Logistics Services Market

Logistics Services Market Share & Trends Analysis Report By Mode (Roadways, Railways, Airways, Waterways), By End-Use (Retail, Manufacturing, Healthcare, E-commerce, Others).

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

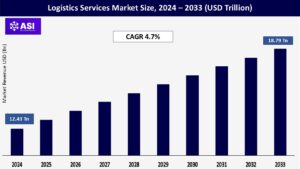

CAGR: 4.7%

Last Updated : June 2, 2026

The global Logistics Services Market size is expecting to reach USD 12.43 trillion in 2024, rising to USD 18.79 trillion by 2033, at a compound annual growth rate (CAGR) of 4.7%.

As the backbone of global trade and commerce, logistics services developing the planning, implementation, and management of goods, services, and information from origin to consumption. Accelerated by e-commerce expansion, digital transformation, and increasing international trade, the demand for efficient, tech-driven logistics solutions is rapidly expanding.

Logistics services are tough for proper supply chain operations, ensuring on time movement of goods, accessaries optimization, and customer satisfaction. The rise of e-commerce, technological advancements, and globalization of trade are key forces accelerating the growth of this sector.

The logistics industry is being propelled by a combination of e-commerce growth, urbanization, and global trade expansion. The surge in online shopping, especially post-pandemic, has created the need for faster and more reliable delivery services.

In addition, consumer expectations for real-time tracking, faster delivery, and flexible return policies are compelling logistics providers to upgrade their infrastructure and services.

Technological developments such as machine control warehouses, AI-driven route upgrade, and Internet of Things (IoT) in fleet management are improving supply chain efficiency and accuracy.

These improvements reduce delivery times, decrease errors, and help improving resource usage. Sustainability trends are also redevelopment of the industry. With increasing pressure to reduce carbon footprints, companies are investing in green logistics solutions, including electric delivery fleets and carbon offsetting programs.

Digital variations restructure logistics in way cloud-based platforms, data analytics, and blockchain for secure and transparent operations. These tools allow better inventory management, predictive maintenance, and demand forecasting, enhancing overall responsiveness and reducing costs.

The assumptions of warehouse robotics and autonomous delivery systems is next pushing the borders of efficiency and expandabilities in logistics performences. Digital implementationsare helps to sustainability by optimizing routes and enabling greener transport options. Customer experience is enhanced through real-time updates, chatbots, and flexible delivery options.

Additionally, paperless systems simple customs and compliance, decreasing late deliveries. Digital integration across the supply chain allows for seamless collaboration and faster response to disruptions. Overall, digitalization is transferred logistics into a more agile, data-driven, and customer-centric industry.

The companies grade supply chain flexibility between global unreliabilities. This coastal trend is beneficial for increasing demand for domestic and cross-border logistics services, especially in regions like North America and Europe.

The need for more flexible and graceful supply chains is increasing investment in multi-modal logistics, local warehousing, and last-mile delivery solutions. By transfer production closer to end markets, companies decreases lead times and transportation distances, improving quicker and more flexible delivery.

It helps increasing demand for regional logistics hubs and local warehousing, while decreasing reliance on long-haul ocean shipping. Instead, road, rail, and air freight become more prominent.

Although coastal production is involve higher worker costs, these are often offset by lower logistics expenses, decreasing inventory holding, and improved time-to-market. Additionally, regionalized supply chains are less vulnerable to global disruptions such as port delays or geopolitical instability.

For all strong demand, the market create conflicts like this infrastructure limitations, labor shortages, and increasing operational costs. Most of the countries , particularly in developing countries, they struggle with inadequate roads, ports, and rail networks, which can taking more time for shipments and increase transportation costs.

Driver shortages and high employee turnover in the transportation sector also pose ongoing issues, making it difficult for logistics companies to scale operations quickly. Moreover, volatile fuel prices and increasing compliance costs related to environmental and safety regulations can squeeze profit margins.

Other increasing aspects is cybersecurity. As logistics operations become more digitized, the risk of cyberattacks, data breaches, and system disruptions becomes more significant, requiring substantial investment in IT security and resilience measures.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Mode Type |

Roadways Railways Airways Waterways |

| By End-Use Type |

E-commerce Retail &FMCG Manufacturing Healthcare Others [Automotive, Construction,etc] |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Roadways transport is acquired the largest market shares of the global logistics services market. Road transport is most commonly used for freight transportation because it is cheap, easy, and can provide door-to-door service.

Technological advancements and the growing e-commerce industry are anticipated to bolster the growth of the roadways segment during the forecast period. The increasing number of global export and import activities is also another factor expected to drive the growth of the segment during the forecast period.

Road transportation offers unparalleled flexibility and accessibility, allowing goods to be transported directly from the point of origin to the final destination.

Roads provide connectivity to even the most remote areas, enabling door-to-door delivery and serving locations that may not be easily accessible by other modes of transportation.

Water ways holds the 20% market shares of the global markets. The waterways segment occupies the second-largest market position.

The growing development of infrastructure, such as canals that shorten trade routes, expand trade agreements, and increase consumer disposable income, is increasing global demand for international goods. These factors are poised to enable the waterways segment to maintain its second position throughout the forecast period.

Railways mode of transportations is acquired 18% market shares of the global logistics services markets. Railways, known for their environmental sustainability and large carrying capacity, continued to be a critical component of the logistics infrastructure.

Rail transport is particularly effective for long-distance, heavy freight, offering a balance between cost-efficiency and speed. Rail logistics plays a vital role in the transportation of goods, especially in the context of cross-border trade activities and trade contracts.

This sector encompasses the use of wheeled vehicles on tracks to move cargo from one place to another, ensuring a secure and efficient transport system.

Airways mode of transportations is acquired 15% market shares of the global logistics services markets. Airways, while less dominant, were essential for rapid deliveries and high-value goods. The speed and reliability of air transport make it indispensable for time-sensitive shipments, albeit at a higher cost compared to other modes.

E-commerce logistics acquired 35% market of services such as warehousing, transportation, and packaging solutions, facilitating management, movement, storage, and easy flow of goods in the online retail sector. The e-commerce logistics industry has undergone significant transformation over the past decade, driven by the rapid growth of online shopping platforms.

One of the key drivers is increasing consumer demand for fast and reliable delivery services. Companies are continually innovating to meet expectations, leveraging technology such as automated warehouses, real-time tracking systems, and data analytics to optimize supply chain efficiency.

Additionally, the emergence of omnichannel retailing, where consumers expect seamless integration between online and offline experiences, has further complicated logistics operations.

FMCG is captured 25% market of the global logistics services markets. FMCG is considered a unique business model that requires competitive advantages in manufacturing, branding, advertising, and logistics.

The key growth drivers for the consumer goods industry are changing lifestyles, ease of access, and rapidly changing consumer habits. Consumers expect a wide array of products to be always available in local stores and online. to achieve this, consumer goods companies tie up with global supply chains that are highly efficient, agile, and sustainable.

FMCG manufacturers are adopting collaborative logistics solutions that deliver products to stores faster and more cost-effectively. The recent e-commerce boom has also been a blessing for the FMCG industry.

Manufacturing transportations mode is acquired 20% market shares of the global markets. Manufacturing involves the production of goods on a large scale, leading to high volumes of goods that need to be transported, stored, and distributed. This results in a significant demand for logistics.

Many manufacturing companies operate on a global scale, sourcing raw materials from one country, manufacturing products in another, and distributing them to markets worldwide.

This globalization of manufacturing activities increases the complexity of logistics operations and drives demand for international freight forwarding, customs clearance, and cross-border logistics services.

Healthcare is acquire sonly 10% shares of the global logistics services markets. the cold chain segment plays an important role in the healthcare logistics market, which includes inflammatory drugs such as vaccines, vaccines, and blood products a highly desirable.

Recent advances in biotechnology, gene therapy, and personalized medicine have raised the need for robust cold-chain drug delivery systems. The cold chain segment dominates the market due to its high-value offerings and essential role in delivering critical medical products globally.

The COVID-19 pandemic highlighted the importance of cold chain logistics, as vaccines requiring ultra-low temperatures were distributed worldwide, cementing its dominance. Investments in cutting-edge technologies, such as the IoT-enabled temperature monitoring, and infrastructure like refrigerated warehouses, have strengthened this segment.

Automotive market acquired 10% market shares. The total logistics involved in automotive transportation continues to witness significant growth, driven by a rise in vehicle registrations as well as the need for organized warehousing of automotive parts.

OICA stated that there was a 12.3% increase in passenger car registrations in 2022-2023 and this registered an over 57 million total registrations. With trade and production of vehicles continuing to increase across all countries, there is a strong demand for robust and valid dispatch solutions, and this can especially be said for the global scene.

North America accounted for a 24% of the worldwide logistics services market in 2024. The North American freight and logistics landscape is experiencing significant transformation driven by infrastructure investments and regulatory changes. The United States Department of Transportation has allocated approximately USD 31 million to strengthen cargo infrastructure and enhance supply chain resilience.

This investment strategy demonstrates the region’s commitment to modernizing its logistics infrastructure and improving operational efficiency. In United States, infrastructure development and the rise of e-commerce are anticipated to boost employment in the transportation and storage sector.

An efficient and reliable transportation system is crucial for the economy. Through the National Trade Corridors Fund, the Government of Canada invests in improving supply chains, reducing trade barriers, and fostering business growth for future economic opportunities.

Europe is stay with the 22% market shares in the global markets of logistics services The European logistics market is undergoing a significant transformation driven by sustainability initiatives and infrastructure modernization.

Germany’s transportation sector currently accounts for approximately 20% of the nation’s emissions, prompting aggressive decarbonization efforts across the region. The industry is witnessing a rapid transformation in delivery services and logistics operations.

All supported projects are part of the Trans-European Transport Network, which connects EU Member States and aligns with the European Union’s goal of completing the TEN-T core network by 2030 and the comprehensive network by 2050, all while aligning with climate objectives outlined in the European Green Deal.

APAC leads with the 38% of the global logistics services market. The Asia Pacific’s exponential growth of e-commerce has highly spurred the need for advanced logistics networks.

Increased internet penetration and ubiquitous use of smartphones have enabled consumers in both urban and rural areas to access online retail websites, causing parcel volumes and delivery frequency to surge sharply.

This expansion of the digital customer base has forced the creation of flexible and scalable logistics solutions to enable quicker delivery and higher levels of service. Extensive investment in infrastructure and policy measures for regional economic integration are the primary drivers of logistics growth in the Asia Pacific region.

MEA is having only 16% share of the global logistics services market. The databook is designed to serve as a comprehensive guide to navigating this sector. The databook focuses on market statistics denoted in the form of revenue and y-o-y growth and CAGR across the globe and regions.

A detailed competitive and opportunity analyses related to logistics market will help companies and investors design strategic landscapes. Transportation services was the largest segment with a revenue share of 29.76% in 2024.

Horizon Databook has segmented the Middle East & Africa logistics market based on transportation services, warehousing and distribution services, freight forwarding services, inventory management services, value-added logistics services, integration & consulting services covering the revenue growth of each sub-segment from 2024 to 2033.

The market is expected to reach USD 16.18 trillion by 2033.

Asia-Pacific [APAC] dominating logistics service market.

Freight forwarding, transportation, warehousing, inventory management, last-mile delivery.

The E-commerce logistics is expecting to fastest grow segment.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Logistics Services Market, By Mode Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Logistics Services Market, By End-Use Type

6.1 North America Logistics Services Market, By Country

6.1.1 Logistics Services Market, By Mode Type

6.1.2 Logistics Services Market, By End-Use Type

6.2 U.S.

6.2.1 Logistics Services Market, By Mode Type

6.2.2 Logistics Services Market, By End-Use Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping