Surgical Sutures Market

Surgical Sutures Market Share and Trend Analysis, By Technology (Absorbable Sutures, Non-absorbable Sutures), By Application (General Surgery, Cardiovascular Surgery, Orthopedic Surgery, Gynecological Surgery, Ophthalmic Surgery, Other Applications), By End User (Hospitals, Ambulatory Surgery Centers, Clinics) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

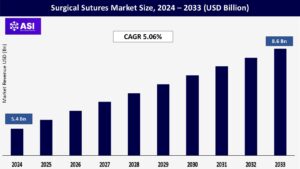

CAGR: 5.06%

Last Updated : April 2, 2026

The global surgical sutures market size was valued at USD 5.4 billion in 2024 and is projected to reach USD 8.6 billion by 2033, expanding at a compound annual growth rate CAGR of 5.06% during the forecast period (2025–2033).

Surgical sutures are still vital medical threads for bringing tissue edges together after injury or surgery, promoting hemostasis and facilitating quick healing of the wound with their availability in absorbable forms that lose tensile strength gradually and get enzymatic breakdown within weeks or months, making removal unnecessary, and non-absorbable forms usually extracted unless meant for permanent implantation.

These instruments, designed from natural fibers or newer synthetic polymers, are carefully chosen by surgeons according to certain tissue types, needed healing time, and procedural tolerance, with great emphasis on corresponding needle geometry, accurate suture caliber, and handling properties to reduce tissue trauma but maximize closure efficacy.

Continuing innovation, such as antimicrobial coatings fighting infection, barbed designs preventing knots, and new bioengineered fibers, expands their use substantially beyond routine surgery into specialty cardiovascular, ophthalmic, and gynecologic procedures.

This dynamic market environment undergoes strong growth fueled by increasing global surgical procedure volumes, increasing incidence of chronic wounds requiring closure, and the growing transition toward minimally invasive surgery methods, all generating high competition among seasoned industry titans and nimble new start-ups all competing to bring the next phase of advanced wound closure products meeting changing clinical needs.

Rising worldwide surgical volumes, spurred notably by demographic aging, are a prime market driver. Aging populations, growing at a rapid rate toward mid-century estimates, present increased vulnerability to degenerative disease processes requiring interventions such as joint arthroplasty, cardiovascular revascularization, and eye surgeries, all highly reliant on sutures for tissue approximation and secure closure.

Simultaneously, the increasing worldwide incidence of chronic diseases like diabetes drives demand for corrective procedures and advanced wound care interventions, further boosting suture usage in these areas.

Upgrade of healthcare infrastructure in developing countries further increases surgical access with progressive inclusion of advanced technology in routine care procedures. Ambulatory surgery centers and hospitals consistently expand procedural throughput capabilities in response to this growing demand, directly boosting usage of both absorbable and non-absorbable suture types.

Manufacturers strategically react by expanding production capacities, lengthening global distribution channels, and increasing education programs aimed at healthcare providers to maximize product choice and deployment effectiveness. Synergies between these factors jointly create a robust foundation demand pattern, providing for steady market growth in a variety of clinical environments and geographic areas.

Ongoing technical innovation is a key engine for growth, promoting competitive differentiation by way of enhanced suture functionality and increased clinical utility. Antimicrobial coatings using powerful drugs like triclosan or new biocidal molecules

significantly reduce surgical site infection risk by successfully preventing bacterial colonization, a critical innovation particularly useful in contamination sensitive procedures.

Barbed suture configurations, with microscopic barbs along filament lengths, obviate the conventional knot tying necessities, accelerate wound closure mechanisms, and provide even faster distribution of tension, benefits especially beneficial in minimally invasive and cosmetic surgical specialties.

Refinements in material sciences involving bioabsorbable polymers, such as polyglycolic acid, polylactic acid, and their sophisticated copolymers, allow for precise control of degradation kinetics along with better tensile strength retention profiles, to fit varied healing timelines.

Complementary needle design innovations, from reverse cutting geometries for durable fascial layers to highly specialized atraumatic designs for fragile vascular or neural tissues, maximize procedural efficiency and tissue compatibility.

These incremental material and design enhancements collectively drive surgeon adoption of higher-performance product tiers, capture favorable pricing matrices, and drive strong revenue expansion while meeting emerging clinical needs in increasingly specialized surgical fields.

Persistent cost-containment imperatives across healthcare systems globally act as a significant market restraint for surgical sutures. While sutures represent a minor component of overall procedural expenses, institutional budget constraints increasingly drive procurement toward economical generic alternatives rather than premium-priced branded innovations.

Reimbursement systems across many regions are inflexible, underpaying the additional expenses of sophisticated sutures such as antimicrobial-coated or barbed sutures, thus forcing surgeons to use traditional monofilament or multifilament sutures even if they have clinical benefits.

Growing markets, where high out-of-pocket spending by patients occurs, are also highly sensitive to price fluctuations, further restricting uptake of more valuable products. Producers thus have a difficult balancing act: large investments in research and development are necessary to ensure technological leadership and differentiate products, but affordability is key for broad market penetration.

This conflict stifles revenue opportunities in price-sensitive segments, especially where reimbursement policies fall short of product innovation cycles. As a result, although new sutures hold out the prospect of enhanced performance and procedural efficiencies, their value proposition is often undercut by budgetary constraints, retarding adoption rates and limiting growth curves in spite of proven clinical advantages.

Such unalignment between costs of innovation, reimbursement schemas, and purchasing priorities is therefore a persistent challenge to all stakeholders seeking to bring next-generation closure technologies to market.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Absorbable Sutures Non-absorbable Sutures |

| By Application |

General Surgery Cardiovascular Surgery Orthopedic Surgery Gynecological Surgery Ophthalmic Surgery Other Applications |

| By End User |

Hospitals Ambulatory Surgery Centers Clinics |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Surgical sutures are generally categorized into absorbable and non-absorbable categories, each with specific clinical uses depending upon their material behavior and application. Absorbable sutures are designed to degrade naturally inside the body over a specified period of time by enzymatic degradation or hydrolysis.

Removal of sutures is avoided by this process, and it is especially beneficial in internal operations like gastrointestinal anastomoses or gynecologic procedures. Polyglycolic acid (PGA), polylactic acid (PLA), and polydioxanone (PDO) are widely used and provide a controlled degradation rate and minimize postoperative complications.

Technological advancements have, over the years, resulted in absorbables with increased knot security, retention of tensile strength, and low tissue reactivity. Conversely, the non-absorbable sutures, which are usually made of nylon, polyester, polypropylene, or silk, maintain their tensile strength for an infinite period and are frequently used for exterior wound closure or surgical sites demanding extended mechanical stability.

Procedures such as vascular grafting, orthopedic ligament repair, and some neurosurgical repairs hinge significantly on the assurance and surety provided by the permanence of these sutures. Advances continue to refine both types with designs such as antimicrobial coatings, better pliability, and decreased memory.

Ultimately, clinical decision-making weighs durability, patient comfort, procedural setting, and cost-effectiveness against each other in selecting between these two foundation suture technologies.

The use of surgical sutures permeates a wide array of medical specialties, each needing specialized suture properties adapting to its procedural needs. In general surgery, sutures are used extensively for incision closure in abdominal, colorectal, and hernia repair operations.

These techniques require dependable handling, firm knot security, and very low risk of infection, necessitating both absorbable and non-absorbable materials. Cardiovascular operations are supported by ultra-fine monofilament sutures that can resist arterial pressure without inducing trauma or leakage.

Surgeons trust that materials such as polypropylene can provide the required strength and biocompatibility for operations such as coronary artery bypass grafting (CABG). Orthopedic operations entail high-strength tissue repair, especially of tendons, ligaments, and fascia.

Here, non-absorbable sutures of high tensile strength are used because of the physical trauma these tissues undergo after surgery. In gynecological surgery, specifically in uterine repair and laparoscopic hysterectomy, barbed absorbable sutures enhance efficiency by preventing knot tying and reducing closure time.

Ophthalmic surgeries, for instance, corneal transplants, require micro-gauge sutures that provide high precision without compromising the integrity of the tissues. Neurosurgery and pediatric procedures emphasize atraumatic manipulation and tissue irritation minimization, while in urology, some sutures are treated to minimize urinary calculus formation.

These varied uses spur ongoing design, material, and functionality innovation specific to each surgical specialty requirement.

User various types of healthcare facilities shape the surgical sutures market depending on their procedural volume, scope, and economic concerns. Hospitals are the biggest end users, performing a broad range of operations demanding reliable suture choices in many departments.

They hold a large stock of high-quality and regular sutures to support planned and urgent procedures. They tend to choose on the basis of quality, flexibility, and supplier continuity, with a willingness to try out new innovations providing better outcomes or procedure efficiency.

Ambulatory Surgery Centers (ASCs), specialized in elective, minimally invasive surgeries, are another expanding end-user market. ASCs conduct high volumes of procedures like arthroscopies, cataract removals, and laparoscopic cholecystectomies.

For them, time-saving devices such as barbed sutures are especially appealing because of their ability to save time in operating and enhance patient turnover. ASCs usually have more constrained budgets, so they look for something with advanced performance with affordability in return.

Clinics and out-patient care facilities serve minor surgical requirements, including mole removal, stitching of lacerations, or biopsies. They tend to prefer cost-effective absorbable suture material appropriate for short procedures.

Budget constraints, low procedural volumes, and space limitations dictate their buying behavior. This segment demands flexible product offers, customized pricing, and different support models from suppliers.

North America is still the largest market for surgical sutures, underpinned by established healthcare infrastructures and steady procedural demand. The U.S. and Canada enjoy quick take-up of new suture technologies, such as antimicrobial and knotless barbed sutures.

Beneficial reimbursement policies via Medicare and private payers enable hospitals and surgical facilities to make premium-quality product investments. FDA regulatory supervision guarantees steady product safety and efficacy, which stimulates manufacturers to innovate.

High consciousness, expert surgical specialists, and recurrent elective surgeries are responsible for continued market dominance. Strong R&D pipelines and extensive distribution networks help reinforce the area’s dominance in the international suture market.

Europe remains very much a part of the world’s leading surgical sutures market, driven by driver economies Germany, the U.K., France, and Italy. The area is focused on healthcare efficiency and quality, pushing product demand in the direction of those that reduce hospital stays and facilitate faster healing.

Policies based on ERAS (Enhanced Recovery After Surgery) have made the adoption of barbed and absorbable sutures mainstream. Public hospital networks and centralized procurement schemes allow for bulk purchases based on cost-effectiveness and clinical performance.

EU regulations also push high standards for products, forcing manufacturers to focus on innovation. Educational programs and surgical training fuel further product adoption.

Asia Pacific is becoming the fastest-growing market in the surgical sutures sector, led by growing healthcare accessibility and increasing procedure volumes in China, India, and Southeast Asia. Increased hospital infrastructure and growing insurance penetration ensure surgical services are more accessible to larger populations.

Government investments in rural care access and public health are key growth drivers. Local producers, usually in collaboration with international companies, are increasing production levels and enhancing affordability.

The sizeable patient base in the region, medical tourism in Thailand, as well as increasing sensitivity towards surgical hygiene, lead to increasing demand for sutures in both urban and semi-urban regions.

LAMEA, though having a lower market share, exhibits strong long-term growth potential. Brazil and Mexico are regional market leaders in Latin America, driven by the growth of a network of private and public hospitals, as well as growth in elective procedures. Medical tourism, particularly in bariatric and cosmetic procedures, underpins suture demand.

The Middle East and Africa have regional countries such as the UAE, Saudi Arabia, and South Africa investing in specialist surgical centers. Yet, obstacles such as restricted funding for healthcare, unequal distribution of surgical facilities, and cost-effective procurement practices discourage premium suture uptake. The emphasis lies on economical, affordable alternatives with minimum performance assurance.

The global Surgical Sutures Market was valued at USD 5.4 billion in 2024.

The market is projected to grow at a CAGR of 5.06 % from 2025 to 2033.

Absorbable sutures hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Ethicon (Johnson & Johnson), Medtronic, B. Braun Melsungen AG, Smith & Nephew, Boston Scientific Corporation, and Peters Surgical.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Surgical Sutures Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Surgical Sutures Market, By Application

5.3 Surgical Sutures Market, By End User

6.1 North America Surgical Sutures Market, By Country

6.1.1 Surgical Sutures Market, By Technology

6.1.2 Surgical Sutures Market, By Application

6.1.3 Surgical Sutures Market, By End User

6.2 U.S.

6.2.1 Surgical Sutures Market, By Technology

6.2.2 Surgical Sutures Market, By Application

6.2.3 Surgical Sutures Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping