Vacuum Cleaner Market

Vacuum Cleaner Market Share & Trends Analysis Report, By Product Type (Upright, Canister, Robotic, Handheld, Stick, Wet/Dry), By Technology (Cordless, Corded), By Mode of Operation (Manual, Automatic/Smart), By End-Use (Residential, Commercial, Industrial) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

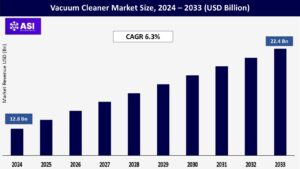

CAGR: 6.3%

Last Updated : July 1, 2026

The global Vacuum Cleaner Market size was valued at approximately USD 12.8 billion in 2024 and is projected to reach USD 22.4 billion by 2033, growing at a CAGR of 6.3% during the forecast period (2025–2033).

Vacuum cleaners are household and industrial cleaning devices that use suction to remove dust, dirt, and debris from floors, upholstery, draperies, and other surfaces. They are available in a wide range of designs and technologies—from traditional upright and canister models to robotic and cordless variants—catering to residential, commercial, and industrial needs.

Modern vacuum cleaners integrate advanced filtration systems (such as HEPA filters), smart navigation, IoT connectivity, and energy-efficient motors, enhancing both convenience and cleaning efficiency.

One of the most prominent drivers in the vacuum cleaner market is the shift toward automation. Robotic vacuum cleaners, equipped with sensors, AI-based mapping, and app-controlled features, have transformed the cleaning process for households and small commercial spaces.

The growing penetration of IoT and smart home ecosystems enables these devices to be integrated with virtual assistants such as Amazon Alexa and Google Assistant, making them more user-friendly.

Consumers are increasingly seeking devices that save time, reduce physical effort, and maintain high cleanliness standards. This demand is amplified by busy urban lifestyles, the increasing prevalence of dual-income households, and growing awareness of hygiene and dust-related allergies.

Post-pandemic hygiene consciousness has significantly impacted consumer behavior. Vacuum cleaners with advanced HEPA filtration systems can capture microscopic allergens, bacteria, and viruses, which is particularly appealing to consumers with respiratory issues or households with children and pets.

The rise in dust and pollution levels in urban areas, along with an increase in pet ownership, has further accelerated demand for efficient cleaning solutions. As governments and health organizations highlight the importance of clean indoor environments, households and commercial establishments are investing more in modern cleaning appliances.

While demand for smart and feature-rich vacuum cleaners is growing, their higher price points can be a barrier for mass adoption, especially in emerging markets. Robotic vacuum cleaners and premium cordless models with advanced sensors, powerful suction, and long battery life can cost significantly more than traditional models.

For price-sensitive consumers, this limits purchasing decisions, even when they recognize the convenience and hygiene benefits. Additionally, maintenance costs—such as filter replacements, battery changes, and servicing—add to the total cost of ownership. Manufacturers must balance innovation with affordability to achieve broader market penetration.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Upright Canister Robotic Handheld Stick Wet/Dry |

| By Technology |

Cordless Corded |

| By Mode of Operation |

Manual Automatic/Smart |

| By End-Use |

Residential Commercial Industrial |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Vacuum Cleaner Market is segmented by By Product Type (Upright, Canister, Robotic, Handheld, Stick, Wet/Dry), By Technology (Cordless, Corded), By Mode of Operation (Manual, Automatic/Smart), By End-Use (Residential, Commercial, Industrial)

Upright Vacuum Cleaners: Popular in North America and Europe, upright models offer powerful suction, wide cleaning paths, and ease of use for carpeted floors. Canister Vacuum Cleaners: Favored for versatility and maneuverability, canister models are suitable for cleaning hard floors, stairs, and upholstery.

Robotic Vacuum Cleaners: The fastest-growing category, robotic vacuums are equipped with AI navigation, scheduled cleaning, and obstacle detection. Handheld Vacuum Cleaners: Compact and lightweight, handheld vacuums are ideal for quick clean-ups, cars, and tight spaces.

Stick Vacuum Cleaners: Cordless stick vacuums have surged in popularity due to their portability and convenience, especially in apartments. Wet/Dry Vacuum Cleaners: Used for both liquid and dry debris, these models are common in industrial and garage applications.

Cordless Vacuum Cleaners: Growing rapidly due to improved battery performance, portability, and convenience. Corded Vacuum Cleaners: Still dominate in high-suction applications, especially in commercial and industrial settings.

Manual Vacuum Cleaners: Traditional models requiring physical operation remain common in price-sensitive markets. Automatic/Smart Vacuum Cleaners: These are gaining popularity in urban households and tech-savvy regions.

Residential: The largest segment, driven by rising disposable incomes and changing lifestyle preferences. Commercial: Includes hotels, offices, and retail spaces where cleanliness is essential for customer experience. Industrial: Heavy-duty vacuums used in factories, warehouses, and construction sites for safety and efficiency.

North America remains a dominant region in the vacuum cleaner market, fueled by high household appliance penetration, strong purchasing power, and a preference for premium cleaning solutions. The U.S. is the largest contributor, with a high adoption rate of upright and robotic vacuum cleaners.

Smart home integration is a major driver here, with many consumers choosing devices compatible with IoT platforms. Pet ownership is high in this region, which boosts demand for vacuum cleaners with specialized pet-hair removal features.

Additionally, robust retail channels—both online and offline—enable easy accessibility to the latest products. Canada follows similar trends but exhibits stronger demand for canister models, driven by its mix of carpeted and hard flooring in households.

Europe represents a mature yet evolving market, characterized by a strong preference for energy-efficient and eco-friendly appliances. Western Europe—particularly the UK, Germany, France, and the Nordic countries—sees high adoption of canister and cordless stick vacuum cleaners.

EU regulations encouraging sustainable appliance manufacturing have led to innovations in energy-saving motors and recyclable materials. Germany leads in technological adoption, with a growing robotic vacuum cleaner market, while the UK has seen rapid uptake of cordless stick vacuums due to compact urban living spaces.

Southern and Eastern Europe are gradually increasing their adoption rates as disposable incomes rise and retail infrastructure expands.

Asia-Pacific is the fastest-growing region, with China, Japan, South Korea, and India driving most of the demand. China is a global manufacturing hub for vacuum cleaners, producing for both domestic use and export.

Rapid urbanization, growing middle-class populations, and increasing hygiene awareness are key growth factors. Japan and South Korea lead in robotic vacuum adoption, with domestic brands launching AI-powered models that appeal to tech-savvy consumers.

India’s market is in an early growth stage, with rising demand for affordable yet efficient models, particularly cordless stick and handheld vacuums. Increasing e-commerce penetration and localized product offerings are boosting regional sales.

Latin America is experiencing steady growth, with Brazil, Mexico, and Argentina as primary markets. Urban migration and growing disposable incomes are increasing demand for modern cleaning appliances.

However, economic instability and price sensitivity influence consumer choices, leading to higher sales of mid-range models over premium robotic units. Retail partnerships, installment payment schemes, and targeted marketing are helping brands expand their footprint.

MEA is an emerging market for vacuum cleaners, led by countries like Saudi Arabia, UAE, and South Africa. The region’s growing hospitality and retail sectors, coupled with increasing household appliance adoption, support market expansion.

Robotic vacuum cleaners are gaining traction among high-income households, while traditional canister and wet/dry models remain common in commercial and industrial settings. Infrastructure development and an expanding middle class are likely to support long-term market growth, although limited product availability in rural areas remains a challenge.

The market was valued at approximately USD 12.8 billion in 2024.

It is projected to grow at a CAGR of 6.3% from 2025 to 2033.

Upright and canister vacuum cleaners hold significant shares, but robotic vacuums are the fastest-growing segment.

Asia-Pacific is expected to witness the highest growth due to urbanization, rising incomes, and increasing hygiene awareness.

Major players include Dyson, Electrolux, Miele, iRobot, Samsung, and LG Electronics.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Vacuum Cleaner Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Vacuum Cleaner Market, By Technology

5.3 Vacuum Cleaner Market, By Mode of Operation

5.4 Vacuum Cleaner Market, By End-Use

6.1 North America Vacuum Cleaner Market , By Country

6.1.1 Vacuum Cleaner Market, By Product Type

6.1.2 Vacuum Cleaner Market, By Technology

6.1.3 Vacuum Cleaner Market, By Mode of Operation

6.1.4 Vacuum Cleaner Market, By End-Use

6.2 U.S.

6.2.1 Vacuum Cleaner Market, By Product Type

6.2.2 Vacuum Cleaner Market, By Technology

6.2.3 Vacuum Cleaner Market, By Mode of Operation

6.2.4 Vacuum Cleaner Market, By End-Use

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping