Therapeutic Respiratory Devices Market

Therapeutic Respiratory Devices Market Share and Trend Analysis, By Technology Type (Mechanical Ventilators, CPAP & BiPAP Systems, Oxygen Concentrators, Nebulizers & Inhalation Therapy Devices, Humidifiers, Other Supportive Equipment), By Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Sleep Apnea, Cystic Fibrosis, Acute Respiratory Distress Syndrome (ARDS), Other Respiratory Indications), By End User (Hospitals & Clinics, Home Care Settings, Ambulatory Care Centers, Long Term Care Facilities, Other Specialized Institutions) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 8.3%

Last Updated : March 31, 2026

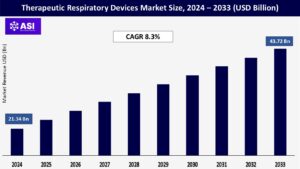

The global Therapeutic Respiratory Devices size market was valued at USD 21.34 billion in 2024 and is projected to reach USD 43.72 billion by 2033, expanding at a compound annual growth rate CAGR of 8.3% during the forecast period (2025 – 2033).

Therapeutic respiratory equipment encompasses a broad variety of devices essential to assist or restore normal breathing in patients with lung ailments. Some of the most significant examples are critical care mechanical ventilators, oxygen concentrators that supply purified oxygen, CPAP and BiPAP machines for the treatment of sleep apnea through keeping airways patent, nebulizers converting liquid medication into mist to be inhaled, humidifiers providing moisture to dry therapeutic air, and sophisticated air-filtration devices.

These devices treat chronic diseases such as COPD, severe asthma, cystic fibrosis, sleep apnea, and acute conditions such as ARDS. They do this by supplying controlled oxygen, administering aerosolized medication directly into the lungs, or with pneumatic pressure preventing collapsed airways during sleep.

Use is not limited to hospitals; these devices are now critical in outpatient facilities and, most importantly, increasingly in patients’ own homes. This transformation of decentralized, patient-driven care is driven by technologies that make devices more mobile, easier to use, and monitorable from a distance.

Patients treat complicated diseases every day with home ventilators, BiPAP machines, or portable oxygen concentrators. Proper installation and frequent utilization are crucial for success, often necessitating training. Routine cleaning and replacement of filters avoid infection and provide maximum performance.

This home-based strategy enhances quality of life and decreases hospitalization, but requires patient education and consistent support systems. Awareness of insurance coverage of these frequently needed devices is also crucial for long-term management.

Continued increases in chronic respiratory diseases – particularly COPD, asthma, and interstitial lung disease – continue to be the driving market force. Aging populations in high-income countries significantly raise dependence on long-term oxygen therapy and ventilatory support as lung function deteriorates.

At the same time, rapid industrialization and intense urban air pollution, especially within densely populated developing economies, expose huge populations to toxic levels of particulate matter, leading to the earlier onset of disease. This growing global patient burden places considerable strain on the health care system worldwide.

Hospitals are beset by severe capacity issues treating acute respiratory failures and exacerbations, while outpatient centers and home settings are dealing with unprecedented demand for devices that allow effective, long-term disease control.

This deeply rooted epidemiological trend, extensively forecasted to strengthen, forms the foundation for strong and resilient demand throughout the entire therapeutic device universe. The demand for management solutions generates adoption, from high-tech intensive care ventilators for acute emergencies through to portable oxygen concentrators and home nebulizers enabling daily functioning in chronic disease.

The accompanying high economic cost, including direct medical expenses and lost productivity, also justifies investment in these vital technologies. Particular pollution peaks in regional settings and seasonal changes similarly sharply stimulate demand for relief devices such as nebulizers and air cleaners.

Accelerating and relentless technology innovation profoundly reconfigures paradigms of respiratory care, acting as an influential driver of market growth. Major advancements in miniaturization, battery technology, and material science provides truly portable, ultralight oxygen concentrators along with highly compact and almost noiseless CPAP/BiPAP machines, freeing patients from institutional or home detention.

Critically, the incorporation of advanced multi-parameter sensors, solid wireless communication (Bluetooth, cellular), and end-to-end telehealth platforms enables unprecedented continual remote clinician monitoring.

This allows for real-time monitoring of therapy compliance, accurate mask fit, sophisticated respiratory patterns, blood oxygen saturation, and possible system integrity problems. Adaptive intelligent pressure algorithms maximize effectiveness and comfort through real-time adjustment of support levels across sleep stages or activity.

Secure, user-friendly mobile applications and cloud-based analytics enable patient self-management yet deliver clinicians granular data for tailored therapy optimization as well as early detection of adverse trends or clinical deterioration.

These technologies demonstrably raise safety standards, increase therapeutic efficacy, and significantly enhance patient convenience and quality of life.

As a result, the persuasive movement toward patient-oriented home care, fueled by empowerment and significant decreases in expensive hospitalizations and readmissions, drives tremendous expansion in the home respiratory equipment industry. Government support of home-based models and innovations, minimizing device upkeep impediments, further drives the change.

Substantial market growth is curbed due to the high cost of advanced therapeutic respiratory devices. State-of-the-art mechanical ventilators, high-specification non-invasive ventilation (NIV) devices such as BiPAP machines, and bundled platforms with real-time telemonitoring functionality have exorbitantly high front-end purchase costs.

This cost constraint significantly constrains adoption, especially in under-resourced healthcare institutions of low- and middle-income countries (LMICs) and for individual patients without proper insurance coverage.

Reimbursement policies in most areas are inconsistent, complicated, or provide only partial reimbursement, short of the actual cost of these cutting-edge technologies.

Even in well-resourced healthcare systems of developed countries, chronic financial constraints on hospital procurement units and tight reimbursement ceilings often defer or deny the purchase of next-generation equipment. In addition, maintenance fees, necessary consumables (masks, filters, tubing), and necessary servicing contribute significant long-term financial loads.

This cost restraint considerably retards overall market penetration, postpones the necessary replacement cycle of old legacy gear, and inhibits patient access to the most effective treatments. As such, while there is a strong underlying clinical need and demand for enhanced patient outcomes, the high total cost of ownership is a substantial brake on market growth.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology Type |

Mechanical Ventilators CPAP & BiPAP Systems Oxygen Concentrators Nebulizers & Inhalation Therapy Devices Humidifiers Other Supportive Equipment |

| By Application |

Chronic Obstructive Pulmonary Disease (COPD) Asthma Sleep Apnea Cystic Fibrosis Acute Respiratory Distress Syndrome (ARDS) Other Respiratory Indications |

| By End Use |

Hospitals & Clinics Home-Care Settings Ambulatory Care Centers Long-Term Care Facilities Other Specialized Institutions |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The respiratory therapy market is segmented according to discrete technology solutions for diverse clinical demands. Mechanical ventilators assist patients with serious respiratory failure through invasive or non-invasive support, offering highly controlled breathing for mostly intensive care unit environments, such as during pandemics or catastrophes.

CPAP and BiPAP devices provide critical non-invasive positive airway pressure treatment, regulating breathing at night for obstructive sleep apnea and treating respiratory insufficiency; technology advances continually enhance patient interface convenience and compliance monitoring.

Concentrators of oxygen are a critical market segment, producing therapeutic oxygen from the surrounding air for patients with continuous or ambulatory supplemental oxygen dependence because of hypoxemia, with battery-powered portable units allowing more freedom of movement.

Nebulizers and inhalation therapy equipment allow effective aerosolized medicine delivery directly into the lungs, essential for treating asthma attacks, COPD exacerbations, and cystic fibrosis; newer mesh nebulizers improve drug delivery efficiency.

Humidifiers provide sufficient moisture in therapeutic gases delivered, which improves patient comfort and airway protection, especially during long-term ventilation. Other supporting equipment includes advanced air-filtration systems for environmental management and various monitoring accessories such as pulse oximeters.

Each technology modality meets distinct therapeutic needs throughout the spectrum of acuity, ranging from acute intervention to control of chronic disease, as a result of continuous innovation in respiratory therapy.

Chronic obstructive pulmonary disease is a leading application sector, fueling long-term demand for oxygen concentrators, nebulizers, and non-invasive ventilation devices to treat symptoms and control recurring exacerbations, with special emphasis on quality of life enhancement and avoidance of hospitalization.

Asthma control is another key application area, critically dependent upon nebulizers and inhalers for acute relief as well as maintenance treatment, with extreme focus on pediatric asthma and severe adult asthma management.

Sleep apnea treatment, based largely on CPAP and BiPAP machines, constitutes a high and growing segment driven by increased rates of diagnosis and greater recognition of concomitant cardiovascular comorbidities.

Cystic fibrosis treatment requires specialized airway clearance devices and nebulizers for daily mucus removal and antibiotic administration, part of multicomponent care plans. Acute respiratory distress syndrome requires advanced mechanical ventilation techniques in critical care settings, employing lung-protective strategies.

Other important applications include the management of respiratory complications of neuromuscular diseases, treatment of pandemic-induced respiratory infections, care of patients throughout post-operative recovery, and treatment of novel conditions such as long COVID respiratory sequelae.

Market dynamics across each application are inherently tied to prevalence of disease, standard clinical practice, and documented effectiveness of device intervention in enhancing patient outcomes and quality of life, propelling directed technological advancement.

Hospitals and clinics represent the biggest traditional segment, especially for high-acuity products such as sophisticated mechanical ventilators in intensive care units, emergency departments, and operating rooms for critical life support, and also substantial volumes of nebulizers and oxygen delivery systems for general wards.

Home care settings account for the most rapid growth end user channel, driven by the intersection of patient desire to be treated in familiar settings, technology that supports safe and effective home use, and systematic forces encouraging the reduction of expensive hospitalizations.

Demand here is focused on transportable oxygen concentrators, CPAP/BiPAP devices, home ventilators, and small nebulizers. Ambulatory care centers employ devices for diagnostic testing and outpatient therapy sessions, such as pulmonary function equipment and nebulizer treatments.

Long-term care centers need equipment to support residents of chronic respiratory diseases, usually including fixed oxygen systems and simple nebulizers. Rehabilitation centers and specialty respiratory care clinics are other specialized centers, which have particular equipment needs based on patient populations and models of care. The trend towards decentralized care continues to underpin the strategic significance of the home care segment.

North America is the leading region for global therapeutic respiratory devices, fueled by high healthcare spending, advanced reimbursement systems (particularly Medicare/Medicaid), and strong adoption of advanced home-based care products.

The United States has the highest regional revenue, spearheaded by large numbers of sleep apnea and COPD cases, extensive use of portable oxygen concentrators, and state-of-the-art integrated CPAP/BiPAP systems with telemonitoring.

Substantial presence of large device manufacturers, early embracement of technology, facilitating regulatory routes (FDA), and patient affinity for minimally invasive home treatments further solidify its position. Massive investment in digital health infrastructure enhances remote management capabilities in both acute and chronic respiratory care environments.

The mature nature of the market in Europe is aided by well-established universal healthcare programs, strict regulatory harmonization under EU MDR, and high awareness of diseases. Germany, the UK, and France are the most important national markets, with high penetration of oxygen therapy and non-invasive ventilation.

Rising focus on cost control and aging populations propel investments in telemedicine platforms and remote patient monitoring solutions, especially for managing increasing COPD and asthma burdens.

Government programs encouraging home care and reimbursement models increasingly favoring outpatient management underpin steady market development, albeit with involved procurement procedures.

The Asia Pacific market showcases the highest world growth, driven by fast-growing healthcare access, major government programs addressing extreme air pollution, growing disposable incomes, and rising disease diagnosis rates.

China and India are core growth drivers, with demand skyrocketing in heavily polluted urban areas for affordable portable oxygen concentrators, nebulizers, and simple CPAP machines.

Enhancing hospital infrastructure, increased healthcare investments, increased awareness about sleep disorders, and attempts to decentralize the delivery of care are major contributors. Local production is on the rise, making it more affordable and accessible through various economic segments.

These markets are emerging economies with growth being limited by fragmented healthcare infrastructure, meager reimbursement coverage, and wide economic disparities. Yet, targeted public health initiatives for endemic tuberculosis, pneumonia, and air pollution/biomass cooking fuel hazards are propelling incremental demand for necessary devices.

Needs are concentrated around affordable oxygen concentrators, simple nebulizers, and minimum ventilation equipment for hospitals. Government procurement, NGOs, and incremental expansion in healthcare availability provide growth opportunities, especially in more urbanized regions and larger economies such as Brazil, Mexico, Saudi Arabia, and South Africa. Challenges persist in rural access and maintaining maintenance programs.

The global Therapeutic Respiratory Devices Market was valued at USD 21.34 billion in 2024.

The market is projected to grow at a CAGR of 8.3 % from 2025 to 2033.

Mechanical ventilators hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include E Healthcare Technologies Inc., Koninklijke Philips N.V., ResMed Inc., Fisher & Paykel Healthcare Limited, Medtronic plc, Drägerwerk AG & Co. KGaA, ICU Medical (Smiths Medical), Invacare Corporation, Becton Dickinson & Company (BD), and Getinge AB.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Therapeutic Respiratory Devices Market, By Technology Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Therapeutic Respiratory Devices Market, By Application

5.3 Therapeutic Respiratory Devices Market, By End User

6.1 North America Therapeutic Respiratory Devices Market, By Country

6.1.1 Therapeutic Respiratory Devices Market, By Technology Type

6.1.2 Therapeutic Respiratory Devices Market, By Application

6.1.3 Therapeutic Respiratory Devices Market, By End User

6.2 U.S.

6.2.1 Therapeutic Respiratory Devices Market, By Technology Type

6.2.2 Therapeutic Respiratory Devices Market, By Application

6.2.3 Therapeutic Respiratory Devices Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping