Temperature Sensor Market

Temperature Sensor Market Share & Trends Analysis Report, By Type (Thermocouples, Resistance Temperature Detectors (RTDs), Thermistors, Infrared Temperature Sensors, IC Temperature Sensors, Others), By Output (Analog, Digital), By End-Use Industry (Automotive, Healthcare, Industrial, Consumer Electronics, Aerospace & Defense, Food & Beverage, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

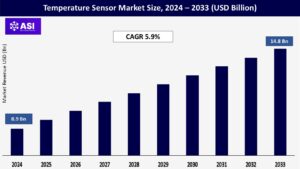

CAGR: 5.9%

Last Updated : November 29, 2025

The global market for temperature sensors was valued at USD 8.9 billion in 2024 and is expected to grow to USD 14.8 billion by 2033, with a compound annual growth rate (CAGR) of 5.9% from 2025 to 2033.

Temperature sensors are devices that detect thermal energy and convert it into readable information, which facilitates monitoring, control, and safety functions across various applications. These sensors play a crucial role in industrial automation, automotive climate management, medical diagnostics, consumer electronics, aerospace systems, and food safety monitoring.

The rapid growth of Industry 4.0, increasing demand for accurate process control in manufacturing, and strict safety regulations in sectors such as pharmaceuticals, aerospace, and food & beverage are propelling market expansion. Moreover, the rise of connected devices within IoT ecosystems—spanning from wearable health devices to smart home temperature controllers—has greatly broadened the range of temperature sensing technologies.

Innovations such as non-contact infrared temperature sensors, miniaturization for embedded electronics, and integration with wireless communication protocols have further increased the market’s potential. The trend of electrification in the automotive industry, the emphasis on energy-efficient buildings, and the healthcare sector’s dependence on remote patient monitoring solutions are also driving adoption.

The rise of smart devices, wearable technology, and advanced automotive systems significantly contributes to the growth of the temperature sensor market. In the realm of consumer electronics, temperature sensors play a crucial role in maintaining device safety, optimizing battery life, and improving user experience in items like smartphones, laptops, and fitness trackers.

In the automotive industry, the increasing transition to electric and hybrid vehicles has heightened the demand for temperature sensors, which are vital for monitoring battery packs, power electronics, and climate control systems within the cabin.

As the global movement toward connected and autonomous vehicles continues, manufacturers are incorporating more accurate and dependable temperature sensors to ensure optimal functionality and safety across diverse environmental conditions.

The industrial sector depends significantly on temperature sensors for managing processes, protecting equipment, and facilitating predictive maintenance, especially in areas such as manufacturing, chemical processing, and energy generation.

With the rise of Industry 4.0 and the adoption of industrial IoT, temperature sensors are increasingly integrated into connected monitoring systems, allowing for real-time analytics and improvements in efficiency. In the healthcare field, temperature sensors play a vital role in monitoring patients, aiding diagnostics, and managing the cold chain for pharmaceuticals and vaccines.

The COVID-19 pandemic hastened the implementation of non-contact temperature sensing solutions in medical facilities, workplaces, and public areas, and these developments continue to drive market growth.

An increasing focus on safety, energy efficiency, and product quality regulations across different sectors is anticipated to further enhance the demand for reliable and precise temperature sensing technologies.

One significant limitation in the temperature sensor industry is the difficulty in achieving high accuracy and stability over time, especially in harsh or varying environmental conditions. Sensors that are subjected to extreme temperatures, humidity, vibrations, or chemical exposure can suffer from drift, resulting in incorrect readings.

To maintain performance, regular calibration is required, but this leads to increased operational downtime and maintenance expenses, particularly in large industrial settings. Moreover, certain sensor types, like thermocouples, may exhibit slower response times or reduced accuracy at very low or high temperatures, which restricts their use in applications where precision is critical.

In highly regulated sectors such as pharmaceuticals or aerospace, even slight deviations can result in quality issues, compliance failures, or safety hazards. These performance-related challenges, coupled with the necessity for specialized calibration tools and skilled technicians, can impede adoption in cost-sensitive markets and slow the overall rate of widespread implementation.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Thermocouples RTDs Thermistors Infrared IC Sensors Others |

| By Output |

Analog Digital |

| By End-Use Industry |

Automotive Healthcare Industrial Consumer Electronics Aerospace & Defense Food & Beverage Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Temperature Sensor Market is segmented By Type (Thermocouples, Resistance Temperature Detectors (RTDs), Thermistors, Infrared Temperature Sensors, IC Temperature Sensors, Others), By Output (Analog, Digital), By End-Use Industry (Automotive, Healthcare, Industrial, Consumer Electronics, Aerospace & Defense, Food & Beverage, Others)

The market for temperature sensors is divided into several categories: Thermocouples, Resistance Temperature Detectors (RTDs), Thermistors, Infrared Sensors, and Semiconductor Sensors. In industrial and robust applications, Thermocouples are the most prevalent due to their wide operational temperature range and durability.

RTDs are favored in scenarios where accuracy is essential, such as laboratory testing and aerospace sectors. Thermistors provide high sensitivity within limited temperature ranges, making them ideal for consumer electronics and HVAC applications.

Infrared sensors are increasingly utilized in non-contact scenarios like medical thermometers, industrial safety monitoring, and food processing. Semiconductor sensors are widely employed in compact devices because of their small size, low energy consumption, and ability to be integrated easily.

Temperature sensors are divided into two categories: Analog Output and Digital Output. Analog sensors, which include thermocouples and RTDs, generate continuous voltage or current signals that correspond to temperature, providing versatility for a range of industrial applications.

On the other hand, digital sensors present temperature measurements directly in a digital format, minimizing the need for signal processing and enhancing precision.

The increasing adoption of microcontrollers and IoT devices in both industries and consumer electronics is fueling the demand for digital-output sensors, while analog sensors continue to see a strong demand in traditional and high-temperature settings.

The main end-user segments consist of Consumer Electronics, Automotive, Industrial, Healthcare, and Aerospace & Defense. The Consumer Electronics sector leads in demand volume due to the need for thermal monitoring in smartphones, wearables, and home appliances.

The adoption rates in the Automotive industry are increasing with the growth of electric vehicles, which utilize sensors for monitoring battery packs, engines, and HVAC systems. In the Industrial sector, temperature sensors are employed for optimizing processes, conducting predictive maintenance, and ensuring equipment safety.

Healthcare applications encompass devices for patient monitoring, laboratory equipment, and managing cold chains. The Aerospace and Defense sectors require highly accurate and rugged sensors capable of performing in extreme conditions, such as those found in avionics and military applications.

North America is a prominent regional market, driven by significant adoption of industrial automation, cutting-edge automotive research and development (including electric vehicles), and a high demand for healthcare and medical devices.

In particular, the United States demonstrates substantial investments in high-precision sensors utilized in aerospace applications, semiconductor fabrication plants, and automotive testing.

A robust network of distribution channels, a strong presence of suppliers, and ongoing investments in IoT and Industry 4.0 initiatives facilitate the transition from traditional analog sensors to smart digital sensors featuring embedded diagnostics. Recent regional forecasts indicate that North America is one of the largest revenue generators in the global market.

The European market is driven by the needs of the manufacturing, energy, and automotive industries. The implementation of stringent regulations regarding safety, emissions, and energy efficiency (such as building inspections, HVAC, and cold chain) promotes the use of high-precision RTDs and digital sensors.

Germany, France, and the UK are at the forefront of procurement and research and development, bolstered by a robust industrial automation sector in the region. Additionally, there is an increasing interest in sensor-driven predictive maintenance and smart grid solutions, with manufacturers preferring established and certified suppliers for sectors that are regulated.

The Asia-Pacific (APAC) region is the fastest-growing and largest market by volume. The surge in industrial development, significant manufacturing centers for electronics and automotive in countries like China, India, Japan, and South Korea, extensive smart-city initiatives, and heightened investment in healthcare are driving the demand for both affordable semiconductor sensors and premium industrial devices.

Local original equipment manufacturers (OEMs) and high-volume production in China and other APAC nations have contributed to price reductions, facilitating widespread adoption in consumer electronics, the automotive sector (including monitoring for electric vehicle batteries), and industrial Internet of Things (IoT) applications. Forecasts for growth in APAC consistently exceed those of other regions according to various market analyses.

Latin America continues to be a developing market driven by projects, experiencing moderate growth. Important sectors include mining, oil & gas, and utilities, where monitoring temperature is essential for safety and optimizing processes.

Brazil and Mexico are at the forefront of demand in the region, frequently acquiring sensors through project tenders or as part of modernization initiatives. In smaller economies, budget constraints and slower technology refresh rates limit adoption, resulting in growth that tends to be inconsistent and centered around large industrial initiatives.

Demand in the MEA region is primarily focused on the Gulf Cooperation Council nations and wealthy African markets. Key factors driving this demand include energy, oil and gas, and infrastructure security—especially for durable, high-reliability sensors and extended monitoring systems.

Both governments and energy firms are making investments in drone and robotic inspections, along with real-time monitoring systems for ensuring pipeline integrity and safety at plants. Although political instability and inconsistent procurement processes in certain nations hinder widespread adoption, significant defense and energy contracts still promote the need for precision and specialty sensors.

USD 8.9 billion in 2024.

Asia-Pacific.

Thermocouples, RTDs, thermistors, infrared sensors, and IC temperature sensors.

Automotive, industrial, healthcare, and consumer electronics.

Honeywell, TE Connectivity, Texas Instruments, STMicroelectronics, NXP Semiconductors.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Temperature Sensor Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Temperature Sensor Market, By Output

5.3 Temperature Sensor Market, By End-Use Industry

6.1 North America Temperature Sensor Market, By Country

6.1.1 Temperature Sensor Market, By Type

6.1.2 Temperature Sensor Market, By Output

6.1.3 Temperature Sensor Market, By End-Use Industry

6.2 U.S.

6.2.1 Temperature Sensor Market, By Type

6.2.2 Temperature Sensor Market, By Output

6.2.3 Temperature Sensor Market, By End-Use Industry

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping