Third Party Logistics (3PL) Market

Third Party Logistics (3PL) Market Size, Share & Trends Analysis Report By Mode of Transport (Ground/Roadways Transport, Air Transport), By Industry Vertical (Manufacturing, Automotive), By Service (Domestic Transportation Management (DTM), International Transportation Management (ITM)) market Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

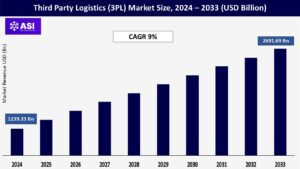

CAGR: 9%

Last Updated : December 16, 2025

The global third-party logistics (3PL) market size revenue was valued at USD 1239.33 billion in 2024. It is projected to reach from USD 1350.87 billion in 2025 to USD 2691.69 billion by 2033, growing at a CAGR of 9% during the forecast period (2025-2033).

Third-party logistics (3PL) is the method of outsourcing warehouse management operations, inventory operations, and shipping services across the globe. These services also augment the order fulfillment operations, transportation, freight forwarding, picking, and packing.

3PL focuses on the entire supply chain management operations, from the package pickup to the delivery of the products. The increasing trend of utilization of these services due to the emergence of distribution outsourcing drives market growth.

Every market has a certain degree of demand fluctuations, and the manufacturers need to cope with the fluctuations. Third-Party Logistics (3PL) services provide effective inventory management and product warehousing.

These solutions offered by these companies enable manufacturing companies to regulate their manufacturing operations without getting concerned about the proper storage of the manufactured products.

Third-Party Logistics also works to maintain a supply of the company’s products across the various regions in the market, which helps the company increase its product availability across the markets.

Third-Party Logistics offers distribution, shipping, and warehousing of the products of manufacturers. Significant improvement in the overall supply chain management is anticipated to bolster the use of Third Party Logistics during the forecast years.

Many companies wish to enter into untapped markets to improve their performance and sales footprints across multiple regions. Although, limitations such as the unavailability of established shipping and delivery solutions and the need for warehouse infrastructure and inventory storage restrict these companies from operating across multiple regions.

Third-party logistics provides the manufacturers with all these services and helps them improve their business in various potential regions.

The companies can increase their market penetration and product availability without making substantial investments in warehouse establishment and strengthening their distribution chain.

Thus, 3PL stands very useful for organizations trying to improve their global sales footprints. The tier 2 and tier 3 players are expected to contribute significantly as these companies do not possess a strong distribution channel and warehouse infrastructure outside their regional market. Third-party logistics services stand as the optimum solution for these companies to initiate operations in the potential regions.

Third-Party Logistics operators pick up the packages from the manufacturing facilities and initiate shipping and inventory management operations of these products as per the requirements of the products at different regions.

Although, manufacturers tend to lose control of the supply chain management of their products. The interactions of an unknown third-party supplier with the products of the company may restrict certain manufacturers from using third-party logistics services.

The manufacturer also faces difficulties in tracking the process of delivery, further reducing the hold and control on the in-transit shipments.

Additionally, during quality assurance and testing, companies usually identify anomalies and need to alter the manufactured products to eliminate the problems. The companies operating their own delivery process can perform this task efficiently, while the manufacturers operating with third-party logistics face difficulties.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Mode of Transport Typ |

Roadways Airways |

| By Industry Vertical Type |

Manufacturing Automotive |

| By Service Type |

Domestic Transportation Management (DTM) International Transportation Management (ITM) |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Roadways transport accounted for over 58.2% in 2023. Over the course of the forecast period, it is anticipated that the expansion of roadways will be driven by the emerging model of public-private partnerships as well as the increased emphasis on supply chain infrastructure.

Additionally, the expansion of the road transportation sector is being fueled by a number of initiatives undertaken by the government. It is anticipated that the recent regulations that were imposed by the Federal Motor Carrier Safety Administration and that permit the use of cameras as an alternative to rearview mirrors will be beneficial to truck drivers in terms of safety.

The airline segment is anticipated to emerge as the segment with the highest growth rate, expanding at a compound annual growth rate of 9.1% over the period of the forecast. Due to the recent outbreak of the coronavirus, there has been a restriction placed on the global air freight trade.

This has led to a significant decrease in the capacity of the air uplift, which has resulted in an increase in the rates charged by carriers.

A number of businesses, including CEVA Logistics, have initiated medical relief cargo charters for the purpose of delivering emergency supplies and equipment, including personal protective equipment (PPE) kits, facial masks, gloves, hand sanitizers, disposable gowns, respirators, ventilators, and other COVID-19 relief provisions.

The manufacturing sector held the largest revenue share of 24.8% in 2024. Manufacturing and logistics go hand in hand as the industry has a complex supply chain process. The manufacturing sector involves the procurement of raw materials and other parts from different resources across the regions.

The involvement of various suppliers and distributors makes the transport activity a tedious job. Thereby, the manufacturing sector is outsourcing transportation activities owing to the benefits offered in terms of reduced transportation cost, supply chain visibility, inventory and vendor management, business process development, and improved customer services.

The buoyant manufacturing sector in the U.S., Mexico, China, and India has witnessed an increase in outsourced transportation activities. The local manufacturing sector in India is growing with several tax reform policies and government initiatives such as ‘Made in the USA’ and ‘Make in India’ projects.

The automotive sector is expected to emerge as the fastest-growing segment expanding at a CAGR of 8.9% over the forecast period. Transportation and supply chain management is the backbone of the modern retail industry, playing a crucial role in same-day delivery and fulfillment capabilities.

E-retailing and dedicated transportation services have paved the way for medium scale companies to enter the third-party logistics market, thereby helping the retail companies to expand their operations and offerings in semi-urban areas.

Furthermore, 3PL offers flexibility to retail businesses to develop new Transports, enhance capabilities, and expand their regional presence.

The Domestic Transportation Management (DTM) segment held the largest market share of 32.4 % in 2024. DTM services are performed in conjunction with freight brokers, which deal with shipment origin to their destination.

The increasing trade movement among the unloading dock to a warehouse, escalating carrier rates, a surge in cross-docking services, and rising fuel surcharge are driving the growth of the DTM segment. The growing consumer demand in sectors such as retail, healthcare, and the steady GDP growth of various countries is further aiding the segment growth.

The continued growth in global economic activities and a rise in the e-commerce sector have led to an increase in demand for international transportation management services. Trade liberalization policies and cross-border transport activities have increased international trade, thereby propelling the segment growth.

Free Trade Agreements (FTAs) are driving the demand for international transportation. The African Continental Free Trade Area (AfCFTA) and Progressive Trans-Pacific Partnership (CPTPP) are the two recent examples of rising multilateral free-trade agreements.

Several bilateral free-trade agreements such as Costa Rica- South Korea FTA and Indonesia-Australia comprehensive economic partnership agreement are influencing the demand for international transportation services.

Asia-Pacific is expected to witness the highest growth rate in the 3PL market. China is anticipated to emerge as a significant contributor to the third-party logistics market in the Asia Pacific region. Robust export activities of the manufacturers operating in China are anticipated to drive the growth of the market in the region.

The use of third-party logistics for cross-border trade is anticipated to significantly contribute to the development of the market. The maritime transport development initiatives by the government of India are anticipated to boost market growth.

As per the government initiative, India is aiming to surplus the capacity of its 18 major ports by 25% to increase and augment maritime shipments. Similarly, the Vietnam government is taking decisive steps in making noteworthy developments in the marine transport network.

Europe is expected to witness substantial growth over the forecast period. The region’s largest retail and e-commerce industries are among the largest users of third-party logistics. In extremely competitive markets, such as the United Kingdom, delivery time is a crucial issue for shops and online stores.

Therefore, businesses outsource their logistics to delivery professionals, and both large and small stores can compete with next-day, on-demand delivery. The U.K. is one of the world’s leading trade nations, exporting the majority of its goods to numerous European nations.

Due to developed infrastructure, a sophisticated supply chain network, and the presence of global businesses, the freight and logistics market in the country has formed a solid foundation over the years.

The growth of the Latin American logistics market is propelled by an increase in technologically driven logistics services, a surge in the adoption of IoT-enabled linked devices, and the expansion of the e-commerce market.

However, the lack of necessary infrastructure, the high cost of logistics, and the lack of manufacturers’ control over logistics services restrict the market’s expansion.

The governments of the Middle Eastern countries are supporting the 3PL and logistics sector through a variety of initiatives, laws, and investment incentives to entice firms to invest in the country and provide customers with logistical services.

Additionally, e-commerce has emerged as a major market driver in the region. The number of e-commerce sales has increased; local vendors, merchants, wholesalers, and manufacturing units are focused on online channels to boost their sales.

The market is expected to grow CAGR of 9 % from 2025 to 2033.

The current market size is USD 1239.33 Billions in 2024.

North America currently holds the largest market shares.

Top 12 industry players in industry are H. Robinson Worldwide (CHRW) Inc., FedEx Corporation, Nippon Express Co., Ltd., BDP International, XPO LogisticsInc, DB Schenker Logistics, Burris Logistics, CEVA Logistics, Kuehne + Nagel International AG, DSV Panalpina A/S, Yusen Logistics Co. Ltd. (Nippon Yusen), UPS Supply Chain Solutions, Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Third Party Logistics (3PL) Market, By Mode of Transport Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Third Party Logistics (3PL) Market, By Industry Vertical Type

5.3 Third Party Logistics (3PL) Market, By Service Type

6.1 North America Third Party Logistics (3PL) Market , By Country

6.1.1 Third Party Logistics (3PL) Market, By Mode of Transport Type

6.1.2 Third Party Logistics (3PL) Market, By Industry Vertical Type

6.1.3 Third Party Logistics (3PL) Market, By Service Type

6.2 U.S.

6.2.1 Third Party Logistics (3PL) Market, By Mode of Transport Type

6.2.2 Third Party Logistics (3PL) Market, By Industry Vertical Type

6.2.3 Third Party Logistics (3PL) Market, By Service Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping