Train Control and Management System Market

Train control and Management system Market Share & Trends Analysis Report, By Train Type (Metros & High Speed Trains, Light Rails & Trams, Freight Trains), Solution (Communication base train control, Integrated trin control,), By Component ( Vehicle control unit, Human machine interface, Mobile communication), By connectivity (Wired, Wireless), By sales channel (OEM, Aftermarket) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

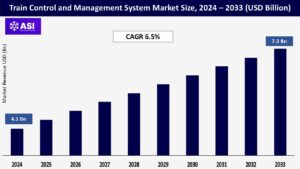

CAGR: 6.5%

Last Updated : June 25, 2026

The global Train Control and Management System Market size was valued at approximately USD 4.1 billion in 2024 and is projected to reach USD 7.3 billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.5% during the forecast period 2025–2033.

TCMC plays an important role in increasing train safety, operational continuity, and paseenger comfort. The system integrates vehicle control, data communications, monitoring, and diagnostics. Increasing investments in railway infrastructures, smart mobility, and the need for automated and efficient rail transport are driving market growth.

Rapid urban growth and traffic congetion are pushing governments to invest in metro and high speed trian systems, increasing the assumptions of TCMS to manage and control operations efficiently.

The integration of 5G, AI, and IoT in TCMS is increasing real time data processing, fault diagnostics, and predictive maintenance, improving safety and reducing operational downtimes.

Infrastructure development programs, specially in Asia and Europe, are incorporating intelligent rail systems and automation, boosting demand for TCMS solutions.

TCMS implementation requires significant capital, particularly for legacy system upgrades, which can deter small and regional rail operators.

The increasing connectivity and data reliance in TCMS expose rail systems to potential cyber threats, necessitating robust measures.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Fuel Type |

Gasoline-Powered Diesel-Powered Electric & Hybrid |

| By End User Type |

Individual Consumer Rental Companies Corporate/Commercial |

| By Sales Type |

OEMs [ Original Equipment Manufacturers ] Aftermark/Conversions |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The gasoline segment is projected to hold a significant share of the market during the forecast period. The Gasoline engines tend to be quiet and smooth, providing a comfortable driving experience. Gasoline is cheaper and more readily available than diesel, making it a convenient option for many consumers.

Lastly, advancements in technology are improving the performance and efficiency of gasoline engines, making them an increasingly attractive option for class B motorhomes. The diesel segment held the largest market share in 2024. The segment growth is attributed to the inherent advantages of diesel engines.

Diesel motorhomes typically offer high fuel efficiency, which is a significant consideration for consumers given the size and weight of these vehicles. These factors contribute to the preference for diesel motorhomes among a large segment of consumers.

Electric motorhomes represent a growing segment of the market, driven by increasing environmental awareness and advancements in battery technology. These models offer zero emissions and lower operating costs, making them an attractive option for eco-conscious consumers.

As governments around the world implement stricter emissions regulations and offer incentives for electric vehicles, the adoption of electric motorhomes is expected to accelerate.

Manufacturers are investing in research and development to improve the range and charging infrastructure of electric motorhomes, addressing some of the current limitations and expanding their appeal to a broader audience.

Individual consumer demand for Class B motorhomes has led to growth in the direct owners segment. These vehicles provide a convenient and comfortable way for individuals and families to explore the great outdoors while also providing amenities such as sleeping accommodations, kitchens, and bathrooms.

Modern Class B motorhomes offer a diverse range of facilities and features, such as slide-outs, convertible furniture, and innovative storage solutions, making them an appealing option for direct owners looking for a more spacious and comfortable living experience while traveling.

Rental companies offer Class B motorhomes to customers seeking short-term travel solutions without the commitment of ownership. This segment appeals to a wide range of consumers, including tourists, holidaymakers, and adventure enthusiasts.

Fleet owners benefit from the high demand for rental motorhomes, driving business growth and expanding their market presence. The growing interest in motorhome rentals is also supported by the convenience and flexibility they offer. Customers can choose from a variety of motorhome models, catering to different preferences and budgets.

Commercial motor homes, on the other hand, include vehicles used for business purposes, such as mobile offices, food trucks, or rental services. The commercial segment is gaining traction as businesses recognize the potential of mobile solutions in enhancing flexibility and reaching wider customer bases.

Motor homes offer unique opportunities for businesses to expand their operations and engage with customers in diverse locations. The growing popularity of remote work and flexible business models is fueling the demand for commercial motor homes, as companies seek innovative ways to adapt to changing market dynamics and consumer preferences.

OEM [Original Equipment Manufacturer] sales involve the direct sale of motor homes by manufacturers to consumers or distributors, typically through dealerships or direct sales channels. The OEM segment is a dominant force in the market, as it ensures the availability of the latest models and technologies directly from the manufacturer.

Consumers prefer OEM channels for their reliability, warranty coverage, and access to the latest features and innovations. The strength of the OEM segment is supported by the extensive dealership networks and marketing efforts by manufacturers to promote their brands and products.

Aftermarket sales, on the other hand, involve the sale of motor homes that are previously owned or refurbished, as well as the sale of parts and accessories. The aftermarket segment is growing as consumers seek cost-effective options or wish to customize and upgrade their existing motor homes.

The availability of a wide range of aftermarket parts and accessories allows consumers to enhance their vehicles according to personal preferences, whether it’s improving comfort, functionality, or aesthetics.

The aftermarket segment is particularly appealing to budget-conscious consumers and those looking to personalize their vehicles without the premium costs associated with new models.

The Asia-Pacific Motor Home Market is expected to register a CAGR of greater than 9% during the forecast period. Asia-Pacific is witnessing increasing demand for adventure camping as the number of camping grounds is increasing and along with that supportive plans from governments is expected to support the growth of the motorhome market during the forecast period.

The Europe Motor Home Market size is estimated at USD 11.76 billion 27% in 2025. The increase in travel activities and the cost benefits offered over other modes of travel are encouraging people to purchase recreational vehicles such as motorhomes.

The ability of a motorhome to be customized at ease is propelling technological advancements in the market rapidly. Additional factors driving this growth include an aging population, increased interest in outdoor activities, and a desire for more sustainable and eco-friendly travel options.

North America is the most significant 50% market shareholder globally for Class B motorhomes and is expected to expand substantially during the forecast period. This region’s dominance, led by the United States, stems from a well-established RV culture, favorable economic conditions, and a strong affinity for outdoor recreational activities.

Several factors contribute to the popularity of Class B motorhomes in North America. Their compact size, fuel efficiency, and versatility make them ideal for urban exploration, camping in congested areas, and long-distance travel. The region’s well-developed road infrastructure and extensive network of campgrounds and RV parks further support market growth.

MEA is acquired the 4.2 % of the global market shares in 2024. The market is expected to grow at a CAGR of 6.1% from 2025 to 2033. In MEA region Rental Services are the most affecting factors for developing the global market postitions.

Infrastructure limitations such as a lack of campgrounds and service facilities continue to constrain market expansion. Climate-adapted designs and off-road capabilities are crucial features in regional offerings..

The current market size is USD 4.1 Billions in 2024.

The market is expected to grow at a CAGR 6.5% during the forecast period from 2025 to 2033.

North America currently holds the largest market shares, driven by adoption across sectors such as finance, healthcare, and logistics.

High upfront costs, limited living space, and growing fuel costs for traditional models.

Winnebago, Thor Industries, airstream, Roadtrek, Pleasure-Way.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Train Control and Management System Market, By Fuel Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Train Control and Management System Market, By End User Type

5.3 Train Control and Management System Market, By Sales Type

6.1 North America Train Control and Management System Market , By Country

6.1.1 Train Control and Management System Market, By Fuel Type

6.1.2 Train Control and Management System Market, By End User Type

6.1.3 Train Control and Management System Market, By Sales Type

6.2 U.S.

6.2.1 Train Control and Management System Market, By Fuel Type

6.2.2 Train Control and Management System Market, By End User Type

6.2.3 Train Control and Management System Market, By Sales Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping