Tonometer Market

Tonometer Market Share & Trends Analysis Report, By Product Type (Applanation Tonometers, Indentation Tonometers, Rebound Tonometers, Non-contact Tonometers (Air Puff), Transpalpebral Tonometers, Dynamic Contour Tonometers) By End User (Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers (ASCs), Homecare Settings, Research Institutions) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

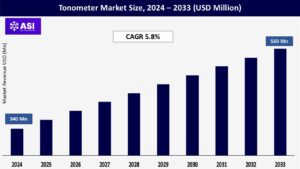

CAGR: 5.8%

Last Updated : September 30, 2025

The global Tonometer Market was valued at approximately USD 340 million in 2024 and is projected to reach USD 560 million by 2033, growing at a CAGR of 5.8% during the forecast period (2025–2033).

Tonometers are used in ophthalmic diagnostics to assess intraocular pressure (IOP), which helps to diagnose and treat glaucoma, one of the leading causes of irreversible blindness globally. Tonometry measures the resistance of the eye to indentation or flattening with different tonometer designs available: applanation, rebound, and non-contact (air puff). Tonometers have traditionally been used in hospitals and clinics, however, it is increasingly used for homecare purposes, enabling early diagnosis and follow-up. The market drives a global increase in glaucoma diagnosis and the growing awareness of ocular health consequences. The drive for greater portability and contactless tonometers is also reflected in the tonometer space. Furthermore, the aging population and access to ophthalmic care have also opened the door for growth in emerging economies.

The worldwide burden of glaucoma, as one of the top causes of irreversible blindness, is a major reason for the increase in the tonometer market. According to the World Health Organization (WHO) and International Agency for the Prevention of Blindness (IAPB), there are currently over 76 million people around the globe that have glaucoma and it is projected that in 2040 this number will rise to more than 110 million, particularly in areas with older populations.

Glaucoma is often called the “silent thief of sight,” as it can come on silently over time without any warning signs, and is only detectable through checks of the intraocular pressure (IOP), which is the major risk factor. Therefore, tonometers are used by ophthalmologists and optometrists for the early detection and ongoing management of the condition.

With the increase in awareness of ocular health, routine screening for eye conditions is moving towards becoming increasingly common, particularly for individuals older than 40 years of age. Many national health organizations are lobbying for mandatory glaucoma screening for high-risk populations. As an example, the American Academy of Ophthalmology suggests comprehensive eye exams every 1–2 years for individuals older than age 65 years.

With the increasing need for regular monitoring of IOP, more clinicians and patients are utilizing the conventional applanation tonometers and the more recent rebound tonometers (or non-contact tonometers). Likewise, the increasing prevalence of ocular disorders such as ocular hypertension and diabetes and diabetic retinopathy will continue leading to a higher demand for tonometry in clinical settings and home care settings.

Technological advances have completely altered the tonometry picture; we now have tonometers that are portable, non-invasive, user-friendly, and can send and receive data remotely. Due to these changes, tonometry has expanded beyond the clinic to home care, where they are particularly useful for patients requiring regular monitoring.

Manufacturers are now releasing next-generation tonometers with rebound technology, wireless capability, and integration with cloud-based services to propel patient-centric care and share data constantly with their healthcare providers. For example, in March 2024, Revenio Group released the Icare HOME2 tonometer, or self-tonometer, that allows patients with glaucoma to measure their intraocular pressure independently at home and securely transmit the results to their doctor through a digital data platform.

This is a clear indicator that we are moving toward decentralized ophthalmic care, with the intent of better, more precise and personalized treatment strategies. Companies like NIDEK and Keeler are also working on lightweight, handheld tonometers with automatic capture capabilities to decrease operator dependence and maximize efficiencies in both rural and urban communities.

This is also driven by the growing number of older adults. According to the United Nations, the geriatric population will increase from 1 billion in 2020 to 2.1 billion by 2050. As people age, their chance of developing glaucoma or other vision-impairing conditions increases, which will require future visits to healthcare professionals and potentially increase the global market size for tonometers.

Also, healthcare expenditure is rising sharply, especially in emerging economies such as India, China, and Brazil. These nations are not limited to the expansion of ophthalmic infrastructure (for example, certainly the procurement of diagnostic instruments), but also making significant investments to improve healthcare delivery and eventually, the overall health and wellness of their citizens. These countries are expected to fuel growth in the tonometers market.

One of the main challenges for the tonometer market is the high cost of advanced instruments resulting from the use of rebound technologies, digital transmission of data, and self-monitoring technologies. Classic forms of tonometry (applanation and indentation), are relatively inexpensive; however, the next generation of tonometry instruments (e.g. handheld, non-contact tonometers, and home-use rebound tonometers) can often be cost prohibitive for small clinics, independent optometrists, and patients, especially in low- and middle-income populations.

The cost prohibition for measuring intraocular pressure (IOP) is weighty. The costs for obtaining more advanced tonometers, such as non-contact tonometers and non-contact, self-monitoring tonometers, may be too high for low- and middle-income clinics offering government funded services.

There are limited opportunities for patients to seek reimbursement for diagnostic procedures, and in many developing countries there is limited access to specialized ophthalmic clinics capable of managing patients with elevated IOP. Limited access for an individual to receive a timely, accurate diagnosis of elevated IOP may have dire consequences, given the growing burden of glaucoma, and all ocular diseases in low- and middle-income populations.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Applanation Tonometers Indentation Tonometers Rebound Tonometers Non-contact Tonometers Transpalpebral Tonometers Dynamic Contour Tonometers |

| By End User |

Hospitals Ophthalmic Clinics Ambulatory Surgical Centers Homecare Settings Research Institutions |

| Key Players |

Revenio Group Corporation Haag-Streit Group NIDEK Co., Ltd. Topcon Corporation Keeler Ltd. Kowa Company, Ltd. Tomey Corporation Canon Medical Systems Corporation OCULUS Optikgeräte GmbH AMETEK, Inc. (Reichert Technologies) |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Tonometer Market is segmented by product type and end user. Each segment contributes uniquely to enhancing intraocular pressure (IOP) assessment, early detection of glaucoma, and broader ocular disease management.

In 2024, Applanation Tonometers had the major market share with 34.2%, due to their long clinical history and established precision in measuring intra-ocular pressure (IOP). Goldmann applanation tonometry is still the gold standard in eye care practices, especially in hospital and cosmetic practices. Its high adoption rate from eye care to community practices allows it to maintain this dominant status due to consistency in performance and adaptation with slit lamp systems.

Rebound Tonometers will have the fasted growth, as they are the newest type of tonometer which are portable, have a simple process to use, and are good for self-monitoring. For example, the Icare HOME2 allows patients to monitor their own eye pressure at home allowing for reflective, treatment or a remote patient management plan when needed.

Although it is a new segment in established markets (i.e., United States, Germany, etc.) and urban emerging market economies, it will quickly grow. Non-Contact Tonometers (Air-Puff) are emerging in sustained use in high volume screening environments such as the optometry chains and community health programs indiciating that there is longevity in increasing demand in this segment as well. The contactless nature increases comfort for patients, as well as decreasing risk of cross-contamination, the latter of which is especially relevant in a post-pandemic world.

These tonometers, in particular, are also preferable for pediatric and geriatric patients. Some tonometers such as Transpalpebral and Dynamic Contour Tonometers are currently niche and may experience increased clinical interest due to their accuracy in complex cases (i.e. post-corneal surgery patients). Should the technology be further validated and standardized, we may see greater popularity amongst the latter mentioned examples of tonometers.

The segment share of tonometers in the hospital market is very significant, amounting to 51.7% in 2024. Most patients in hospitals are persons who have some form of complicated ocular disease, and these facilities are likely capable of making multiple purchases or investing in different types of tonometry equipment. Tonometers are used frequently in emergency departments, ophthalmology departments, and preoperative evaluations.

Second only to hospitals are the ophthalmic clinics where the growing number of private eyecare centers and specialists office practices, further established in developed and developing countries is driving the growth in this segment. Clinics use a combination of manual and digital tonometers to diagnose and manage glaucoma, cataracts and other conditions in an outpatient setting.

Ambulatory Surgical Centers have a steady growth in performing ophthalmic procedures as procedural volume increases, specifically cataract surgery and glaucoma surgery. Tonometers are crucial in the preoperative assessment and recovery phases. Homecare Settings is a newly developing segment resulting from the increase of self-tonometry devices and greater recognition by glaucoma patients about the importance of daily IOP (intraocular pressure) assessments.

There is ongoing advocates for appropriate ease of use in handheld rebound tonometers, especially for aging and chronic ocular condition populations. Research and Academic Institutes use tonometers at various levels of technology for their additional ophthalmic research and clinical trials, including but not limited to those investigating potential treatments for ocular hypertension and the progression of glaucoma.

The North American region accounted for the largest market share of 38.5% in 2024. This is attributed to the existing and expected availability and adoption of new diagnostic devices and testing methods, alongside strong healthcare infrastructure, as well as high awareness of glaucoma and other eye illnesses. The United States currently drives the majority of growth in the regional market, particularly because both private and public healthcare systems in the country have opened access to tonometry.

There is also a growing interest in home-use tonometers, largely through the elderly glaucoma patient population, as well as patients lacking mobility. In addition to the US market, the region as a whole, is also seeing the effects of reimbursement policies, in addition to key market untapped players such as Revenio Group, Topcon Corporation, and Haag-Streit.

Europe should be noted as a major part of the tonometer market, fueled by a rise in the prevalence of glaucoma and other chronic eye diseases (especially in an aging population), and countries such as Germany, France, the UK, Italy, and Netherlands have well-inserted the available ophthalmology services provided through hospitals and outpatient clinics.

The European Glaucoma Society estimates that up to 10 million people in Europe suffer from glaucoma and many do not yet know that they have it. Sources of demand are national eyecare initiatives and diagnosis, as seen in Sweden and Austria where national eye health screening and early diagnosis and recommended follow-up are more frequent and urgent.

Reliable tonometry devices are also being requested as a result of more investment in health technology or support from government/opposer institutions looking for alternatives to amateur tonometry. There are indicators for continued growth in the tonometer market across Europe.

The Asia-Pacific region is expected to grow at the highest rate, registering a compound annual growth rate (CAGR) of 7.9% over the forecast period (2025–2033) propelled by rapid urbanization, increasing access to healthcare, and the increase in geriatric population in China, India, and Japan. The Asia Pacific Glaucoma Society (APGS) has noted a rising number of undiagnosed glaucoma cases in the region which has created demand for the purchase of affordable and portable tonometers.

In addition, government initiatives to improve on ophthalmic infrastructure like India’s National Programme for Control of Blindness and China’s increased commitment to community eye health, are bringing tonometers into urban and rural clinics. The new portable rebound tonometers and handheld tonometers affording high-quality measurements are becoming even more appealing because of their affordability compared to other tonometers available on the market in resource-limited settings.

Latin America and the Middle East & Africa (MEA) regions experience moderate growth thanks to slow enhancements in healthcare management and increasing endeavors to alleviate preventable blindness. Eye care knowledge is increasing in countries such as Brazil, Mexico, South Africa, and UAE due to investments coming from both the public and private sector.

There are still obstacles such as disparities in economic status and access to ophthalmic specialists as well as limited penetration of advanced diagnostic equipment which slows down progress adoption. International NGOs and health partnerships are making in-roads to increase access to affordable tonometry services specifically in underserved communities and remote communities globally.

The market was valued at USD 340 million in 2024.

The market is projected to grow at a CAGR of 5.8% from 2025 to 2033.

Applanation Tonometry hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Revenio Group Corporation, Haag-Streit Group and NIDEK Co., Ltd.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 The Tonometer Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 The Tonometer Market, By End User

6.1 North America The Tonometer Market, By Country

6.1.1 The Tonometer Market, By Product Type

6.1.2 The Tonometer Market, By End User

6.2 U.S.

6.2.1 The Tonometer Market, By Product Type

6.2.2 The Tonometer Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping