Specialty Resins Market

Specialty Resins Market & Trends Analysis Report, By Type (Epoxy Resins, Unsaturated Polyester Resins, Vinyl Resins, Polyamide and Others), By Application (Construction, Automotive, Electronics and Electricals), By End Use (Original Equipment Manufacturers (OEMs), Contractors, Consumers)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

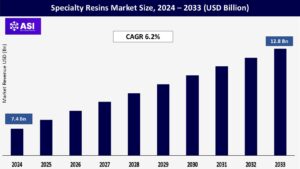

CAGR: 6.2%

Last Updated : March 7, 2026

The global Specialty Resins Market was valued at approximately USD 7.4 billion in 2024 and is projected to reach USD 12.8 billion by 2033, growing at a CAGR of 6.2% during the forecast period. Specialty resins are engineered polymers tailored for advanced performance across specific applications, offering benefits such as chemical resistance, thermal stability, mechanical strength, and weatherability.

Market growth is driven by increased demand across end-use sectors such as automotive, construction, aerospace, electronics, and marine, along with growing trends in lightweight materials, high-performance coatings, and green building practices.

Largescale infrastructure projects and the increasing rate of urbanization, especially in developing nations in Asia-Pacific, Latin America, and Africa, are greatly increasing the demand for specialty resins.

Because of their remarkable bonding strength, resistance to corrosion, and capacity to tolerate harsh environmental conditions, these materials are widely utilized in coatings, adhesives, composites, and sealants. They are essential to contemporary construction methods because of their ability to improve structural longevity and performance.

The car industry is moving toward lighter materials due to stricter emission laws and fuel economy norms. Because they offer significant weight reduction without sacrificing mechanical strength, heat resistance, or chemical durability, specialty resins including polyamides, vinyl esters, and epoxies are being employed more and more to replace metal components.

The use of specialized resins in body panels, structural elements, and under-the-hood parts is increasing as a result of this trend.

Because of their intricate manufacturing procedures, unique raw materials, and stringent quality control standards, specialty resins are substantially more costly than commodity resins.

Their adoption is restricted by these high manufacturing costs, especially in industries where prices are a concern and among small and medium-sized businesses (SMEs) that do not have the funds to purchase premium material solutions.

Environmental restrictions are becoming more and more strict for many specialty resins, particularly those that include formaldehyde, solvents, or other hazardous materials. Manufacturers have difficulties with VOC emissions, non-recyclability, and end-of-life disposal.

Market expansion is hampered by the increased burden of R&D expenditure, process optimization, and regulatory reporting resulting from compliance with regulatory frameworks including REACH (Europe), EPA (USA), and comparable standards around the world.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Epoxy Resins (Dominant Segment) Unsaturated Polyester Resins Vinyl Resins Polyamide and Others |

| By Application |

Construction (Largest Market) Automotive Electronics and Electricals |

| By End-Use |

Original Equipment Manufacturers (OEMs) Contractors Consumers |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Specialty Resins Market is segmented by Function (Acidulant, Emulsifier, Diuretic), By End-Use (Food & Beverage, Pharmaceuticals, Personal Care, Industrial).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Epoxy Resins (Dominant Segment)

Because of their remarkable mechanical strength, chemical resistance, and adhesive qualities, epoxy resins hold the biggest market share among specialty resins. Their demand is further supported by applications in wind turbine blades, composite materials, and high-performance adhesives. They are widely utilized in electronics, aerospace, and industrial coatings.

Unsaturated Polyester Resins

UPRs are prized for being easy to process, inexpensive, and having good mechanical performance. Common uses include the production of watercraft, sanitary ware, automobile parts, and construction panels. Additionally, they are an essential component of fiberglass-reinforced plastics (FRPs).

Vinyl Resins

Vinyl esters offer superior corrosion resistance and thermal stability. They are extensively used in marine, chemical storage tanks, and piping systems. Their high performance in corrosive environments supports demand from the oil & gas and chemical industries.

Polyamide and Others

Polyamides are perfect for mechanical parts, electronic connectors, and automotive under-the-hood parts because of their exceptional wear resistance, thermal stability, and structural strength. Bismaleimides, cyanate esters, and phenolic resins are examples of other specialty resins that are used in high-temperature and aerospace-grade applications where superior performance is crucial.

Construction (Largest Market)

The usage of specialty resins in floor coatings, sealants, concrete adhesives, and waterproofing systems makes the construction sector the largest application segment. Modern infrastructure and green building programs require these resins since they improve a building’s fire retardancy, weather resistance, chemical resistance, and durability.

car specialty resins are being used more and more in the car industry for electrical housings, interior trimmings, adhesives, and lightweight structural elements.

Their capacity to lighten vehicles without sacrificing mechanical integrity helps the industry meet its targets for pollution control and fuel economy. The demand for resin systems that are high-voltage robust, flame-retardant, and thermally conductive is rising in tandem with the electric vehicle (EV) industry’s explosive growth.

Electronics and Electricals

The automotive sector is increasingly adopting automobile specialty resins for lightweight structural components, adhesives, interior trims, and electrical housings. Their ability to reduce vehicle weight without compromising mechanical integrity aids the industry in achieving its fuel efficiency and pollution reduction goals.

The rapid expansion of the electric vehicle (EV) industry is driving up demand for resin systems that are thermally conductive, flame-retardant, and high-voltage resistant.

Original Equipment Manufacturers (OEMs)

OEMs are a significant end-user group that employs specialty resins in the design and manufacture of high-performance parts for a variety of industries, including industrial machinery, electronics, automotive, and aerospace. The necessity for materials that provide precision, durability, and regulatory compliance is what drives their demand.

Contractors

Specialty resins are widely used by contractors, especially in the infrastructure and construction industries. These materials provide important advantages like weather resistance, lifespan, and structural protection in both residential and commercial applications, and are frequently utilized in coatings, sealants, adhesives, and waterproofing systems.

Consumers

The consumer segment includes DIY users and small-scale applications, where specialty resins are used in paints, adhesives, sealants, and home improvement products. Growing awareness of premium and environmentally friendly materials is gradually influencing consumer choices in this space.

Asia-Pacific dominates the specialty resins market, both in terms of volume and growth rate. Countries such as China, India, and those in Southeast Asia are witnessing rapid industrialization, infrastructure development, and automotive production, driving robust demand.

The presence of major domestic resin manufacturers, low production costs, and rising consumption across construction, automotive, and electronics sectors contribute to the region’s strong market expansion.

North America remains a key market, led by the United States, with strong demand from aerospace, defense, electronics, and automotive industries. Growth is supported by increasing investments in electric vehicles (EVs) and sustainable construction materials, along with regulatory support for low-VOC and recyclable resins.

Europe’s specialty resins market is shaped by stringent environmental regulations, especially concerning VOC emissions and recyclability. This has driven innovation in bio-based and eco-friendly resin formulations. Germany, France, and the UK are major contributors, with significant usage in automotive, construction, and marine applications.

These regions are experiencing moderate growth, fueled by infrastructure development and urbanization in countries like Brazil, Mexico, UAE, and Saudi Arabia. However, import dependency, raw material price volatility, and limited local manufacturing capabilities continue to pose challenges to sustained growth.

USD 7.4 billion

6.2%

Epoxy Resins in the Construction and Automotive sectors

Asia-Pacific, due to infrastructure development and electronics production

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Specialty Resins Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Specialty Resins Market, By Application

5.3 Specialty Resins Market, By End-Use

6.1 North America Specialty Resins Market , By Country

6.1.1 Specialty Resins Market, By Type

6.1.2 Specialty Resins Market, By Application

6.1.3 Specialty Resins Market, By End-Use

6.2 U.S.

6.2.1 Specialty Resins Market, By Type

6.2.2 Specialty Resins Market, By Application

6.2.3 Specialty Resins Market, By End-Use

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping