Industrial Phenols Market

Industrial Phenols Market & Trends Analysis Report, By Grade (Phenol, Cresols and Bisphenol A (BPA)), By Application (Plastics, Pharmaceuticals and Agrochemicals), By End User (Automotive and Construction, Healthcare and Electronics)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

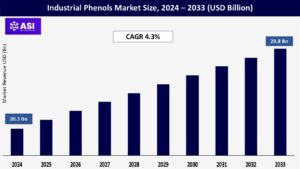

CAGR: 4.3%

Last Updated : March 16, 2026

The global Industrial Phenols Market size was valued at approximately USD 20.3 billion in 2024 and is projected to reach USD 29.8 billion by 2033, growing at a CAGR of 4.3% during the forecast period.

Industrial phenols are key chemical intermediates, primarily used in the production of plastics, resins, pharmaceuticals, and other specialty chemicals.

One of the main factors influencing the usage of phenol worldwide is the growing demand for bisphenol A (BPA), a crucial phenol derivative. The manufacturing of polycarbonates and epoxy resins, which are extensively utilized in high performance applications in the electronics, construction, and automotive sectors, depends on BPA.

These materials are perfect for consumer electronics, circuit boards, safety equipment, and structural components because of their exceptional mechanical strength, heat resistance, and longevity. The need for phenolderived resins is increasing along with the demand for materials that are strong, lightweight, and resistant to chemicals.

The demand for phenol-based goods is rising dramatically in Latin America and Asia-Pacific due to rapid urbanization and industrialization. The use of adhesives, laminates, coatings, and insulation materials is being driven by the region’s growing manufacturing, packaging, and construction industries.

The phenol industry is expected to grow steadily as consumer markets develop and infrastructure spending increases, particularly in nations like China, Brazil, and India.

Furthermore, these areas are becoming more and more desirable for phenol production and downstream processing due to their reduced production costs and the presence of important petrochemical hubs.

Given its poisonous, corrosive, and environmentally harmful qualities, phenol is categorized as a hazardous chemical. Skin burns, respiratory disorders, and systemic poisoning are only a few of the major health problems that can result from prolonged exposure.

Because of this, regulatory agencies including the EPA (U.S.), ECHA (Europe), and OSHA have implemented strict rules for how it should be handled, stored, and disposed of Manufacturers’ operational and compliance expenses are raised by these restrictions, especially in North America and Europe, which restricts market expansion in these areas. The increasing demand for environmentally friendly substitutes heightens the examination of items containing phenol.

Benzene and propylene, petrochemical derivatives that are correlated with the price of crude oil, are essential to the manufacturing of phenol. The economics of phenol production are directly impacted by the erratic swings in raw material prices caused by the intrinsic volatility of world oil markets.

Particularly for small and mid-sized firms, abrupt price changes might reduce profit margins and jeopardize the integrity of the supply chain. The phenol market is severely constrained by this price sensitivity, especially when there are supply interruptions in the oil industry or geopolitical unrest.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Grade |

Phenol Cresols and Bisphenol A (BPA) |

| By Application |

Plastics Pharmaceuticals and Agrochemicals |

| By End-Use |

Automotive and Construction Healthcare and Electronics |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Industrial Phenols Market is segmented by Grade (Phenol, Cresols and Bisphenol A (BPA)), By Application (Plastics, Pharmaceuticals and Agrochemicals), By End User (Automotive and Construction, Healthcare and Electronics).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Phenol (Dominant Segment)

Due to its extensive industrial application as a precursor in the synthesis of phenolic resins, caprolactam, and bisphenol A (BPA), pure phenol commands the biggest market share.

These downstream products guarantee a steady demand for base phenol worldwide since they are essential to a variety of industries, such as electronics, plastics, textiles, and the automotive sector.

Cresols and Bisphenol A (BPA)

Because they are used to make disinfectants, colors, perfumes, and antioxidants, cresols are becoming more and more popular. They provide particular chemical characteristics that are useful in formulations for specialized chemicals.

In the phenol value chain, bisphenol A is still a crucial commodity that is widely utilized in engineering plastics and high-performance polymers like epoxy resins and polycarbonates, which are essential in the consumer, automobile, aerospace, and electronics industries.

Plastics (Largest Application Area)

Plastics represent the largest application segment for phenol, primarily due to its use in producing polycarbonates and epoxy resins.

These materials offer excellent thermal stability, impact resistance, and transparency, making them indispensable in automotive components, electronic housings, construction materials, and consumer goods. Rising demand for lightweight and durable materials continues to drive this segment.

Pharmaceuticals and Agrochemicals

Phenol and its derivatives are critical intermediates in the production of antiseptics, anesthetics, herbicides, and various pharmaceutical agents.

In the healthcare sector, phenols are used in sterilization solutions, throat sprays, and analgesic products, while in agriculture, they are found in crop protection chemicals. The growing demand for advanced medical treatments and efficient agrochemicals supports steady growth in this segment.

Automotive and Construction (Key End Users)

Phenol-based materials are widely used in the construction and automotive industries because of their electrical insulation, flame resistance, durability, and thermal stability. Phenolic compounds are extensively utilized in the automotive industry for structural adhesives, brake systems, dashboards, and under-the-hood parts.

In order to satisfy the rising demand for energy efficiency and structural integrity in buildings and infrastructure, they are essential in the production of insulating foams, laminates, engineered wood products, and protective coatings.

Healthcare and Electronics

Electrical insulation, semiconductor packaging, and printed circuit boards (PCBs) all depend on phenol-derived materials like epoxy resins and phenolic laminates. Phenol’s superior mechanical and thermal resistant properties are advantageous for these uses.

Phenol is still used in healthcare in the production of intermediate pharmaceuticals, throat sprays, antiseptics, and sterilizing solutions. Its broad-spectrum antibacterial qualities make it useful in clinical and consumer contexts, particularly in light of growing awareness of infection prevention and cleanliness.

Despite facing increasing regulatory scrutiny and environmental restrictions, North America continues to maintain stable phenol demand, largely due to technological advancements and consistent consumption in engineering plastics, medical-grade resins, and automotive components.

The region benefits from a well-established manufacturing base, robust R&D infrastructure, and demand for high-performance materials in healthcare, aerospace, and electronics industries.

Asia-Pacific remains the growth engine of the global phenol market, with China and India leading the charge. Key growth drivers include a large-scale chemical manufacturing base, cost-efficient labor and production, and rising demand from the automotive, construction, electronics, and packaging sectors.

Rapid urbanization, expanding middle-class populations, and favorable government policies supporting industrial growth further boost regional phenol consumption.

The European phenol market is experiencing a gradual shift toward sustainability, driven by stringent environmental regulations and REACH compliance. As a result, there’s a growing interest in bio-based phenol alternatives.

Nevertheless, Europe continues to exhibit demand in high-value applications such as specialty pharmaceuticals, semiconductor manufacturing, and renewable energy technologies, where performance specifications still favor traditional phenol derivatives.

In Latin America and Africa, the phenol market is gaining traction due to increased infrastructure development, industrialization, and foreign investments in manufacturing.

These regions are witnessing rising demand for phenol-based adhesives, resins, coatings, and insulating materials, particularly in construction, furniture manufacturing, and consumer goods. However, market growth is moderated by regulatory challenges, limited technological infrastructure, and fluctuating raw material supply chains.

The market size of Industrial Phenols market is USD 20.3 billion.

The projected CAGR of Industrial Phenols market is 4.3%

Plastics, especially BPA and phenolic resin applications.

Asia-Pacific, led by China and India

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Industrial Phenols Market, By Grade

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Industrial Phenols Market, By Application

5.3 Industrial Phenols Market, By End-User

6.1 North America Industrial Phenols Market , By Country

6.1.1 Industrial Phenols Market, By Grade

6.1.2 Industrial Phenols Market, By Application

6.1.3 Industrial Phenols Market, By End-User

6.2 U.S.

6.2.1 Industrial Phenols Market, By Grade

6.2.2 Industrial Phenols Market, By Application

6.2.3 Industrial Phenols Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping