Ultrasound Devices Market

Ultrasound Devices Market Share & Trends Analysis Report By Technology (Diagnostic Ultrasound, Therapeutic Ultrasound) By Application (Radiology/General Imaging, Cardiology, Obstetrics/Gynecology, Urology, Musculoskeletal, Others (Anesthesiology, Emergency Medicine, etc.) By End User (Hospitals, Diagnostic Centers, Ambulatory Surgical Centers, Maternity Centers, Research & Academic Institutes)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

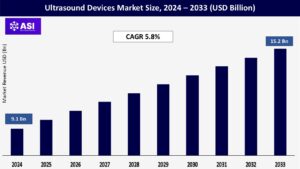

CAGR: 5.8%

Last Updated : October 31, 2025

The global Ultrasound Devices Market size was valued at approximately USD 9.1 billion in 2024 and is projected to reach USD 15.2 billion by 2033, growing at a CAGR of 5.8% during the forecast period (2025–2033).

Ultrasound devices use high-frequency sound waves to capture real-time images of other organs, tissues, and blood flow. Ultrasound is a non-invasive diagnostic modality used in many specialties including radiology, obstetrics and gynecology, cardiology, emergency medicine, etc. Ultrasound technology is also utilized for numerous therapeutic applications including tissue ablation and targeted drug delivery.

Compact or handheld devices, point-of-care imaging and integrating AI with ultrasound systems are some major driving forces to the growth of the market. Other growth drivers include the aging population, an increase in the prevalence of chronic diseases and expanding access to healthcare in emerging economies.

The continuous development in point-of-care ultrasound and mobile ultrasound devices is one of the major catalysts of the overall ultrasound devices market growth. Pocus allows clinicians to perform diagnostic imaging right at the bedside or in an emergency setting – which shortens diagnostic time and can improve patient outcomes, particularly in major trauma, rural areas, and critical care. A 2023 study published in BMJ Open revealed that the use of Pocus greatly increases accuracy of diagnosis and decision making in emergency medicine and low-resource settings.

In addition, as outpatient care increases, and as people increasingly prefer care at home or in an ambulatory setting, health care systems must procure small and portable devices, such as handheld ultrasound systems. For example, GE HealthCare’s Vscan Air – a wireless, pocket-sized ultrasound system – was launched in 2022, and allows healthcare providers to scan and diagnose patients from virtually any location. Similar to GE, Philips Lumify has successfully branded itself as a portable option based on an app for real-time imaging. The ease and efficiency of these portable imaging devices has driven their acceptance among anesthesiologists, emergency medical technicians, and primary care doctors for quick non-invasive imaging, and portability is a significant growth driver in the ultrasound devices market.

The field of ultrasound diagnostics is undergoing rapid and continual technological innovation specifically advancements in image clarity, automation, and artificial intelligence (AI). Modern ultrasound machines are utilizing AI-enabled image generation and analysis, automated measure, and higher quality images in 3D/4D that allow for greater accuracy and less variability of the operator. For example, in 2024 Siemens Healthineers introduced the ACUSON Maple ultrasound machine embedded with AI for general imaging, OB/GYN imaging, workflows, automated measures and enhanced image quality. Similarly, Canon Medical introduced AI-based liver analysis for images of the liver and utilization of machine learning algorithms in 2023 for reports with real-time fibrosis and steatosis. These advances can help identify chronic conditions like liver fibrosis, cardiovascular abnormalities, and cancers.

Other similarly situated advances are improving the ability for real-time elastography and contrast-enhanced ultrasound (CEUS) and the ability to identify lesions and obtain biopsies, therefore increasing the uses of ultrasound in oncology and interventionally. However, the uses for AI-derived technology is significantly broader than for ultrasound, which will improve efficiency but also the availability and scalability of machines for use in varied clinics, settings or environments.

The high cost of advanced ultrasound systems, especially with AI, 3D/4D imaging and elastography are one of the major barriers limiting ultrasound devices market growth. While basic 2D ultrasound machines are generally affordable, high-end models (primarily used for cardiology, oncology, and prenatal) can easily cost USD 70,000 to USD 200,000 depending on features and imaging options. For smaller and mid-sized hospitals and clinics, the prices for these top-of-the-line systems may exceed limited capital budgets, especially in emerging economies. Even in societies with established healthcare systems, reimbursement policies for ultrasound procedures are limited or inconsistent in parts of the world which discourages healthcare providers from investing in high-cost systems.

For example, the United States Medicare only reimburses certain types of diagnostic ultrasound scans in part, unless the procedure is deemed medically necessary thus putting uncertainty on return on investment. In some developing areas, countries like India or Brazil, most procedures that include some form of ultrasound in the diagnostic process are out of pocket expenses for patients, which further limits opportunities and impact of ultrasound in public healthcare systems. These financial barriers impeded market penetration, particularly in rural areas and underserved populations.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Diagnostic Ultrasound Therapeutic Ultrasound |

| By Application |

Radiology/General Imaging Cardiology, Obstetrics/Gynecology Urology Musculoskeletal Others (Anesthesiology, Emergency Medicine, etc.) |

| By End User |

Hospitals Diagnostic Centers Ambulatory Surgical Centers Maternity Centers Research & Academic Institutes |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Ultrasound Devices Market share is segmented by technology, application, end user. Each segment contributes significantly to improving diagnostic capabilities, treatment precision, and accessibility across healthcare settings.

In 2024, Diagnostic Ultrasound accounted for over 72.4% of the global market share, as ultrasound is utilized in a range of specialties, including cardiology, obstetrics, urology and general imaging. 2D ultrasound is still the major type of diagnostic imaging used universally; it offers affordability and reliability for routine scans. The 3D & 4D ultrasound segment has an upswing in adoption rates and rapidly growing growth prospects as these modalities are used frequently in obstetrics and oncology for the shared goal of anatomical visualization.

For obstetricians, anatomical visualization is essential for fetal monitoring while oncologists use anatomical visualization for tumor detection. Therapeutically, ultrasound, specifically High-intensity Focused Ultrasound, (HIFU) is being researched more frequently in the realm of cancer treatment and pain management. HIFU devices are being used with increasing frequency in treating uterine fibroids and prostate cancers. The ESWL segment has importance in urology for treating kidney stones with non-invasive means.

The Radiology/General Imaging segment is the biggest contributor at approximately 34.7% of the ultrasound devices industry in 2024 due to the general use of ultrasound in abdominal, liver, and kidney imaging. The Obstetrics/Gynecology segment follows closely with the expansion of routine fetal prenatal screenings and the rising global awareness of the importance of maternal care. Cardiology ultrasound is another large area of growth. The potential for growth in echocardiography is also supported by the increasing prevalence of cardiovascular diseases. Musculoskeletal ultrasound is gaining traction among sports medicine doctors and orthopedists assessing soft tissue and joint status.

Hospitals will account for a whopping 58.6% of the ultrasound devices market in 2024, due in part to the institutional infrastructure and expertise to perform diagnostic and therapeutic procedures. Diagnostic Centers are increasingly popular given the drivers for decentralizing imaging services for patient convenience and cost-effectiveness. Ambulatory Surgical Centers (ASCs) also present a growth area for ultrasound, particularly with pain management procedures and anesthesiology. Maternity Centers will support the increasing demand for OB/GYN ultrasound machines. Research & Academic Institutes will leverage advanced ultrasound systems used for clinical and exploratory studies, for training AI models, and in medical education.

North America has a high market share for ultrasound procedures (38.2% in 2024), because of the advanced healthcare infrastructure, speed of technology adoption, and increased levels of physician preference for noninvasive means of diagnosis. The United States is the higher contributor to revenue, because of the significant prevalence of ultrasound in multiple specialties (e.g., cardiology, obstetrics, emergency medicine, and musculoskeletal medicine).

The expected adoption of ultrasound products with AI integrated systems, along with the growth of point-of-care ultrasound (PoCUS) devices, is expected to contribute to overall Ultrasound Devices market growth. The high levels of reimbursement for ultrasound procedures and the presence of global leaders like GE HealthCare and Philips North America further support regional strength.

Europe continues to be an important market, lead specifically through countries like Germany, France, the UK, and Netherlands whose healthcare systems provide access to diagnostic imaging services across populations. From Eurostat data in 2022, there were more than 900,000 prenatal ultrasound procedures performed across EU countries, which illustrates a reliance on ultrasound for obstetric care.

The rising demand in Europe is attributed to the growing aging population, rising chronic disease burden, and an increase in use of 3D/4D and Doppler imaging technology. Continued governmental funding into the modernization of diagnostic imaging, especially in Eastern Europe and Nordics, will help encourage the adoption of this technology as it is incorporated in diagnostic policy.

The Asia-Pacific area is expected to achieve the highest growth of any region, with a CAGR of 7.9% from 2025 -2033, driven by increased healthcare spending, a greater awareness of the advantages of early disease detection, and the demand for either portable or low-cost ultrasound systems.

China, India, and Japan are leading market players, underwritten by public health initiatives and improving access to healthcare in urban and rural areas. For example, India’s National Health Mission and China’s Healthy China 2030 plan plan are large-scale initiatives to introduce diagnostic tools like ultrasound into the primary care setting. The increased rate of technological adoption and local manufacturing, primarily in China, also allows for lower costs-per-unit from vendors in many instances.

Latin America and Middle East & Africa (MEA) regions are also steadily growing given improving maternal health services, increasing private healthcare providers, and international aid programs. Countries like Brazil, Mexico, South Africa, and the UAE investment diagnostics infrastructure for both the public and private sector, with increasing need for lower-cost ultrasound devices to bring to examination and screening programs in health centers and community programs.

However, significant barriers to full-scale adoption remain, including economic disparities, lack of reimbursement framework, and lack of trained sonographers. Despite these challenges, mobile and handheld ultrasound examinations are developing in remote and underserved areas.

The ultrasound devices market was valued at USD 9.1 billion in 2024.

The ultrasound devices market is projected to grow at a CAGR of 5.8% from 2025 to 2033.

The diagnostic ultrasound hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

The ultrasound devices market major players include Philips Healthcare, Siemens Healthineers and Canon Medical Systems.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Ultrasound Devices Market, By Component

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Ultrasound Devices Market, By Technology

5.3 Ultrasound Devices Market, By Application

5.4 Ultrasound Devices Market, By End User

6.1 North America Mine Ventilation Market , By Country

6.1.1 Ultrasound Devices Market, By Technology

6.1.2 Ultrasound Devices Market, By Application

6.1.3 Ultrasound Devices Market, By End Use

6.2 U.S.

6.2.1 Ultrasound Devices Market, By Technology

6.2.2 Ultrasound Devices Market, By Application

6.2.3 Ultrasound Devices Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping