Warehousing and Storage Services Market

Warehousing and Storage Services Market Size, Share & Trends Analysis Report By Type (General Warehousing and Storage, Refrigerated Warehousing and Storage, Farm Product Warehousing and Storage), By Ownership (Private Warehouses, Public Warehouses, Bonded Warehouses), By End-User Industry (Manufacturing, Healthcare, Other End-User Industries) market Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

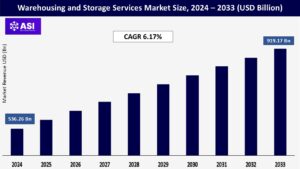

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.17%

Last Updated : December 16, 2025

The global warehousing and storage services market size was valued at USD 536.26 billion in 2024 and is expected to grow from USD 569.35 billion in 2025 to reach USD 919.17 billion by 2033, growing at a CAGR of 6.17% during the forecast period (2025-2033).

Warehousing and storage services offer storage for the commodities owned by another business or organization, including their products, vehicles, equipment, parts, and perishable goods. This frequently includes distribution and inventory management.

Both short-term and long-term contractual storage arrangements are possible. The ability to adjust the environment, such as temperature and humidity, may be included in warehouse and storage facilities to extend product lifespan or prevent item degradation.

Major online brands entering physical storefronts have considerably increased the omnichannel supply chain. Some people find the speed and force of changing business dynamics overwhelming. Intelligent retail solutions are now implicitly required by the intelligent consumer.

Different consumer groups use a variety of retail channels to shop and select products that suit their needs and way of life. Businesses have thus realized that expanding customer options and the buying experience drives profitability. The key phrase for medium and large brands will be “Omni-channel retail” as they push to expand B2C and B2B e-commerce.

The interoperability of various channels and the accessibility of more recent technologies for visibility have made it possible for merchants to fulfill orders from the closest fulfillment center, which has reduced the impact of inventory holding costs over time. As a result, shipping costs have decreased, and consumer satisfaction has increased, encouraging repeat business.

An omnichannel network takes pride in emphasizing the consumer experience. Customers feel in charge and independent of the manufacturer because they may contact them anytime and request assistance if necessary.

The explosive growth of e-commerce has fundamentally transformed warehousing requirements, with major retailers expanding their distribution networks to meet growing consumer demands.

For instance, Walmart’s strategic network of 31 dedicated e-commerce fulfillment centers and 4,700 stores within 10 miles of 90% of the U.S. population demonstrates the scale of infrastructure needed to support modern e-commerce operations.

This expansion has led to the development of both mega-fulfillment centers exceeding 1 million square feet and smaller facilities strategically located near urban centers, creating unprecedented demand for varied storage services.

The evolution of e-commerce has necessitated the development of more sophisticated warehousing solutions, particularly in handling returns and managing inventory across multiple channels.

Warehouses are increasingly adopting automation and sortation equipment to minimize labor requirements and reduce product touches, while implementing labor management systems to track and monitor productivity.

The industry has also witnessed a significant shift toward waveless picking systems, which continuously evaluate order pools and automatically release work based on variables such as order priorities and facility processing capacities, enabling more efficient e-commerce fulfillment operations.

Maintenance and site upkeep is essential to keeping operations running smoothly, even more so in a quick-moving supply chain system where a single error or problem could significantly impact operations.

The cost of cold storage and temperature control in general facilities is high and can result in significant losses if done incorrectly. Lighting and temperature control are a warehouse’s two major energy consumers (in the form of heating, cooling, or refrigeration).

Therefore, the quickest approach to saving energy is to lower the costs of these two significant contributors. Other significant costs include labor and rent.

Due to damage, the monthly amount of freight passing through the warehouse is a crucial cost factor for maintenance. At the same time, the location and age of a facility are particularly relevant elements of breakdown maintenance.

Therefore, it becomes evident that frequently moving warehouses to meet the changing needs of freight volume and to use young building facilities is a valuable management practice based on both the difficulty of estimating future market demand and the relevance of the building’s age in determining building management costs.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

General Warehousing and Storage Refrigerated Warehousing and Storage Farm Product Warehousing and Storage |

| By Ownership Type |

Private Warehouses Public Warehouses Bonded Warehouses |

| By End-Use Type |

Manufacturing Healthcare Other End-user Industries |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The general segment owns the highest market share and is expected to grow at a CAGR of 7.00% during the forecast period. The global need for e-commerce is likely to increase demand for general warehousing. Clothing and accessories, fashion, consumer electronics, home and garden, and sporting items are some important product categories.

As a result of COVID-19, the demand for general storage increased sharply in the second half of 2020. The household demand from metropolitan areas worldwide has been a primary driver of this need. The supply chain disruption and logistical difficulties experienced in H1 were lessened by the restart of industrial output that gradually relaxed lockdown limitations.

Based on the Global Cold Chain Alliance’s measure of market penetration, chilled warehouse space was unevenly distributed among nations. In 2018, the capacity of all refrigerated warehouses globally increased by 2.67% to 616 million cubic meters from the capacity reported in 2016. With 150 million cubic meters, India has the largest country market by far, followed by the United States with 131 million cubic meters and China with 105 million cubic meters.

In 2020, the capacity of all refrigerated warehouses globally increased by 16.7% to 719 million cubic meters. North America and China accounted for the majority of the increase in capacity since 2018.The farm product warehousing and storage segment plays a crucial role in the agricultural supply chain, offering specialized agricultural storage solutions for agricultural commodities.

This segment has evolved significantly with the integration of advanced monitoring systems and climate control technologies to maintain optimal storage conditions for various agricultural products. The segment’s importance has been heightened by the growing focus on food security and the need for efficient agricultural supply chain management, particularly in major agricultural producing regions. The development of smart storage solutions and the implementation of sustainable practices have further enhanced the segment’s value proposition in the overall warehousing market.

Private warehousing dominates the global warehousing and storage services market, commanding approximately 50% market share in 2024. These warehouses are typically established by private enterprises for their specific purposes, offering highly flexible and customizable storage solutions that can be tailored to the nature of products being stored.

Private warehouses are strategically located to address the requirements of manufacturing and commercial units, providing enterprises with complete control over their storage operations. These facilities can be either self-operated or managed by third-party logistics providers (3PLs), making them particularly attractive for large enterprises with substantial warehousing requirements.

The segment’s prominence is further strengthened by major international conglomerates in the construction and manufacturing sectors who own significant warehousing spaces, contributing to its market leadership position.Governments generally create public warehouses, which are authorized to be used by private parties (including cooperative societies). One can rent out public warehouses for both professional and private purposes.

These are frequently utilized by manufacturers, wholesalers, exporters, importers, and government organizations to receive and deliver their goods. They are typically situated near transportation lines, such as railways, highways, rivers, etc. Public warehouses offer monthly short or long-term storage. Pallets stored and square footage used can be used to determine the cost of storage.

The manufacturing segment continues to dominate the global warehousing and storage services market, holding approximately 33% market share in 2024. This significant market position is driven by increasing demand from the automotive, electronics, and industrial manufacturing sectors requiring sophisticated warehousing solutions.

The segment’s prominence is further strengthened by the growing adoption of automation and smart warehousing technologies in manufacturing facilities, enabling improved inventory management and operational efficiency. Manufacturing companies are increasingly outsourcing their warehousing needs to specialized service providers to optimize their supply chain operations and reduce operational costs.

The rise of Industry 4.0 and smart manufacturing practices has also contributed to the segment’s dominance, as manufacturers require more advanced warehousing solutions to support their digitalized operations. The healthcare segment is emerging as the fastest-growing segment in the warehousing and storage services market, with projections indicating robust growth from 2025 to 2033.

This exceptional growth is primarily driven by the increasing demand for specialized pharmaceutical warehousing facilities for pharmaceutical products, medical devices, and healthcare supplies.

The segment’s expansion is further fueled by stringent regulatory requirements for healthcare product storage, growing adoption of temperature-controlled warehousing solutions, and the rise in pharmaceutical manufacturing activities globally.

The implementation of advanced warehouse management systems (WMS) in healthcare facilities is also contributing to this growth, as these systems help optimize inventory management and ensure compliance with quality control standards.

Additionally, the increasing focus on maintaining efficient healthcare supply chains and the growing trend of outsourcing warehousing operations in the healthcare sector are expected to sustain this segment’s rapid growth trajectory. The warehousing and storage services market encompasses several other significant segments, including consumer goods, food and beverages, retail, and other miscellaneous industries.

The consumer goods segment is characterized by the growing demand for omnichannel distribution capabilities and e-commerce fulfillment centers. The food and beverages segment is driven by the need for specialized temperature-controlled storage facilities and strict compliance with food safety regulations.

The retail segment continues to evolve with the changing landscape of online and offline retail operations, requiring more sophisticated warehousing solutions. These segments collectively contribute to the market’s diversity and demonstrate the varied applications of warehousing services across different industries, each with its unique storage requirements and operational challenges.

The Asia-Pacific warehousing and storage services market is positioned for exceptional growth, with projections indicating a robust growth rate of approximately 8% during the period 2025-2033. The region’s warehousing sector is undergoing significant transformation, driven by rapid urbanization and the expansion of e-commerce platforms.

The market is characterized by increasing investments in modern warehousing facilities, particularly in emerging economies such as India, China, and Southeast Asian nations. Technological advancement in warehouse operations, including the adoption of automation and digital solutions, is reshaping the industry landscape.

The European warehousing and storage services market has demonstrated robust growth, recording an impressive expansion of approximately 19% between 2019 and 2024. The market is characterized by increasing investments in automation and digital transformation initiatives across warehousing operations.

The region’s warehousing sector is experiencing significant evolution in response to changing retail patterns and the growth of e-commerce platforms. Major developments are concentrated in key logistics hubs across Germany, France, the Netherlands, and the United Kingdom, with particular emphasis on developing sustainable and energy-efficient warehousing solutions.

The market is witnessing a notable trend toward the adoption of multi-modal optimization strategies, enabling sophisticated planning across regions and transport modes.

North America represents a mature and highly sophisticated warehousing and storage services market, commanding approximately 25% of the global market share in 2024. The region’s dominance is driven by the robust e-commerce sector, with web-based shopping becoming increasingly popular across all customer segments.

The market is characterized by advanced automation technologies, sophisticated warehouse management systems, and a strong focus on operational efficiency. The demand for outsourcing warehousing services continues to grow, particularly from manufacturing companies expanding their production and operational capacities.

The region’s warehousing infrastructure is notably advanced in terms of technology adoption, with widespread implementation of IoT, automation, and real-time tracking systems.

The market is expected to grow CAGR of 6.13 % from 2025 to 2033.

The current market size is USD 536.26 Billions in 2024.

North America currently holds the largest market shares.

Top 12 industry players in warehousing and storage services market are, Deutsche Post DHL Global, XPO Logistics, Ryder System Inc., NFI Industries Inc., Americold Logistics, FedEx Corporation, Lineage Logistics, NF Global Logistics Ltd, APM Terminals, DSV Panalpina AS, Kane Is Able, MSC Mediterranean Shipping Co. SA, etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Warehousing and Storage Services Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Warehousing and Storage Services Market, By Ownership Type

5.3 Warehousing and Storage Services Market, By End-Use Type

6.1 North America Warehousing and Storage Services Market , By Country

6.1.1 Warehousing and Storage Services Market, By Type

6.1.2 Warehousing and Storage Services Market, By Ownership Type

6.1.3 Warehousing and Storage Services Market, By End-Use Type

6.2 U.S.

6.2.1 Warehousing and Storage Services Market, By Type

6.2.2 Warehousing and Storage Services Market, By Ownership Type

6.2.3 Warehousing and Storage Services Market, By End-Use Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping