Catheter Market

The Catheter Market Share & Trends Analysis Report, By Product Type (Cardiovascular Catheters, Urological Catheters, Neurovascular Catheters, Specialty Catheters, Intravenous (IV) Catheters, Others) By End User (Hospitals, Ambulatory Surgical Centers, Home Healthcare, Clinics, Dialysis Centers) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

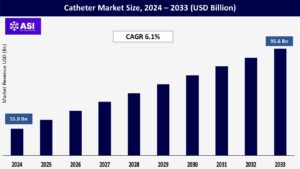

CAGR: 6.1%

Last Updated : November 8, 2025

The global Catheter Market was valued at approximately USD 55.8 billion in 2024 and is projected to reach USD 95.6 billion by 2033, growing at a CAGR of 6.1% during the forecast period (2025–2033).

Catheters are adaptable tubing inserted into a patient’s body to cure a disease or to allow a procedure to be performed surgically. They are classified as instruments in a number of medical disciplines including cardiology, urology, neurology, and oncology, among other fields, for diagnostic and therapeutic reasons. Some of the frequent activities with catheters include administering medications, draining bodily fluids, and gaining access to the vascular system to perform procedures, such as those used in angioplasty, dialysis, and catheter ablation.

The maximum share of the overall catheter market can consist of many types of catheters including cardiovascular, urologic, intravenous, neurovascular, and specialty catheters to name. The increasing growth of the catheter market is primarily due to the increase in the prevalence of chronic diseases such as cardiovascular disease and end-stage renal and the growing aging population; along with the increase demand for medical procedures that are minimally invasive and the growth and improved technologies such as drug-coated catheters; Antimicrobial catheters; the growing infrastructure of healthcare in emerging countries, and more hospital visits as patients apparently become more comfortable with surgery and diagnostic interventions thus adding more to the catheter market.

The growing global burden of chronic diseases, such as cardiovascular disease, end-stage renal disease (ESRD), cancer and neurologic diseases is impacting demand for a variety of catheters. The World Health Organization (WHO) reported that noncommunicable diseases (NCDs) cause 74% of total deaths globally, with cardiovascular disease causing 17.9 million deaths per year on its own.

Catheters play a critical role in the management and treatment of these conditions. Catheters are required for treatment and procedures related to hemodialysis, chemotherapy, central venous access (critical care), and cardiac. Among urinary and central venous catheters, there is evidence of an increasing use of catheters administered to hospitalized patients with urinary retention, sepsis, or hospital patients needing medication for long periods of time.

For example, CDC demonstrated in an article that about 25% of hospitalized patients receive a urinary catheter when hospitalized in the U.S. Consequently, Baxter International recently introduced in 2023 an entire advanced line of central venous catheters to lower the risk of infection and enhance patient comfort for central venous catheters.

The expanding number of hospital admissions and surgical procedures, as well as the growing volume of chronic illness cases, are all elevating demand for short-term and long-term catheter solutions for patients in hospital, nursing, and home care environments.

Innovation in technology is a key driver of growth in the catheter market, as healthcare systems shift toward safer, faster and less invasive procedures. Catheters are becoming more sophisticated and sophisticated in their designs and function, incorporating antimicrobial coatings, sensors for pressure, steerability, and integration with imaging modalities such as fluoroscopy and MRI.

Overall, these function-enhancing features aim to improve clinical outcomes, mitigate complications from catheterization, and improve the therapeutic efficacy of treatment or interventions. Most recently, in April 2024, Medtronic (NYSE:MDT) announced the launch of its next-generation Ablation Catheter System, offering smart thermal mapping for real-time feedback regarding tissue contact and patient temperature which can provide procedural precision during cardiac ablation procedures for atrial fibrillation.

A similar development is the expansion of Teleflex’s (NYSE: TFX) Arrow® EZ-IO® with a new line of vascular access products with improved vascular access solutions directed at emergency care providers. Additionally, developments in robotic-assisted catheter placements and image-guided interventions with catheters may continue to increase in demand as precision medicine becomes more embraced in various medical fields.

There was a broad approval market of over 30% in 2024 by the U.S. FDA year over year for minimally invasive vascular and neurovascular catheter-based systems which, added to the strong reports of new product dominance within the industry, exemplifies the emerging rapid transformation of innovation in the catheter related market space.

The high risk of catheter-related infection and its complications therefrom presents one of the largest restraints or risk factors limiting the overall growth of the global catheter market. Health care-associated infections (HAIs) cause additional patient morbidity, extended hospital stays and increased cost of health care. The most known HAIs are Catheter-Associated Urinary Tract Infections (CAUTIs) and Central Line-Associated Bloodstream Infections (CLABSIs).

The U.S. Centers for Disease Control and Prevention (CDC, 2019) reports that CAUTIs comprise over 30% of all HAIs reported in acute care hospitals, with CAUTIs representing over 500,000 cases, annually, in the United States. Similarly, CLABSI’s exceed 25% annual prevalence rate within acute care hospitals, can contribute to significant complications and represent additional treatment costs of over $45,000 each, with an estimated mortality rate of 12% to 25%, and prevalence of >75 infected patients per hospital (CDC, 2019).

The increased emphasis on patient safety and infection control have resulted in more scrutiny and regulations regarding the use of catheters and use of insertion techniques when catheters are used. Hospitals too are assessing their placement of catheters, and relying on alternatives if they can, to reduce the risks associated with catheters.

Most importantly, hospitals have limited or eliminated its overall or long-term use of catheters and/or specifically certain types of catheters, especially non-critical (ICU) settings. Despite technological advancements such as antimicrobial coatings and infection-resistant materials, the persistent challenge of managing catheter-associated complications continues to pose a barrier to market growth, particularly in developing regions with limited resources and lower compliance with infection control protocols.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Cardiovascular Catheters Urological Catheters Neurovascular Catheters Specialty Catheters Intravenous (IV) Catheters Others |

| By End User |

Hospitals Ambulatory Surgical Centers Home Healthcare Clinics, Dialysis Centers |

| Key Players |

Medtronic plc Boston Scientific Corporation Becton, Dickinson and Company (BD) Coloplast A/S Teleflex Incorporated Braun Melsungen AG ConvaTec Group Plc Hollister Incorporated Johnson & Johnson Services, Inc. Abbott Laboratories |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Catheter Market is segmented by product type and end-user. Each segment plays a vital role in enhancing diagnosis, treatment, and patient care across various medical fields.

In 2024, the Cardiovascular Catheters segment’s market share accounted for the largest portion, at 32.8%, attributed to the large volume of cardiovascular disease cases such as coronary artery disease and arrhythmias that require catheterizations. Further, increased utilization of various cardiovascular procedures, including angiography, percutaneous coronary interventions (PCI), and electrophysiology studies, requires catheters that results in strong demand for cardiovascular catheters.

The angiography catheters sub-segment remains the clinical leader in cardiovascular catheters due to their importance in imaging and treating vascular diseases. The Urological Catheters segment was also the next highest exhibitor for market share, often assigned to the growing population of urinary tract disorders, and an older population requiring long-term catheterization.

The most commonly urological catheters are Foley catheters, intermittent catheters, and external catheters; the latter two expect to increase for garnering attention from the risk of infection, and improved comfort. The Intravenous (IV) Catheters segment is also large, primarily attributed to the increasing utilization of central venous catheters (CVCs), and peripheral IV catheters for fluid administration, chemotherapy, and parenteral nutrition.

Recent development have stimulated the adoption of these IV catheters, such as the introduction of antimicrobial coatings and safety-engineered catheters for limiting blood pathogens in the critical care setting. The Neurovascular Catheters segment is experiencing significant growth due to the higher occurrence of neurological disorders, such as stroke and aneurysms. Growing awareness and accessibility to neurointerventional procedures are supporting this segment.

Hospitals control a whopping 61.5% of the catheter market share in 2024! Why? Because hospitals are the primary source of catheter utilization for acute care, surgical, critical care, and intervention. Tertiary care centers and specialty care hospitals largely dictate the demand for innovative catheter technologies. As outpatient procedures become more common, Ambulatory Surgical Centers (ASCs) are gaining activity in catheter utilization.

The convenience and lower cost imprinted in the ASCs promote catheters based minimally invasive procedures and diagnostic procedures, supporting modest increases in the catheter market space. The Home Healthcare market share is growing rapidly as the number of patients requiring long-term catheterization outside of the hospital is vastly increasing, i.e. urinary catheters and IV access to manage their chronic disease state.

Catheters are being developed to be easier to use and more sterile, as the patient population grows. Clinics and Dialysis Centers contribute to the phenomenon of increasing catheter usage in the market space by performing outpatient procedures for patients with chronic conditions with urological catheters and hemodialysis catheters.

At 39.4% share in 2024, North America will be the biggest market by region which is mainly attributable to steady growth in healthcare infrastructure, a higher prevalence of cardiovascular and chronic diseases, and efficient adoption of innovative catheter technology. The U.S. will be the stronghold of market growth through the high number of catheter-based diagnostic and intervention procedures performed in the healthcare systems, hospitals and outpatient centers, as well as home care. Moreover, continued increase in healthcare expenditures and strong reimbursement policies support further increases in utilization of catheters.

Europe, particularly Germany, France, the United Kingdom, Italy, and Spain, command an electoral share across the European Union involving European countries, whose healthcare market is slightly more coherent, with a prevalence of cardiovascular disease and urological issues requiring catheter-based procedures. In 2023, more than 1 million reported catheterization procedures occurred across the European Union. European market growth is generally driven by an aging population, increased spending on healthcare compared to GDP, and increased adoption of new designs of catheters to minimize risk of infection whilst also enacting better outcomes for the patient.

The Asia-Pacific region is expected to grow at the highest CAGR of 8.1% during the forecast period due to rising urbanization, increasing healthcare infrastructure, the growing healthcare expenditure by governments, and increasing geriatric population in markets like China, India, Japan, South Korea, and Australia. Increasing awareness regarding chronic diseases and growing access to minimally invasive procedures are the key factors driving growth in the catheter market.

The catheter market is growing moderately in Latin America and the Middle East & Africa regions, supported by rising healthcare investment and sustained efforts to manage cardiovascular and urological diseases. In these regions of Latin America and the Middle East & Africa, several countries also face significant market challenges: demographic and economic disparities; limited healthcare infrastructure; and limited access to advanced medical technologies limiting the growth of healthcare and the catheter market in the region

The catheter market was valued at USD 55.8 billion in 2024.

The catheter market is projected to grow at a CAGR of 6.1% from 2025 to 2033.

The Cardiovascular Catheters hold the largest market share of catheter.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Medtronic, Boston Scientific Corporation, and Philips Healthcare.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 The Catheter Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 The Catheter Market, By End User

5.1 North America The Catheter Market, By Country

6.1.1 The Catheter Market, By Product Type

6.1.2 The Catheter Market, By End User

6.2 U.S.

6.2.1 The Catheter Market, By Product Type

6.2.2 The Catheter Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping