Sterilization Equipment Market

Sterilization Equipment Market Share & Trends Analysis Report, By Product (Heat Sterilizers (Autoclaves, Dry‑Heat), Low‑Temperature Sterilizers (EO, H₂O₂ Gas Plasma), Radiation Sterilization Devices, Filtration Sterilizers, Sterilization Accessories (Indicators, Pouches, Lubricants)), By Method of Sterilization (Steam Sterilization, Dry Heat Sterilization, Chemical Sterilization, Radiation Sterilization, Filtration), By End-User (Hospitals & Clinics, Pharmaceutical & Biotech Companies, Medical Device Manufacturers, Food & Beverage, Laboratories & Research Institutes), By Operation Site (On‑site Sterilization, Off‑site Sterilization Services), By Technology (Conventional Systems, Automated & Integrative Systems, Portable & Mobile Units)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

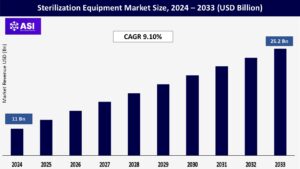

CAGR: 9.10%

Last Updated : August 20, 2025

The global Sterilization Equipment Market was valued at approximately USD 11 billion in 2024 and is projected to reach USD 25.2 billion by 2033, growing at a CAGR of 9.10% during the forecast period (2025–2033).

The Sterilization Equipment Market encompasses a broad range of devices and technologies used to eliminate all forms of microbial life—including bacteria, viruses, fungi, and spores—from medical instruments, laboratory tools, pharmaceutical products, and other sensitive materials. These devices are critical in healthcare, biotechnology, food processing, and research industries to ensure safety, prevent infections, and maintain product integrity.

Common sterilization methods include steam sterilization (autoclaves), dry heat, ethylene oxide (EtO) gas, hydrogen peroxide vapor, and gamma irradiation. Each method has specific properties: for example, autoclaves are highly efficient for heat-resistant instruments, while EtO gas is ideal for delicate, moisture-sensitive devices due to its low-temperature efficacy. Sterilization equipment is characterized by its reliability, efficiency, adaptability to different load types, and compliance with stringent international standards such as those from the FDA, ISO, and WHO.

The growing need for infection control, the rise in hospital-acquired infections (HAIs), and the expansion of surgical procedures and pharmaceutical manufacturing are key drivers propelling this market. As healthcare systems globally emphasize patient safety and product sterility, the demand for innovative, automated, and eco-friendly sterilization technologies continues to rise.

One of the most significant drivers of the sterilization equipment market is the increasing prevalence of hospital-acquired infections (HAIs), also known as nosocomial infections. These are infections that patients acquire during the course of receiving treatment for other conditions within a healthcare facility.

Common types include bloodstream infections, urinary tract infections, and surgical site infections. According to the World Health Organization (WHO), hundreds of millions of patients are affected by HAIs worldwide each year, leading to significant mortality and economic losses.

To combat HAIs, hospitals and clinics are under immense pressure to maintain strict infection control protocols. Sterilization of surgical tools, medical devices, and hospital environments is a critical component of these protocols. This has led to increased adoption of advanced sterilization equipment that ensures comprehensive microbial elimination.

Moreover, regulatory bodies like the U.S. Centers for Disease Control and Prevention (CDC) and European Centre for Disease Prevention and Control (ECDC) have enforced stringent sterilization guidelines, further pushing healthcare institutions to invest in modern and compliant sterilization systems.

The global rise in surgical interventions and the use of complex reusable medical devices is another powerful driver of the sterilization equipment market. Factors such as an aging population, a rise in chronic diseases (e.g., cancer, cardiovascular disorders, and orthopedic conditions), and increasing access to advanced healthcare have resulted in a surge in both elective and emergency surgeries. Each surgical procedure requires the use of sterile instruments to avoid complications and infections.

Additionally, the growing demand for minimally invasive surgeries and the widespread use of catheters, endoscopes, and implantable devices necessitate efficient and safe sterilization solutions. Many of these instruments are reusable and made of heat-sensitive materials, thus requiring advanced sterilization technologies such as low-temperature gas plasma, ethylene oxide, or radiation-based systems. This ongoing demand fuels continuous innovation in sterilization equipment, making the market highly dynamic and essential for modern healthcare infrastructure.

One of the primary restraints affecting the growth of the Sterilization Equipment Market is the high capital and operational cost associated with advanced sterilization technologies. Modern sterilization systems—such as low-temperature plasma sterilizers, ethylene oxide (EtO) sterilizers, and radiation-based sterilization units—are equipped with sophisticated automation, monitoring, and safety features.

While these systems offer high efficacy and compliance with stringent regulatory standards, they require significant upfront investment and regular maintenance, which can be financially burdensome, especially for small- and medium-sized healthcare facilities, clinics, and diagnostic labs.

In addition to the purchase cost, there are ongoing expenses related to consumables, energy consumption, installation of controlled environments (such as specially ventilated rooms for EtO), staff training, and periodic validation and calibration. Moreover, some methods like EtO sterilization face increasing regulatory scrutiny due to concerns about toxicity and environmental emissions, adding to the complexity and cost of compliance.

These economic and regulatory challenges can discourage adoption, particularly in developing countries or in resource-constrained settings where budgets for medical infrastructure are limited. As a result, many smaller facilities may continue to rely on basic or outdated sterilization methods, which may not meet evolving safety and efficiency standards, thus limiting market penetration.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product |

Heat Sterilizers (Autoclaves, Dry‑Heat) Low‑Temperature Sterilizers (EO, H₂O₂ Gas Plasma) Radiation Sterilization Devices Filtration Sterilizers Sterilization Accessories (Indicators, Pouches, Lubricants) |

| By Method of Sterilization |

Steam Sterilization Dry Heat Sterilization Chemical Sterilization Radiation Sterilization Filtration |

| By End User |

Hospitals & Clinics Pharmaceutical & Biotech Companies Medical Device Manufacturers Food & Beverage Laboratories & Research Institutes |

| By Operation Site |

On‑site Sterilization Off‑site Sterilization Services |

| By Technology |

Conventional Systems Automated & Integrative Systems Portable & Mobile Units |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Sterilization Equipment Market is segmented by Production, Method of Sterilization, End Users, Operation Site and Technology. Each factor plays a crucial role in strengthening infection control practices, driving the adoption of advanced sterilization technologies, and supporting the development of safer, faster, and more efficient sterilization solutions across healthcare, pharmaceutical, and research settings ultimately enhancing patient safety and ensuring compliance with global hygiene standards.

The market includes Heat Sterilizers, such as autoclaves and dry-heat sterilizers, which remain widely used in hospitals and laboratories due to their effectiveness and cost-efficiency for heat-resistant instruments. Low-Temperature Sterilizers, including ethylene oxide (EO) and hydrogen peroxide gas plasma systems, are growing in demand for their ability to sterilize heat- and moisture-sensitive devices.

Radiation Sterilization Devices—especially those using gamma rays and electron beams—are vital in pharmaceutical and disposable medical equipment sterilization. Filtration Sterilizers are commonly used for liquids and air-sensitive solutions in biotech and research applications. The Sterilization Accessories segment, comprising indicators, sterilization pouches, and lubricants, supports the main equipment by ensuring procedural accuracy and safety, thus also contributing significantly to recurring revenue streams.

Steam sterilization remains the gold standard, particularly in healthcare, due to its reliability and quick processing time. Dry heat sterilization is preferred for glassware and oils, while chemical sterilization, including EO and formaldehyde, serves temperature-sensitive tools. Radiation sterilization is increasingly used in bulk sterilization of single-use products in pharma and medical device manufacturing. Filtration sterilization is critical in sterile processing of solutions, vaccines, and lab samples.

Hospitals and clinics dominate the market due to high patient volume and surgical procedures requiring stringent sterilization. Pharmaceutical and biotech companies are major contributors, as regulatory requirements mandate sterile manufacturing environments. Medical device manufacturers also drive significant demand, especially for pre-market and post-production sterilization.

The food and beverage industry is an emerging segment, where sterilization ensures food safety and extends shelf life. Laboratories and research institutes require precise sterilization to prevent contamination in experiments and product development.

The market is divided into on-site sterilization, where hospitals and labs install their own sterilization units, and off-site sterilization services, which are increasingly used for large-scale, third-party sterilization—especially by pharma and device companies aiming to reduce operational burdens and meet regulatory outsourcing standards.

The market comprises conventional systems, such as manual autoclaves and EO chambers, which are widely used for routine processes. However, the demand for automated and integrative systems is rising, especially in high-throughput environments like pharmaceutical manufacturing and large hospitals, offering enhanced safety, efficiency, and traceability. Additionally, portable and mobile sterilization units are gaining traction in field hospitals, ambulatory centers, and during emergencies, providing sterilization flexibility in low-resource or remote settings.

The region holds the largest share of the sterilization equipment market, driven by a highly developed healthcare infrastructure, strong regulatory frameworks, and a high volume of surgical procedures. The United States, in particular, sees robust adoption due to the prevalence of hospital-acquired infections (HAIs), strict infection control guidelines set by bodies such as the FDA and CDC, and the presence of leading sterilization equipment manufacturers. In addition, the region benefits from rapid technological innovation, including automated sterilization systems and eco-friendly sterilization methods such as hydrogen peroxide plasma.

Follows closely, with countries like Germany, the UK, and France leading the adoption of sterilization equipment across both healthcare and pharmaceutical sectors. The region places significant emphasis on hygiene and safety, supported by stringent EU regulations for medical device reprocessing and environmental safety. Additionally, the aging population and increasing surgical procedures fuel demand. Government investments in healthcare modernization, especially in Central and Eastern Europe, are further propelling market growth.

Region is witnessing the fastest growth rate, fueled by expanding healthcare infrastructure, rising awareness of infection control, and increasing medical tourism in countries such as India, China, Japan, and South Korea. Rapid urbanization and government initiatives to upgrade hospitals and establish new healthcare facilities have led to higher demand for advanced sterilization technologies. Furthermore, the booming pharmaceutical and medical device manufacturing industries in countries like China and India contribute significantly to the market, as they require large-scale sterilization processes to meet export-quality standards.

The market is growing steadily, supported by improving healthcare systems and rising investments in hospital infrastructure, particularly in Brazil, Mexico, and Argentina. While economic constraints can limit widespread adoption of high-end sterilization systems, international aid programs and public-private partnerships are helping to introduce modern equipment, especially in tertiary care centers and government-run hospitals.

Region presents emerging opportunities, especially in the Gulf Cooperation Council (GCC) countries, such as Saudi Arabia and the UAE, which are heavily investing in advanced healthcare facilities as part of their long-term development strategies. However, much of Sub-Saharan Africa still relies on basic sterilization methods due to limited healthcare budgets and infrastructure. Nonetheless, increasing awareness of infection risks, support from international health organizations, and growing private healthcare investments are gradually improving market penetration in this region.

The market was valued at USD 11 billion in 2024.

The market is projected to grow at a CAGR of 9.10% from 2025 to 2033.

Heat Sterilizers hold the largest market share.

The North America and Europe region is expected to witness the highest growth rate.

Major players include Steris Corporation, Getinge AB and 3M Company

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Sterilization Equipment Market, By Product

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Sterilization Equipment Bronchoscopes Market, By Method of Sterilization

5.3 Sterilization Equipment Market, By End User

5.4 Sterilization Equipment Market, By Operation Site

5.5 Sterilization Equipment Market, By Technology

6.1 North America Sterilization Equipment Market , By Country

6.1.1 Sterilization Equipment Market, By Product

6.1.2 Sterilization Equipment Bronchoscopes Market, By Method of Sterilization

6.1.3 Sterilization Equipment Market, By End User

6.1.3 Sterilization Equipment Market, By Operation Site

6.1.3 Sterilization Equipment Market, By Technology

6.2 U.S.

6.2.1 Sterilization Equipment Market, By Product

6.2.2 Sterilization Equipment Bronchoscopes Market, By Method of Sterilization

6.2.3 Sterilization Equipment Market, By End User

6.2.3 Sterilization Equipment Market, By Operation Site

6.2.3 Sterilization Equipment Market, By Technology

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping