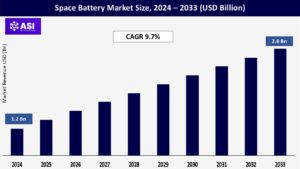

CAGR: 9.7%

Last Updated : November 29, 2025

The worldwide Space Battery Market had an estimated value of around USD 1.2 billion in 2024 and is anticipated to grow to USD 2.8 billion by 2033, reflecting a compound annual growth rate (CAGR) of 9.7% during the period from 2025 to 2033.

The Space Battery Market includes the design, production, and implementation of energy storage solutions utilized in space-related applications, such as satellites, spacecraft, launch vehicles, space stations, and planetary rovers. These batteries act as essential power sources for critical systems involved in navigation, propulsion, communication, telemetry, scientific instruments, and life support systems during launch, orbital operations, and deep space missions.

Space batteries are specifically designed to operate in harsh environmental conditions, including vacuum, microgravity, temperature variations, and high levels of radiation. They must provide high energy density, extended cycle life, durability against launch vibrations, and capabilities for deep discharge. As the global space economy continues to grow with the rise of commercial satellite megaconstellations, national defense initiatives, and exploration missions to the Moon, Mars, and beyond, the need for advanced battery technologies is witnessing significant increases.

The swift rollout of low Earth orbit (LEO) satellite networks aimed at providing worldwide internet, navigation, and remote sensing has led to a significant increase in the need for lightweight and highly efficient battery systems.

These batteries power satellites during periods of eclipse, orbital adjustments, and data transmission phases. Leading private aerospace companies and government entities are making substantial investments in these technologies to enhance the longevity, signal reach, and dependability of satellites.

Space organizations such as NASA, ESA, ISRO, and CNSA are ramping up initiatives aimed at exploring planets, establishing lunar bases, and conducting crewed missions to Mars.

These endeavors depend on secondary batteries to harness solar or RTG-generated energy, facilitating operations during the night, enabling rover movement, and powering scientific instruments. Batteries capable of enduring radiation, extreme temperatures, and functioning over extended mission periods are vital to these undertakings.

One of the main challenges in the space battery market is the elevated expenses linked to research, development, and implementation. Space batteries are required to adhere to strict performance, safety, and durability criteria to operate in extreme conditions such as deep space or low Earth orbit.

These batteries undergo thorough testing for radiation resistance, thermal stability, and long lifespan, which considerably raises R&D costs. Furthermore, the expense of integrating batteries into satellites or spacecraft and sending them into space is significant, often requiring partnerships with major space agencies or private aerospace firms.

These high initial costs can discourage new participants and hinder innovation. Additionally, the procurement and approval processes are frequently protracted, which delays the adoption and commercialization of new battery technologies, such as solid-state or lithium-sulfur options. This financial burden continues to pose a considerable obstacle to broader progress.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Primary Batteries Secondary Batteries |

| By Chemistry |

Lithium-ion Nickel-based Silver-zinc Others |

| By Application |

Satellites Launch Vehicles Spacecraft & Space Stations Rovers & Planetary Landers Others |

| By End User |

Commercial Military Government & Space Agencies Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The market for space batteries is categorized By Type (Primary Batteries, Secondary Batteries), By Chemistry (Lithium-ion, Nickel-based, Silver-zinc, Others), By Application (Satellite, Launch Vehicle, Spacecraft, Rovers, Others), By End User (Commercial, Military, Government & Space Agencies, Others).

Lithium-ion batteries lead the market because of their high energy density and dependability. Satellites account for the largest segment within the platform category, fueled by a growing need for extended space missions and communication systems.

The space battery market encompasses various battery types, primarily categorized into primary (non-rechargeable) and secondary (rechargeable) batteries. Among these categories, secondary batteries particularly lithium-ion are becoming increasingly favored due to their ability to be recharged, their high energy density, and their extended lifespan.

Conversely, primary batteries, such as silver-zinc and thermal batteries, are utilized in situations that demand reliable, single-use power bursts, like in launch vehicles or emergency systems.

Space batteries play essential roles in various space missions. The satellite sector leads in application share, driven by an increasing need for communication, Earth observation, and navigation satellites. The launch vehicle sector is also important, as it requires high-power batteries for short durations to support ignition and control systems.

Furthermore, spacecraft, rovers, and space stations such as the ISS depend significantly on advanced batteries for propulsion, communication, and life-support systems. The growth of interplanetary missions and lunar exploration further broadens the range of applications.

Lithium-ion batteries are the most commonly used technology because of their excellent energy-to-weight ratio, making them suitable for space payloads where weight is crucial. These batteries are recognized for their minimal self-discharge, extended cycle life, and ability to function in low-gravity environments.

Nickel-based batteries, such as nickel-cadmium and nickel-hydrogen, were historically favored for their durability and resistance to radiation but are slowly being phased out. Although silver-zinc batteries are costly, they provide a very high energy density and are frequently selected for critical or short-term missions.

Solid-state batteries are emerging as a promising alternative because of their safety and the potential to offer greater energy density.

The primary end users in the space battery sector comprise government space agencies (such as NASA, ISRO, ESA, and Roscosmos), defense organizations, and commercial space firms (including SpaceX, Blue Origin, OneWeb, and satellite operators).

Due to the significant costs and the crucial roles space batteries play in missions, government and defense sectors remain the predominant purchasers. Nonetheless, commercial businesses are rapidly increasing market demand, particularly in the areas of satellite constellations and reusable launch systems.

North America leads the global space battery market, fueled by substantial government funding, sophisticated aerospace capabilities, and a growing commercial space industry. The United States stands out as a global frontrunner, thanks to key space organizations such as NASA and the US Space Force, as well as private companies like SpaceX, Lockheed Martin, Boeing, and Northrop Grumman.

The rising frequency of satellite launches—encompassing defense satellites and broadband internet constellations—intensifies the demand for high-performance lithium-ion and solid-state batteries.

Strong research and development efforts, along with partnerships between public and private sectors, have established North America as a center for innovative space-grade batteries. Additionally, the presence of local battery manufacturers and supportive policies aimed at space exploration further strengthen the region’s leadership.

Europe accounts for a considerable portion of the space battery market, bolstered by initiatives from the ESA (European Space Agency) and robust aerospace sectors in nations such as Germany, France, and the UK. Countries in Europe are channeling investments into Earth observation satellites, telecommunications, and space-based defense systems, all of which depend on dependable energy storage solutions.

Manufacturers in Europe focus on environmental sustainability and performance, leading to an increased interest in next-generation solid-state and lithium-sulfur battery technologies. Additionally, joint missions between the ESA and companies like Airbus Defence and Space and Thales Alenia Space drive the need for sophisticated space batteries.

The European Union’s commitment to technological independence and its financial backing for space research and development further enhance the region’s market standing.

The space battery market in the Asia-Pacific area is witnessing significant growth due to heightened investments in space initiatives from countries like China, India, Japan, and South Korea.

China is at the forefront of regional advancements with its proactive approach to satellite launches, crewed missions, and lunar exploration, supported by organizations such as CAST (China Academy of Space Technology) and CASC.

India, via ISRO, is expanding its satellite infrastructure and gearing up for ambitious projects like Gaganyaan and Chandrayaan. Japan’s JAXA and South Korea’s KARI are also dedicating resources to satellite and space station initiatives.

The increasing number of government and private aerospace enterprises, along with the development of local manufacturing capabilities, positions the Asia-Pacific as an exciting and potential-rich area for space battery integration.

Latin America represents an emerging market with a reasonable growth outlook in space technologies. Nations such as Brazil, Argentina, and Mexico are allocating resources towards small satellite launches and are establishing regional space initiatives.

Brazil, which hosts the National Institute for Space Research (INPE), is at the forefront of satellite deployment in the region. Nevertheless, challenges arise due to limited funding and infrastructure.

Collaborations with international space agencies and private investments in telecommunications satellites might facilitate the faster adoption of space batteries in the upcoming years.

The Middle East and Africa are experiencing steady progress in space exploration. The UAE is prominent with its Mars mission and its investments via the Mohammed bin Rashid Space Centre (MBRSC).

Similarly, Saudi Arabia is ramping up its emphasis on space technology as part of its Vision 2030 initiative. Although Africa is still at an early stage, nations like Nigeria and South Africa are investigating satellite technologies for communication and weather monitoring.

As regional governments improve their space capabilities through international partnerships and educational programs, the demand for space batteries is expected to grow.

The market was valued at USD 1.2 billion in 2024.

The market is projected to grow at a CAGR of 9.7% from 2025 to 2033.

Secondary (rechargeable) lithium-ion batteries dominate due to their widespread use in satellites and spacecraft.

Asia-Pacific is expected to grow the fastest, driven by ISRO, CNSA, and commercial satellite constellations.

Leading players include Saft Groupe, EaglePicher, GS Yuasa, EnerSys, and Amprius Technologies.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Space Battery Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Space Battery Market, By Chemistry

5.3 Space Battery Market, By Application

5.4 Space Battery Market, By End User

6.1 North America Space Battery Market , By Country

6.1.1 Space Battery Market, By Type

6.1.2 Space Battery Market, By Chemistry

6.1.3 Space Battery Market, By Application

6.1.4 Space Battery Market, By End User

6.2 U.S.

6.2.1 Space Battery Market, By Type

6.2.2 Space Battery Market, By Chemistry

6.2.3 Space Battery Market, By Application

6.2.4 Space Battery Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping