Teleradiology Market

Teleradiology Market Share and Trend Analysis, By Technology (Store-and-Forward Teleradiology, Real-Time Teleradiology, Hybrid Teleradiology), By Application (Routine Radiology Reporting, Emergency Radiology, Second-Opinion Services, Interventional Radiology Consultation, Educational & Research Applications), By End User (Hospitals & Clinics, Diagnostic Imaging Centers, Ambulatory Surgical Centers, Teleradiology Service Providers, Academic & Research Institutions) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 13.2%

Last Updated : April 2, 2026

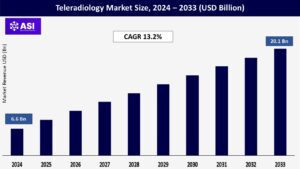

The global teleradiology market size was valued at USD 6.6 billion in 2024 and is projected to reach USD 20.1 billion by 2033, expanding at a compound annual growth rate CAGR of 13.2% during the forecast period (2025 – 2033).

Teleradiology is the process of transferring radiological images imagine X-rays, CT scans, MRIs, and ultrasounds, from where they are captured to some other place. This enables radiologists at some other place to read them or offer consultation. Hospitals and imaging facilities utilize secure telecommunications to forward patient scans to specialists, perhaps in other regions or time zones.

This method accelerates diagnostic activities while also providing high-quality radiology services to rural and underserved areas. Daily applications encompass emergency imaging support, second-opinion services, routine reporting, and academic studies.

Teleradiology solutions typically consist of modules for imaging capture, secure data storage, DICOM viewers, reporting software, and integration with hospital information systems. As an integral part of the broader telehealth context, teleradiology increases operational efficiency, reduces turnaround times, and supports clinicians in making timely, informed treatment decisions.

The past few years have witnessed healthcare professionals increasingly resort to telehealth to bridge the distance gap and deal with limited resources. As hospitals, clinics, and imaging centers computerize scanning, they look for systems that allow remote radiologists to examine scans without a physical presence.

Improved broadband, cloud storage, and cybersecurity now make it possible and reliable to transmit large image files securely. Deploying AI and ML algorithms into teleradiology platforms automates mundane tasks such as image segmentation, anomaly detection, or preliminary measurements, reducing radiologists’ workloads.

Intelligent tools flag critical cases, prioritize reading lists, and provide quantitative information for more accurate diagnoses. Augmented natural language processing (NLP) further simplifies report writing, and cloud-native architectures enhance scalability during spikes in demand. Meanwhile, web and mobile DICOM viewers enable radiologists to interpret images remotely, improving flexibility.

This combination of telehealth infrastructure and sophisticated analytics leads healthcare groups to make investments in teleradiology, looking to simplify operations, reduce report times, improve diagnostic accuracy using AI-augmented pattern recognition, and guarantee standardized imaging quality for networks. Integration with electronic health records (EHRs) also provides combined patient histories for more context-rich interpretations.

All over the world, demand for radiology services outstrips available specialists, particularly in developing regions. Hundreds of rural hospitals and small imaging centers don’t have on-site radiologists, resulting in delays in interpretation or transfers to urban centers.

Teleradiology bridges the gap by providing remote reporting 24/7, allowing images acquired evenings or weekends to receive prompt attention. Remote access to subspecialty reporting in neuroradiology, pediatric radiology, and musculoskeletal imaging is geographically restricted, compelling providers to refer cases to specialists overseas or hire international night-hawking services for around-the-clock coverage.

Academically, teleradiology facilitates collaborative research through the ease of multi-institutional image exchange and data collection. In addition, the COVID-19 pandemic underscored the necessity of remote work, compelling radiology departments to implement teleradiology to ensure care while decreasing on-site personnel.

This transition proved long-term sustainability, establishing teleradiology as a fundamental operational model beyond the crisis. As chronic illnesses, such as cancer, heart disease, and neurological disorders, increase, imaging volumes increase as well.

Teleradiology assists health systems in coping with this influx by distributing workload, avoiding bottlenecks, allowing for load-balancing over time zones, and ensuring uniform interpretation quality, driving market expansion. The aging population in industrialized countries further exacerbates this demand pressure for diagnostics.

Teleradiology clearly has benefits, yet safeguarding sensitive patient information is of paramount importance. Transferring large amounts of imaging data across networks introduces risks such as unauthorized usage, breaches, ransomware incursions, and possible violations of regulations such as HIPAA, GDPR, or local regulations.

Healthcare providers need to spend on robust encryption, secure VPNs, zero-trust networks, and multi-factor authentication to safeguard information while transferring and storing it. Implementation of standard procedures for image de-identification, secure storage, and audit trails introduces technical and cost complexity.

Business continuity and disaster recovery for distributed image repositories pose major technical hurdles. Where patchy regulations prevail, following different demands in terms of restrictions on cross-border data flows, varying requirements for patient consent, and local licensing of distant practitioners, where applicable, adds additional challenges.

Also, the absence of global standards for interoperability among varied picture archiving and communication systems (PACS) can hinder seamless data exchange, sometimes necessitating expensive middleware or bespoke integrations.

These security and regulatory concerns call for continuous IT expenses, personnel training, and periodic audits, which can slow down adoption, particularly among smaller imaging centers and hospitals with limited budgets. The dynamic nature of cyber-attacks demands relentless monitoring and expensive security patches.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Store-and-Forward Teleradiology Real-Time Teleradiology Hybrid Teleradiology |

| By Application |

Routine Radiology Reporting Emergency Radiology Second-Opinion Services Interventional Radiology Consultation Educational & Research Applications |

| By End User |

Hospitals & Clinics Diagnostic Imaging Centers Ambulatory Surgical Centers Teleradiology Service Providers Academic & Research Institutions |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

There are three types of teleradiology platforms: store-and-forward, real-time, and hybrid systems. Store-and-forward teleradiology is the most prevalent model; it records, anonymizes, and transmits imaging studies to distant servers where radiologists read them later. It is cost-effective and best suited for non-emergencies, with batch processing of overnight scans.

Real-time teleradiology, on the other hand, employs streaming technology to connect site technologists with remote radiologists, allowing for real-time guidance during scanning or instant reads for trauma cases. Such systems may require high-bandwidth, low-latency networks for clean images and unbroken communication.

Hybrid models combine both approaches: images are first sent store-and-forward for initial screening, and in the event of an emergency, a real-time session is initiated for interactive consultation. Some advanced platforms also include AI-driven triage, flagging critical cases (e.g., suspected strokes or pulmonary embolisms) for instant review.

As networks improve and 5G spreads, real-time and hybrid models gain ground, particularly in emergency radiology and tele-ultrasound. These platforms also offer secure cloud-based archives and scalable storage, enabling facilities to maintain historical imaging records without significant infrastructure investments.

Moreover, easy-to-use interfaces and configurable workflows minimize administrative weight and speed up report production. Continued research involves the integration of sophisticated machine-learning algorithms to improve diagnostic accuracy and predictive analytics.

Teleradiology meets a variety of essential healthcare applications. The most common is routine radiology reporting, wherein diagnostic images, X-rays, CTs, MRIs, and ultrasounds are read remotely to produce preliminary or final reports. Emergency radiology is another critical segment, providing 24/7 radiologist availability to read urgent studies and direct treatment for trauma, stroke, and other acute conditions.

In addition to clinical reporting, teleradiology drives second-opinion offerings, allowing experts to examine difficult or unusual cases requiring specialized expertise. This segment tends to appeal to academic institutions and reference labs interested in expanding their consult base.

Teleconsultation for interventional radiology can provide on-the-spot guidance during procedures, enhancing outcomes when resources are sparse. Also, teleradiology systems support education and research: trainees receive exposure to varied case archives, participate in multi-institutional research studies, and share image-based projects.

New applications include remote monitoring of transportable ultrasound devices and interfacing with robotics imaging platforms, supporting sophisticated diagnostics for distant or mobile clinics. Providers also tailor service packages according to facility size and patient load to support cost-effective deployment.

Collaboration tools enable multidisciplinary teams to view studies together, enhancing care coordination. Telepathology services are frequently part of teleradiology platforms that create diagnostic suites. Ongoing software interface development guarantees compatibility with new imaging modalities.

Users of teleradiology cover all healthcare environments. Hospitals and clinics are primary adopters, using it to handle peak loads, provide after-hours coverage, and access subspecialty reads. Large hospital networks often run in-house teleradiology hubs serving affiliated outpatient centers.

Diagnostic imaging centers, stand-alone or part of chains, use teleradiology to offer extended hours without extra on-site radiologists. Ambulatory surgical centers increasingly depend on it for pre-op and post-op imaging support, ensuring quick reads to speed up care.

Specialized teleradiology service providers are third-party vendors that provide cloud infrastructure and pools of off-site radiologists to facilities without in-house capability. Academic and research settings employ teleradiology to exchange anonymized data, facilitate multi-center trials, and educate residents.

Telemedicine pioneers are also beginning to combine teleradiology with other electronic health services such as teledermatology and telecardiology to provide comprehensive remote diagnostic solutions across specialties. These vendors upgrade their systems to keep pace with changing regulatory requirements and interoperability with electronic health records.

Portable imaging equipment combined with teleradiology overcomes rural challenges in distant areas so that clinicians can diagnose patients in outlying clinics. Staff proficiency is maintained through training modules within platforms as well as with system upgrades.

The leadership of North America in the teleradiology industry is promoted by sophisticated healthcare infrastructures, robust telehealth regulations, and extensive medical record digitalization. The US accounts for the greatest percentage, supported by supportive payment policies, consolidation of hospital networks, and early adoption of cloud-based PACS.

Canada’s public system also funds telehealth to cover off-remote communities. Sustained growth is promoted by a robust regulatory compliance and data security focus, in addition to collaborations between providers and technology vendors.

Europe demonstrates consistent teleradiology expansion driven by increasing cross-border employment, country-level telemedicine initiatives, and interoperability, such as the European Health Data Space. The UK, Germany, and France are ahead of adoption, taking advantage of strong broadband and centralized health information.

Regulatory harmonization under GDPR and the European Medical Device Regulation (MDR) will guarantee data quality and protection. Telehealth grants and public-private collaborations support growth in Eastern Europe, with remote locations becoming more accessible to radiology.

Asia Pacific is poised for rapid teleradiology uptake, fueled by increasing healthcare expenses, government initiatives for rural telemedicine, and expanding private hospital chains in China and India. Japan and South Korea spend big on AI imaging software, and Southeast Asian countries leverage telecom networks to enhance off-site diagnostics.

Local language support and varied regulatory compliance are areas of emphasis for market players. Collaborations among international vendors and domestic IT companies enable platforms to be customized to varied clinical requirements.

The Latin America, Middle East, and Africa (LAMEA) region represents emerging economies with high potential. Within Latin America, Brazil and Mexico are at the forefront of increasing healthcare digitalization and medical travel. In the Middle East, the UAE and Saudi Arabia are investing in intelligent hospitals to upgrade imaging.

In Africa, South African and Kenyan countries embrace teleradiology to combat radiologist scarcity in rural regions. Yet, unequal availability of broadband and budgetary constraints in certain areas hamper adoption, leading vendors to provide low-cost, scalable cloud solutions.

The global Teleradiology Market was valued at USD 6.6 billion in 2024.

The market is projected to grow at a CAGR of 13.2 % from 2025 to 2033.

The Store-and-Forward holds the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Philips, GE Healthcare, Fujifilm Corporation, Siemens Healthineers, Agfa-Gevaert Group, Carestream Health.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Teleradiology Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Teleradiology Market, By Application

5.3 Teleradiology Market, By End User

6.1 North America Teleradiology Market, By Country

6.1.1 Teleradiology Market, By Technology

6.1.2 Teleradiology Market, By Application

6.1.3 Teleradiology Market, By End User

6.2 U.S.

6.2.1 Teleradiology Market, By Technology

6.2.2 Teleradiology Market, By Application

6.2.3 Teleradiology Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping