X-ray Machine Manufacturing Market

X-ray Machine Manufacturing Market Share and Trend Analysis, By Technology Type (Analog, Digital), By Application (Medical Diagnostics, Security Screening, Industrial Inspection), By End User (Healthcare Providers, Transportation and Logistics, Government Agencies, Industrial Enterprises) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 4.63%

Last Updated : March 31, 2026

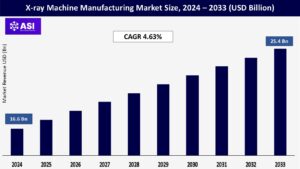

The global X-ray Machine Manufacturing Market size was valued at USD 16.6 billion in 2024 and is projected to reach USD 25.4 billion by 2033, expanding at a compound annual growth rate CAGR of 4.63% during the forecast period (2025 – 2033).

The industry for producing x-ray machines is all about producing the cutting-edge equipment which allows us to visualize what lies beyond surfaces. These devices are critical in medicine, with doctors employing them daily to diagnose broken bones, find tumors, monitor lung disease, and guide treatments.

Their utility extends far beyond the hospital walls. Airports and borders depend heavily on X-ray scanners to provide security, scanning luggage and cargo for dangers. Industrial X-ray devices carry out critical non-destructive testing in workshops and factories, examining pipeline welds, testing airplane parts for defects, and testing cast metal components for integrity without damaging them.

Its special capability to expose inner information non-invasively makes X-ray technology a vital tool in medicine, security, and heavy industry. In turn, the manufacturers continue to innovate under sustained pressure to create increasingly precise, effective, and safe imaging technology across all these varied industries.

The unchecked increase in chronic diseases all over the world is among the most significant drivers of the X-ray machine production market. Diseases such as cardiovascular disease, various cancers, osteoporosis, and chronic respiratory diseases are increasing, primarily by virtue of the effects of population aging and lifestyle changes.

Early diagnosis and proper monitoring are the keys to the effective management of these diseases, and X-ray imaging is a timeless, ubiquitous first-line diagnostic modality. Hospitals, specialty clinics, and diagnostic labs are henceforth investing substantially in refurbishing existing equipment and procuring new, state-of-the-art X-ray machines to improve diagnostics and patient throughput.

This demand is also fueled by the huge upgrades and increases in healthcare infrastructure, most notably among the developing economies as access to basic diagnostics is growing rapidly. Further, outpatient trends and increased demand for point-of-care diagnosis propel demand for mobile and portable X-ray devices.

These devices enable imaging in the very center of emergency rooms, intensive care units, nursing homes, and even in the homes of patients, expanding accessibility and lighter loads on centralized facilities.

The intersection of increasing disease burden, increasing healthcare access, and operational necessities of needing agile imaging solutions drives sustained, solid demand for producers throughout the full range of X-ray technology.

The business of making X-ray machines is being driven fundamentally and in the direction of advancement by unrelenting technological advances. The revolutionary change from traditional analog film-based technologies to computed radiography (CR) and digital radiography (DR) has transformed the landscape.

Digital technology has definite benefits: taking images much faster (seconds compared to minutes), better image quality with greater resolution and contrast, and much lower doses of radiation to the patient.

In addition, computer detectors combined with advanced software support real-time integration with Picture Archiving and Communication Systems (PACS) and Electronic Health Records (EHR), providing access to images to share in real time, remote consultation, and streamlined workflows that optimize radiologist productivity and diagnosis quality.

This kind of electronic infrastructure is needed to support tele-radiology and more widespread telemedicine programs. Aside from digitization, advancements in very high-powered portable and mobile X-rays have expanded the field of application to ambulances, field clinics, sports centers, and inspection units in the industrial sector.

Most importantly, compatibility with Artificial Intelligence (AI) is revolutionary. AI-based programs aid image inspection, rendering activities such as anomaly identification, initial interpretation, and quality control independent, resulting in quicker diagnosis, less human error, and maximum functioning efficiency.

This ongoing wave of innovation keeps X-ray systems more powerful, easier to use, and more versatile, fueling replacement cycles and fresh adoption across a broad spectrum of industries.

Exorbitant prices of today’s X-ray technology are still a key inhibitor for the overall market growth. Installation of high-end digital radiography (DR) technology entails a huge upfront investment. This is a colossal obstacle, especially for small clinics, private practice physicians, and health centers working in less-advantaged environments or in developing countries.

Aside from the initial acquisition price, the actual cost of acquisition holds significant ancillary charges: unique installation needs, strict initial and continued calibration, mandatory periodic software updates required by law, and ongoing adherence to rigorous radiation safety protocols.

Maintenance contracts and unplanned repairs also contribute to consistently increasing operation costs, constantly subjecting operators to financial strain. This is worsened in areas where there is no easily available skilled technical know-how or immediate access to authentic spare parts, and thus, potentially long equipment downtime.

Therefore, the cost typically causes cost-sensitive facilities to postpone upgrades, extend the life of current older analog or CR units, or take used equipment rather than spending money on newer digital equipment. This economic factor retards the technology diffusion rate in the entire market, stifling overall growth potential and maintaining disparities in access to cutting-edge diagnostic imaging.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology Type |

Analog Digital |

| By Application |

Medical Diagnostics Security Screening Industrial Inspection |

| By End Use |

Healthcare Providers Transportation and Logistics Government Agencies Industrial Enterprises |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The market naturally divides between digital and analog X-ray equipment. Digital technology has quickly displaced former analog technology as the leading force, through its overwhelming advantages: increased image resolution providing more precise diagnoses, substantially lower radiation doses providing higher patient protection, and substantially improved image processing speeds enhancing workflow productivity.

Far more significant, however, is that digital technology allows easy storage of images in Picture Archiving and Communication Systems (PACS), with instant recall at the touch of a button, and straightforward sharing, which underpins contemporary collaborative care, telemedicine, and unified electronic health records.

Analog systems remain in use in some resource-poor settings or specialized applications because of their lower initial purchase price, but they represent a shrinking niche. The transition to digital is led almost entirely by healthcare providers worldwide, spurred by strict regulatory demands for better care quality and reduced radiation exposure, the significant operational advantages of digital workflows, and the requirement for enhanced diagnostic ability.

This strong combination of regulatory requirements, advances in operational efficiency, and clinical excellence guarantees digital X-ray systems dominate the market currently and set the direction it will take into the future, with ongoing innovation toward advancing digital detectors, compatibility with software, and analytics using AI.

Digital X-ray technology has excellent versatility across large industries. The biggest and most significant application field is healthcare. Medical X-ray equipment is a critical diagnostic device, employed every day to detect bone fractures, lung diseases (like pneumonia or tuberculosis), breast cancer screening (mammography), abdominal ailment evaluation, guiding minimal invasive procedures, and tracking the outcome of treatment.

Beyond medicine, security screening is a major application. X-ray scanners are ubiquitous throughout airports to scan people and bags, the linchpin to border crossings and ports to inspect cargo, and installed in government offices and public space throughout the world to detect weapons, bombs, and contraband, a pillar of contemporary security infrastructure.

Industrial applications constitute the third broad pillar. Industrial radiography applies X-rays during non-destructive testing (NDT) to examine welds in pressure vessels and pipelines, to detect defects or cracks in key aerospace parts, to confirm the integrity of castings and forgings, and to perform quality control during production without compromising the integrity of the tested object.

Each use sector has individual technical specifications, regulatory needs, and drivers of innovation, but taken as a whole, they reflect the extensive application of X-ray imaging technology in health protection, security, and industrial quality.

Demand for X-ray machines stems from a wide variety of end-user markets, each with its individual specifications. Hospitals are the biggest single market, fueled by their full-service diagnostic imaging needs in their radiology divisions, emergency rooms, operating rooms (C-arms), and bedside settings (mobile X-ray).

They require high-throughput, state-of-the-art systems integrated into an advanced workflow. Diagnostic Imaging Centers and Clinics are another large health-care user segment, covering mostly outpatient diagnostic imaging, which in many cases calls for efficient, cost-effective digital systems for high-volume studies.

Outside of conventional health care, Transportation Hubs (airports, seaports, railway stations) and Logistics firms are frequent-use customers, employing high-throughput security scanners to inspect bags, cargo, and parcels for safety and regulatory compliance.

Government Agencies such as Customs and Border Protection, Homeland Security, and defense ministries purchase advanced systems for safeguarding critical infrastructure, border cargo screening, and law enforcement. Lastly, Industrial Enterprises from various industries such as aerospace, automotive, energy (oil & gas), construction, and manufacturing use industrial X-ray equipment for preventive infrastructure maintenance, production line quality control, and non-destructive testing.

The huge range of end-users underscores the technology’s intrinsic position in all essential aspects of societal function – health, security, and industrial integrity – that fuel steady and multi-faceted market demand.

North America dominates the world X-ray machine market due to improved healthcare infrastructure, heavy expenditure, and fast adoption of digital technology. Top players have a strong presence here supported by heavy R&D spending. High proportion of elderly population provides a stable demand for diagnostic imaging.

Strongly enforceable regulatory standards guarantee equipment quality, and well-established reimbursement systems are present. Greatest digital benefits recognition by providers (e.g., less radiation and efficiency) starts replacement of old analog systems. That alignment of forces – technology leadership, demographic demand, and supportive financial institutions – verifies North America’s leadership.

Europe possesses great, mature share of the marketplace. Well-funded universal health care systems and conscientious focus on preventive care and early detection are the foundation of demand. Market leader nations (Germany, UK, France) strongly embrace high-technology digital X-ray equipment, which is backed by high private and public investment in facility modernization.

EU directives on image quality and radiation protection are significant drivers of technology replacement. The availability of established industry producers and the emphasis on operating efficiency also favor the market. Budget limitations in certain national health services occasionally slow the rate of new equipment adoption behind that in North America.

Asia Pacific has the most dynamic X-ray market in the world. The growth is stimulated by rising healthcare consciousness, growing middle-class populations, increased government spending on healthcare infrastructure, and rising chronic disease levels.

China, India, and Japan are transitioning quickly from analog to digital X-ray machines. It is fueled by upgrading diagnostic centers, increased patient volumes, and a push for greater access to care.

Although cost consciousness prevails, sheer volumes of demand and continued infrastructure development provide tremendous opportunities for producers, and APAC is the key driver driving future market expansion.

Latin America and the Middle East & Africa are growth markets with huge potential, albeit with lower penetration than other markets. In Latin America (i.e., Brazil, Mexico), rising healthcare access and investment in diagnostic technology are major drivers.

The MEA region is appealed to by government initiatives, especially in the Gulf Cooperation Council (GCC) countries, to enhance the health infrastructure and increase demand for advanced equipment.

Development is lopsided, however, and is undermined by such factors as budget constraints, inadequate technical expertise in certain sectors, and disorganized healthcare systems, especially in some African nations. Economic uncertainty may also impact the timing of investment in these countries.

The global X-ray Machine Manufacturing Market was valued at USD 16.6 billion in 2024.

The market is projected to grow at a CAGR of 4.63 % from 2025 to 2033.

Digital X-ray systems segment hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Canon Inc., GE Healthcare, Siemens AG, Philips Healthcare, Fujifilm Holdings Corporation, Shimadzu Corporation, Hitachi Medical Corporation, Hologic Inc., Carestream Health, and North Star Imaging Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 X-ray Machine Manufacturing Market, By Technology Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 X-ray Machine Manufacturing Market, By Application

5.3 X-ray Machine Manufacturing Market, By End User

6.1 North America X-ray Machine Manufacturing Market, By Country

6.1.1 X-ray Machine Manufacturing Market, By Technology Type

6.1.2 X-ray Machine Manufacturing Market, By Application

6.1.3 X-ray Machine Manufacturing Market, By End User

6.2 U.S.

6.2.1 X-ray Machine Manufacturing Market, By Technology Type

6.2.2 X-ray Machine Manufacturing Market, By Application

6.2.3 X-ray Machine Manufacturing Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping