Influenza Diagnostics Market

Influenza Diagnostics Market Share and Trend Analysis, By Technology (Reverse Transcription Polymerase Chain Reaction, Rapid Influenza Diagnostic Tests, Immunoassay), By Application (Type A Influenza Detection, Type B Influenza Detection), By End User (Hospitals, Laboratories, Point of Care Testing Settings) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

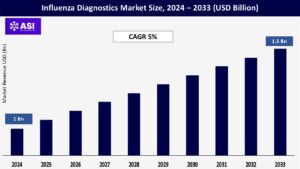

CAGR: 5%

Last Updated : January 21, 2026

The global influenza diagnostics market size was valued at USD 1 billion in 2024 and is projected to reach USD 1.5 billion by 2033, expanding at a compound annual growth rate CAGR of 5% during the forecast period (2025–2033).

Influenza testing involves a number of immunoassay tests aimed at the detection of the presence of influenza A and B viral nucleoprotein antigens in respiratory samples. The tests are utilized by the healthcare sector to screen and categorize influenza viruses within an effective time span, facilitating effective treatment and public health control. Rapid antigen tests, reverse transcription polymerase chain reaction, immunofluorescence assays, serology, and rapid molecular tests are some of the tests available.

Constantly changing in diagnostics and influenza virus studies makes the tests more efficient and effective, making intervention and evidence-based medical practices possible immediately to control outbreaks of seasonal flu and possible pandemics. Market growth is significantly fueled by heightened vaccination activity, availability of point-of-care testing, growing research on influenza viruses, and increased awareness through public health programs.

The global market for the influenza diagnostics is increasing at a fast rate due to the extremely high prevalence of seasonal influenza epidemics globally. Seasonal influenza epidemics impose a burden of millions of cases of severe disease each year, resulting in respiratory-related deaths of hundreds of thousands, rightly making the case for early and accurate diagnosis solutions. Increased disease burden has greatly heightened the level of awareness among healthcare workers and the general population for the necessity of early diagnosis and treatment of influenza infection, strengthening demand within the Influenza Diagnostics Market.

School campaigns and public health campaigns have also helped raise this consciousness to a further level, urging people to get themselves tested when they develop flu-like symptoms, especially during peak influenza seasons. Centers for Disease Control and Prevention recently announced that the flu season caused tens of millions of cases of illness, millions of visits to the doctor, and all-time highs in hospitalizations, emphasizing the ongoing threat posed by the flu and consequently the need for diagnostic products. Additionally, the pandemic of COVID-19 significantly increased awareness of respiratory infections, creating heightened surveillance and influenza diagnostics and other respiratory infections, consequently propelling growth in the Influenza Diagnostics Market.

Advancements in diagnostic technology for influenza are a major driver of market growth, transforming the face of influenza detection and treatment. Older methods like viral culture and serologic testing are being substituted by newer molecular tests like reverse transcription polymerase chain reaction and other nucleic acid amplification tests that are more sensitive, specific, and provide faster turnaround. Molecular laboratory tests have been a godsend in the diagnosis of influenza viruses even at low virus titers, improving patient outcomes and lowering rates of transmission. Point-of-care testing devices have transformed testing for influenza by facilitating on-site detection immediately, accelerating patient management decisions, and easing the load on central laboratory locations.

In addition, the incorporation of artificial intelligence and machine learning technologies into diagnosis platforms is propelling data analysis capacity, enhancing diagnostic performance, and facilitating the efficiency of test result analysis. Improvements in biosensor science and microfluidics are making diagnostic devices more portable and easier to automate and miniaturize, further making them more convenient in different healthcare environments. Both of these technologies combined are providing more efficient, accurate, and inexpensive influenza testing technologies thus propelling the growth of the influenza diagnostics market due to rising demand for rapid and accurate diagnostic measures.

Even with immense opportunities for expansion, the airway management devices market is afflicted by some severe issues of cost limitations and shortage of trained professionals. The newer airway management devices, especially the video laryngoscopes and the high-end intubating devices, are extremely costly and can be outside the reach of financially strained healthcare facilities. Such a budget constraint is very essential in developing countries where the construction of the health infrastructure is a continuous process and resource allocation towards necessary medical needs becomes a priority over specialist apparatus. Compounded to the intricacies is a lack of medical personnel with special skills for managing advanced airway management. Utilization of advanced airway equipment needs specialized skills and competence that are not present in every healthcare facility.

The curve of learning the new technologies is steep and will cause resistance from practitioners who are used to traditional methods. Simulation education and training programs, though a good thing in the long run, are ancillary costs that hospitals must weigh. In addition, the perpetual global shortage of health care professionals has worsened the issue at hand, as numerous facilities have been unable to provide satisfactory critical care and emergency room staffing levels at which airway management skills are required the most. The multi-dimensional nature of these hindrances poses insurmountable barriers to entry into such markets and health care facilities, which can discourage the adoption rate of new airway management solutions for their worth in clinical applications.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Reverse Transcription-Polymerase Chain Reaction (RT-PCR) Rapid Influenza Diagnostic Tests (RIDT) Immunoassay

|

| By Application |

Type A Influenza Detection Type B Influenza Detection

|

| By End User |

Hospitals Laboratories Point-of-Care Testing Settings

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Influenza diagnostics market is divided according to technology into the classical diagnostic tests and molecular diagnostic assays, each further sub-divided within the class. Classical diagnostic tests comprise rapid influenza diagnostic tests, direct fluorescent antibody test, viral culture, and serological assays. Of these, rapid tests have a dominant market share because of ease of use, delivery of results in minutes, and possible application at point-of-care settings.

Influenza A and B viral nucleoprotein antigens are identified by rapid tests in respiratory specimens and yield qualitative results for which they are suitable for initial screening and diagnosis, especially in outpatient clinics.

Molecular diagnostic products such as reverse transcription polymerase chain reaction, loop-mediated isothermal amplification, nucleic acid sequence-based amplification, and simple amplification-based assays are the fastest expanding category, driving growth in the influenza diagnostics market size Reverse transcription polymerase chain reaction, for instance, is becoming increasingly useful since its great sensitivity and specificity allow it to identify the genetic material of influenza virus in an early stage and to manage infection effectively. Molecular tests like these can identify influenza viruses even in low viral loads and differentiate between subtypes of influenza and provide tremendous advantages over the conventional ones.

The advancements in the diagnostic platforms, i.e., the creation of multiplex tests that are able to detect more than one respiratory pathogen at a time, are also generating demand for this segment and changing the entire market map.

The influenza diagnostic market, by application, is concentrating mainly on detection and identification of types of influenza virus, e.g., Type A and Type B, that cause the majority of seasonal flu infections globally.

Type A influenza viruses, due to their higher genetic diversity and capacity for antigenic shift, cause most influenza epidemics and all pandemics to date and are thus of particular interest for public health surveillance and in pandemic planning. Type A influenza lab detection frequently entails subtyping capability to distinguish between such strains as H1N1 and H3N2 whose identification carries important therapeutic and epidemiologic surveillance implications.

Type B influenza viruses, although typically milder illness and less pandemically potent than Type A viruses, are still a target of diagnostic testing due to the reality that they are responsible for a substantial proportion of seasonally associated influenza disease, especially among children. Performer of diagnostic tests among these two virus groups differs since evidence shows most rapid influenza tests are more sensitive in identifying Type A influenza than Type B.

The performer of difference determines test choice and interpretation in clinical use, especially in seasons where Type B viruses dominate. Constant optimization of the diagnostic tests is intended to counteract such performance disparities and increase detection accuracy for all influenza viruses, enabling further clinical management and public health intervention to seasonal epidemics of influenza.

Hospitals are a broad end-user segment which employs a variety of diagnostic products from high-end molecular tests to point-of-care tests for supporting patient care, infection control, and epidemiological surveillance. In hospital settings, diagnostic tests for influenza are performed in outpatient clinics, inpatient departments, and emergency departments to inform treatment, isolate patients, and initiate antiviral therapy.

Hospital-based and separate clinical laboratories provide centralized testing sites with advanced diagnostic equipment containing advanced virus characterization and large-throughput testing capabilities, for routine clinical practice as well as use in public health surveillance activities. The point-of-care testing market is growing at a fast pace due to the increased use of rapid diagnostic technology in physician offices, urgent care, retail clinics, and even in the home, further expanding the influenza diagnostics market size, offering instant testing and treatment outside the bounds of traditional lab. Such decentralization movement is also observed most vividly in the United States, where point-of-care diagnosis for influenza increasingly has become part of regular clinical practice due to advances in the reliability and accuracy of the tests.

Institutional and research organizations employ sophisticated diagnostic technologies primarily to conduct epidemiologic studies, develop vaccines, and monitor outbreaks, while contract research organizations conduct specialty testing on a contract basis to public health organizations and pharmaceutical corporations, especially clinical trials and outbreak investigations.

North America leads the worldwide influenza diagnostics market in terms of biggest market share because it has most well-developed healthcare infrastructure, highest incidence cases, and ambitious government interest in diagnosis technology.

The United States leads most of the market share in this market because of high influenza incidence rates, widespread healthcare infrastructure, favorable government spending, and direct presence in the region by leading diagnostic companies. Investment by the United States Department of Health and Human Services of more than one billion dollars in the construction of influenza surveillance and diagnostic infrastructure in the nation also promotes growth within the regional market.

The second-largest market for the diagnosis of influenza is found in Europe, distinguished by sophisticated health infrastructures, sophisticated government programs for disease surveillance, and rising healthcare expenditure. Innovative public health programs for the prevention and control of influenza drive the European market, in addition to rising awareness among medical professionals and the population in general of the need for early diagnosis. Germany, France, and the United Kingdom are some of the major drivers in the European market owing to their developed medical infrastructure and substantial investment in healthcare technology and research.

The Asia Pacific market is fast emerging as the most developing flu diagnostic market through rising health awareness, rising disposable income, and developing healthcare infrastructure. Large population base within the region, coupled with common prevalence of respiratory infections, creates tremendous demand for influenza diagnostic products. Japan, China, and India are few of the nations that are exhibiting high market growth, as they are defined by government programs aiming to develop the healthcare infrastructure and manage infectious diseases. The shift toward point-of-care testing observed in this market is also driving the market forward.

Both have slow but growing influenza diagnostic markets, fueled by health expenditure growth and awareness, and focused public and international disease surveillance programs. LATAM is dominated by Brazil with large shares for Mexico and Argentina, where national programs are helpful but affected by healthcare infrastructure gaps, balanced by enormous population growth opportunities.

MEA, a smaller market, has unflattering contrasts: The Gulf Cooperation Council countries at the top with sophisticated systems, while sub-Saharan Africa lags behind in terms of access and diagnostic capability, although external efforts are increasingly enhancing technology availability, especially in urban and private health facilities.

The global influenza diagnostics market was valued at USD 1 billion in 2024.

The influenza diagnosticsmarket is projected to grow at a CAGR of 5 % from 2025 to 2033.

Rapid Influenza Diagnostic Tests (RIDT) hold the largest market share of influenza diagnostics.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, Quidel Corporation, bioMérieux, Becton Dickinson (BD), Danaher Corporation, Hologic Inc., Meridian Bioscience, and Luminex Corporation.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Influenza Diagnostics Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Influenza Diagnostics Market, By Application

5.3 Influenza Diagnostics Market, By End User

6.1 North America Influenza Diagnostics Market , By Country

6.1.1 Influenza Diagnostics Market, By Technology

6.1.2 Influenza Diagnostics Market, By Application

6.1.3 Influenza Diagnostics Market, By End User

6.2 U.S.

6.2.1 Influenza Diagnostics Market, By Technology

6.2.2 Influenza Diagnostics Market, By Application

6.2.3 Influenza Diagnostics Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping