Vapor Recovery Unit Market

Vapor Recovery Unit (VRU) Market Size, Market Share & Trends Analysis Report, By Product Type (Conventional VRUs, Rotary Screw VRUs, Liquid Ring VRUs), By Application (Oil and Gas, Chemical Processing, Pharmaceuticals, Food and Beverage, Others), By Region (North America, Europe, APAC, Middle East and Africa, LATAM) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2032

Report Code : ASIEPR1011

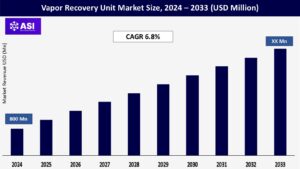

CAGR: 6.8%

Last Updated : July 2, 2026

The global Vapor Recovery Unit Market size was valued at approximately USD 800 Million in 2024 and is projected to reach USD XX Million by 2033, growing at a CAGR of 6.8% during the forecast period (2026–2033).

VRUs are critical for reducing hydrocarbon emissions and recovering valuable vapors across various industries. These units are witnessing increased adoption due to stringent environmental regulations, rising awareness about emission control, and advancements in recovery technologies.

Key growth drivers include the increasing implementation of emission regulations by governments worldwide, growing energy demand, and technological innovations in VRU designs, enhancing operational efficiency and cost-effectiveness.

The imposition of strict environmental regulations by governments globally is a primary driver of the vapor recovery unit market. Regulatory bodies like the U.S. Environmental Protection Agency (EPA) and the European Union have mandated emission standards for volatile organic compounds (VOCs) and greenhouse gases. VRUs play a pivotal role in helping industries comply with these regulations by recovering vapors from storage tanks, pipelines, and other equipment.

For instance, the EPA’s New Source Performance Standards (NSPS) require VOC recovery in oil and gas operations, creating a significant demand for advanced VRUs. Similarly, the European Commission’s Industrial Emissions Directive emphasizes vapor recovery in chemical and refining industries.

In emerging economies, governments are also introducing policies to curb industrial emissions, which is supporting growth in the vapor recovery unit market size, particularly in the petrochemical and transportation sectors. India’s National Clean Air Program (NCAP) and China’s Blue Sky Initiative have bolstered the adoption of VRUs, particularly in the petrochemical and transportation sectors.

The vapor recovery unit market is being propelled by advancements in technology, including the development of rotary screw and liquid ring VRUs. These systems are designed to improve operational efficiency, reduce energy consumption, and achieve higher vapor recovery rates, supporting the growth of the vapor recovery unit market size by addressing the increasing demand for cost-effective and environmentally compliant solutions.

According to a 2023 report by the International Energy Agency (IEA), advanced VRUs can improve vapor recovery efficiency by up to 95%, significantly reducing greenhouse gas emissions and product loss in industries such as oil and gas, chemical processing, and food production.

Rotary screw VRUs are particularly favored for their ability to manage varying pressure levels and flow rates, making them ideal for upstream oilfield operations and bulk storage facilities. On the other hand, liquid ring VRUs, valued for their durability in handling moisture-laden or contaminated gas streams, have found increasing applications in petrochemical plants and refineries.

A recent study revealed that liquid ring VRUs have reduced maintenance costs by 20% over traditional systems, highlighting their operational advantages.

The integration of IoT (Internet of Things) and AI (Artificial Intelligence) technologies into vapor recovery unit systems is another transformative factor driving vapor recovery unit market growth. Smart VRUs equipped with real-time monitoring systems and predictive maintenance features are gaining traction.

These advanced systems provide real-time tracking of key performance indicators such as pressure, temperature, and flow rates, enabling predictive analytics to identify potential equipment failures. For instance, AI-driven diagnostics can reduce downtime by up to 30%, as reported by a 2024 study from the U.S. Department of Energy.

In the chemical sector, where compliance with strict environmental regulations is essential, the adoption of smart vapor recovery unit ensures consistent performance and emission reductions.

In the food processing industry, where product quality and safety are paramount, these systems minimize VOC (volatile organic compound) emissions while ensuring operational efficiency.

The combination of mechanical innovations and digital technology integration is revolutionizing the vapor recovery unit market, positioning these systems as essential tools for industries aiming to balance productivity, cost-effectiveness, and environmental stewardship.

Despite their long-term benefits, vapor recovery unit involve significant upfront costs, including design, installation, and maintenance expenses. These costs can be prohibitive for small and medium-sized enterprises (SMEs), particularly in developing regions where financial resources are limited. Additionally, the need for skilled personnel to operate and maintain VRUs adds to the cost burden, hindering adoption.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Conventional VRUs Rotary Screw VRUs Liquid Ring VRUs |

| By Application |

Oil and Gas Chemical Processing Pharmaceuticals Food and Beverage Others |

| Key Players |

Zeeco, Inc. Flogistix John Zink Hamworthy Combustion Vapor Point LLC PSG Dover AEREON Cimarron Energy, Inc. Koch Industries, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Conventional vapor recovery unit accounted for 37.2% of the global market share in 2024, driven by their reliability, cost-effectiveness, and established applications in the oil and gas sector. These units are particularly effective in stabilizing operations at wellheads, refineries, and storage facilities, ensuring compliance with emission standards.

Rotary screw VRUs are gaining momentum, particularly in upstream oil and gas applications. These units offer superior performance by handling varying pressure and flow conditions, making them suitable for challenging environments like shale gas fields and offshore platforms.

With recovery rates exceeding 90% and energy consumption reduced by up to 20% compared to conventional systems, rotary screw VRUs are becoming indispensable in high-demand applications.

Ideal for high-capacity and multiphase recovery processes, liquid ring VRUs are increasingly adopted in the chemical and pharmaceutical sectors. These systems excel in managing vapors containing moisture or other impurities, ensuring consistent recovery efficiency and minimal downtime.

The oil and gas sector dominates the vapor recovery unit market with a 53.8% market share in 2024, driven by stringent regulations on volatile organic compound (VOC) emissions and the necessity for hydrocarbon recovery. vapor recovery unit are extensively used in upstream, midstream, and downstream operations, including wellhead sites, storage tanks, and pipelines.

Regulatory frameworks like the U.S. EPA’s New Source Performance Standards (NSPS) have further amplified the adoption of VRUs, ensuring environmental compliance while enhancing operational profitability.

Chemical processing is poised to grow at a CAGR of 10.5% during the forecast period. The sector faces stringent mandates for VOC control, such as the European Union’s Industrial Emissions Directive, which has propelled the demand for advanced vapor recovery unit.

These units enhance operational efficiency by recovering valuable hydrocarbons, minimizing waste, and reducing environmental impact, making them integral to modern chemical manufacturing facilities. Regulatory initiatives promoting eco-friendly practices are further driving their adoption in this sector.

The pharmaceuticals segment is witnessing steady adoption of VRUs due to stringent quality standards and environmental compliance requirements. VRUs help capture solvent vapors during production processes, ensuring product integrity while adhering to emissions guidelines.

The food and beverage industry is emerging as a key application area for VRUs. These systems are used to recover vapor during processing and packaging, preserving product quality and minimizing losses. As the industry focuses on waste reduction and sustainability, VRUs are becoming a valuable tool in meeting these objectives.

North America led the global vapor recovery unit market with a 34.5% market share in 2024, driven by strict regulatory frameworks and robust oil and gas infrastructure. The U.S. dominates the region, with high adoption rates in upstream and midstream operations.

For example, the EPA’s Greenhouse Gas Reporting Program has incentivized VRU deployment in natural gas processing plants. Additionally, technological advancements by key players like Zeeco and Flogistix are further boosting regional demand.

Europe accounted for 26.2% of the vapor recovery unit market in 2024, propelled by the region’s commitment to carbon neutrality and VOC emission control. Countries like Germany and the Netherlands are leading adopters, leveraging VRUs in chemical manufacturing and refining processes. The European Union’s stringent directives, such as the Industrial Emissions Directive, are creating favorable conditions for market growth.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 8.2% during 2026–2033. Rapid industrialization, increasing energy demand, and supportive government initiatives like India’s NCAP are key growth drivers. China’s emphasis on methane reduction in its 14th Five-Year Plan has also accelerated vapor recovery unit adoption in petrochemical and gas distribution sectors.

The Middle East and Africa region is emerging as a significant market of vapor recovery unit, driven by the expansion of oil and gas exploration activities. Saudi Arabia’s Vision 2030 and large-scale projects like NEOM are emphasizing sustainable practices, including vapor recovery systems.

Latin America, led by Brazil, is gaining momentum due to rising investments in oil and gas and favorable policies promoting emission control. For instance, Mexico’s Energy Transition Law has spurred the adoption of VRUs in refining and storage facilities.

The global vapor recovery unit market was valued at approximately USD 800 million in 2024.

The VRU market is expected to grow at a CAGR of 6.8% during the forecast period from 2026 to 2033.