T-Cell Lymphoma Market

T-Cell Lymphoma Market Share & Trends Analysis Report By Lymphoma Type (Peripheral T-cell Lymphoma (PTCL), T-cell Lymphoblastic Lymphoma (T-LBL)), By Therapy Type (Chemotherapy, Immunotherapy, Radiotherapy, Other Therapies), By Distribution Channel (Hospitals, Specialty Clinics/Cancer Centers, Diagnostic Laboratories, Research Institutes) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

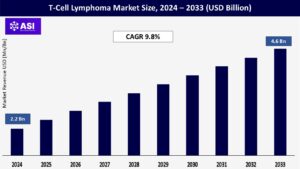

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIITR1006

CAGR: 9.8%

Last Updated : May 6, 2026

The worldwide T-Cell Lymphoma market size was valued at approximately USD 2.2 billion in 2024 and is projected to reach USD 4.6 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 9.8% during the forecast period of 2025–2033.

The T-cell lymphoma market is expected to grow rapidly between 2025 and 2033, fueled by a rising number of cases, breakthroughs in targeted treatments and immunotherapy, and greater investments in healthcare. As medical science advances and awareness improves, more patients are gaining access to innovative therapies that offer new hope for better outcomes.

Recent advances in diagnostic technology are transforming the way T-cell lymphomas are identified and treated. Tools like next-generation sequencing (NGS), immunophenotyping, and molecular testing have significantly improved diagnostic accuracy, allowing doctors to pinpoint the exact subtype of T-cell lymphoma more quickly and reliably. This means patients can begin the right treatment earlier, which is crucial for improving outcomes. At the same time, researchers are making great strides in genomic profiling and biomarker discovery, uncovering key genetic mutations such as TET2, RHOA, IDH2, and TP53 and identifying the molecular pathways involved in disease progression.

These insights are laying the groundwork for more personalized, targeted therapies. Instead of relying on a “one-size-fits-all” approach, clinicians can now tailor treatment plans to each individual’s unique genetic profile, increasing the chances of a successful response. This move toward precision medicine represents one of the most exciting and impactful shifts in the management of T-cell lymphomas.

The treatment landscape for T-cell lymphomas is rapidly evolving, with targeted therapies and immunotherapies offering new hope beyond traditional chemotherapy. Targeted therapies like Histone Deacetylase (HDAC) inhibitors (e.g., romidepsin and belinostat) and PI3K inhibitors are designed to specifically interfere with cancer cell signaling or gene expression. These therapies have shown encouraging results and may come with fewer systemic side effects compared to conventional chemotherapy.

In the realm of immunotherapy, monoclonal antibodies are playing a major role. Mogamulizumab (Poteligeo) targets CCR4, and brentuximab vedotin (Adcetris) targets CD30, both showing strong effectiveness in certain subtypes of T-cell lymphoma. While immune checkpoint inhibitors, such as PD-1/PD-L1 blockers, are not yet as widely used in this space as they are in other cancers, ongoing research suggests they may offer valuable treatment options in the near future.

One of the most exciting areas of innovation is CAR-T cell therapy, which involves engineering a patient’s own immune cells to fight cancer. Although still in the early stages of development for T-cell lymphomas, CAR-T therapies are already showing promise, particularly for relapsed or treatment-resistant cases, and are considered a key driver of future growth.

In addition, there’s a growing trend toward combination therapies pairing traditional chemotherapy with newer treatments like immunotherapy or targeted drugs, or integrating these therapies with stem cell transplantation to boost effectiveness and overcome treatment resistance. Altogether, these advancements are shaping a more personalized and hopeful future for patients with T-cell lymphoma.

One of the biggest challenges in treating T-cell lymphoma today is the extraordinarily high cost of advanced therapies, particularly immunotherapies like CAR-T cell treatments. These cutting-edge treatments offer new hope for patients, especially those with relapsed or hard-to-treat disease but that hope comes at a steep price.

A single infusion of CAR-T therapy can cost several hundred thousand dollars, and in some cases, the total cost per patient can even exceed $1 million USD. This creates serious barriers to access, especially in low- and middle-income countries (LMICs) where healthcare budgets are limited and access to advanced technologies is still developing. But even in wealthier nations, the financial strain on health systems and insurers can be considerable, often limiting how widely these treatments can be adopted.

A major reason behind the cost is the complex manufacturing process for CAR-T therapies, which involves extracting a patient’s own immune cells, genetically modifying them in a lab, and then reinfusing them after expanding the modified cells. This highly personalized, labor- and technology-intensive process adds significantly to the overall expense, making affordability and accessibility major concerns in the global fight against T-cell lymphomas.

T-cell lymphomas are highly complex and heterogeneous, encompassing a wide range of subtypes that differ in how they appear and behave. This diversity makes accurate and timely diagnosis particularly challenging. One major issue is that early-stage T-cell lymphomas, especially cutaneous T-cell lymphomas (CTCLs) can closely mimic benign skin conditions like eczema or psoriasis.

As a result, patients are often misdiagnosed or face significant delays, sometimes waiting years before receiving a correct diagnosis. Reaching a definitive diagnosis typically requires a multidisciplinary approach, involving collaboration between clinicians, dermatopathologists, and molecular specialists. These experts must analyze a combination of clinical signs, tissue samples, immunophenotyping, and molecular testing to piece together a clear picture.

Unfortunately, this level of specialized expertise and diagnostic capability isn’t consistently available, especially in less-resourced regions. Additionally, the lack of standardized diagnostic procedures, such as inconsistencies in immunostaining techniques, can further complicate and delay accurate diagnosis, ultimately affecting patient care and treatment outcomes.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Lymphoma Type |

Peripheral T-cell Lymphoma (PTCL) T-cell Lymphoblastic Lymphoma (T-LBL) |

| By Therapy Type |

Chemotherapy Immunotherapy Radiotherapy Other Therapies |

| By Distribution Channel |

Hospitals Specialty Clinics/Cancer Centers Diagnostic Laboratories Research Institutes |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The T-cell Lymphoma market is categorized by lymphoma type, by therapy, and by distribution channel. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and evolving sector within oncology, driven by increasing disease incidence, advancements in diagnostic techniques, and the development of novel therapies.

Peripheral T-cell Lymphoma (PTCL) represents the largest segment of the T-cell lymphoma market. It includes a diverse and often aggressive group of diseases that can be challenging to treat. One major subtype is Cutaneous T-cell Lymphoma (CTCL), which mainly affects the skin and includes well-known forms like Mycosis Fungoides (MF) and Sezary Syndrome (SS).

Another common subtype is Angioimmunoblastic T-cell Lymphoma (AITL), which often presents with systemic symptoms and immune system complications. Anaplastic Large Cell Lymphoma (ALCL) is also part of this group and can occur in both children and adults.

Beyond these, there are several less common subtypes such as Intestinal T-cell Lymphoma, Follicular T-cell Lymphoma, and Extranodal NK/T-cell Lymphoma, which typically involve organs outside the lymph nodes. In addition to PTCL, T-cell Lymphoblastic Lymphoma (T-LBL) is another aggressive type that primarily affects the thymus and bone marrow, and is often seen in younger individuals. Despite their differences, these subtypes all fall under the broader umbrella of T-cell lymphomas, each requiring tailored treatment strategies due to their unique clinical behaviors.

T-cell lymphoma treatment has traditionally relied on chemotherapy, particularly for aggressive forms such as Peripheral T-cell Lymphoma (PTCL) and Anaplastic Large Cell Lymphoma (ALCL). Chemotherapy remains a mainstay of clinical practice due to its long-standing effectiveness.

However, recent years have seen significant advances in immunotherapy, which is rapidly reshaping the treatment landscape. Monoclonal antibodies like mogamulizumab (Poteligeo) for cutaneous T-cell lymphoma (CTCL) and brentuximab vedotin (Adcetris) for CD30-expressing lymphomas are providing more targeted treatment options. Immune checkpoint inhibitors such as Keytruda and Opdivo are also gaining ground, helping the immune system recognize and fight cancer cells more effectively.

One of the most exciting developments is CAR-T cell therapy, which offers a personalized approach for patients with relapsed or refractory disease. Efforts are underway to reduce the time required to manufacture these therapies, making them more accessible. Radiotherapy remains an important tool, particularly for localized tumors or to provide palliative care in advanced stages. Stem cell transplantation, especially allogeneic transplants, continues to play a vital role in managing high-risk or relapsed cases, potentially offering long-term remission.

Additionally, targeted therapies such as histone deacetylase (HDAC) inhibitors, such as romidepsin and belinostat, work by altering gene expression in cancer cells, leading to their destruction. Other treatment options include antiviral therapies, which are especially relevant for HTLV-1-associated T-cell lymphoma, and topical treatments for cutaneous forms of the disease. Together, these evolving strategies reflect a more personalized and precise approach to managing T-cell lymphomas.

Hospitals are often the first stop for patients, serving as the main hubs for diagnosing and treating T-cell lymphoma. Specialty clinics and cancer centers provide more focused care, offering patients access to advanced therapies and expert support.

Diagnostic laboratories play a vital behind-the-scenes role, helping to confirm diagnoses and guide treatment through detailed molecular testing. Research institutes are where innovation happens, driving drug discovery and clinical trials that pave the way for better treatments in the future.

North America, and especially the United States, stands as the dominant force in the global T-cell lymphoma market. Several key factors contribute to this leadership. First, the region sees a relatively high prevalence of T-cell lymphoma, driving demand for effective treatments. The advanced healthcare infrastructure in the U.S. allows for earlier diagnosis, better disease management, and easier access to cutting-edge therapies.

Additionally, high healthcare spending supports the use of innovative, often costly treatments, such as immunotherapies and CAR-T cell therapies. The presence of many major pharmaceutical and biotech companies focused on cancer research further strengthens the region’s position. These companies are backed by robust research and development efforts, resulting in a strong pipeline of new therapies and a high volume of clinical trials.

The U.S. also benefits from a supportive regulatory environment, with mechanisms like the FDA’s orphan drug designation helping to speed up the development and approval of treatments for rare conditions like T-cell lymphoma. All of these elements contribute to a healthcare landscape where advanced therapies are not only developed but widely adopted, reinforcing North America’s leading role in the global market.

Europe holds a significant share of the global T-cell lymphoma treatment market and is poised for continued growth. Countries like Germany, the United Kingdom, and France are leading the charge, thanks to their strong healthcare systems and investment in cancer care.

As the cancer burden continues to rise across the continent, there’s an increasing demand for effective treatment options, including those for T-cell lymphomas. European healthcare providers are placing a strong focus on innovation, actively exploring new and more effective therapies. This includes the use of HDAC inhibitors, immune checkpoint inhibitors, and monoclonal antibodies, often in combination, to improve outcomes for patients.

Stem cell transplantation also remains a critical treatment pathway for those with high-risk or relapsed disease, and is well-integrated into standard care protocols. In addition, government support across Europe plays a key role—through policies aimed at cancer prevention, early diagnosis, and access to advanced treatments, regulatory bodies are helping to create an environment that supports both patient care and pharmaceutical innovation.

The Asia Pacific region is emerging as the fastest-growing market for T-cell lymphoma treatments, driven by a combination of medical, economic, and demographic factors. Awareness about T-cell lymphoma is steadily increasing, along with improvements in diagnostic tools, leading to earlier and more accurate detection.

At the same time, healthcare access is expanding, with many countries investing heavily in infrastructure and advanced medical services. The rising incidence of T-cell lymphoma, especially subtypes like HTLV-1 associated Adult T-cell Leukemia/Lymphoma, is particularly notable in Japan, where the disease burden is relatively high and the market is already well-established.

Meanwhile, countries like China and India are witnessing strong market momentum fueled by economic growth, a growing middle class, and rising healthcare spending. With large patient populations and evolving healthcare systems, many developing economies in the region offer untapped potential for future growth.

However, treatment approaches can vary widely across Asia Pacific, shaped by differences in healthcare infrastructure, regulatory environments, and patient demographics. Overall, China, Japan, and India are positioned to be the key drivers of this regional surge, with each contributing uniquely to the market’s rapid evolution.

The Middle East and Africa (MEA) region is showing promising growth in the T-cell lymphoma market, with several factors driving this upward trend. Healthcare investment is on the rise, as both governments and the private sector work to strengthen medical infrastructure and expand access to advanced treatments.

Notably, countries like Saudi Arabia have begun approving and offering CAR-T cell therapies, signaling a major step forward in bringing cutting-edge cancer treatments to the region. There’s also a growing emphasis on hematologic malignancies, including T-cell lymphomas, as awareness and specialized expertise increase. In the MENA region, Cutaneous T-cell Lymphoma (CTCL) often presents at a younger age and may show distinct clinical features, such as hypo- or hyperpigmented forms of Mycosis Fungoides, which call for tailored approaches to diagnosis and management.

Among MEA countries, Saudi Arabia and South Africa are emerging as leaders in the market, driven by strong healthcare initiatives and a commitment to expanding treatment options for complex diseases like T-cell lymphoma.

The T-Cell Lymphoma market was valued at USD 2.2 billion in 2024.

The T-Cell Lymphoma market is projected to grow at a CAGR of 9.8% from 2025 to 2033.

The Peripheral T-cell lymphoma (PTCL) segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 T-Cell Lymphoma Market, By Lymphoma Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 T-Cell Lymphoma Market, By Therapy Type

5.3 T-Cell Lymphoma Market, By Distribution Channel

6.1 North America T-Cell Lymphoma Market, By Country

6.1.1 T-Cell Lymphoma Market, By Lymphoma Type

6.1.2 T-Cell Lymphoma Market, By Therapy Type

6.1.3 T-Cell Lymphoma Market, By Distribution Channel

6.2 U.S.

6.2.1 T-Cell Lymphoma Market, By Lymphoma Type

6.2.2 T-Cell Lymphoma Market, By Therapy Type

6.2.3 T-Cell Lymphoma Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping