Meningococcal Vaccine Market

Meningococcal Vaccine Market Share & Trends Analysis Report, By Vaccine Type (Polysaccharide Vaccines, Conjugate Vaccines, Combination Vaccines, Men B Vaccines), By Serotype (Serogroup A, Serogroup B, Serogroup C, Serogroup Y, Serogroup W-135, Others), By Brand (Menactra, Menveo, Bexsero, Trumenba, Others), By End User (Pediatrics, Adults), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Government Supplies, Online Pharmacies)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

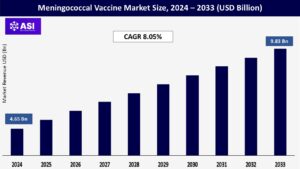

CAGR: 8.05%

Last Updated : January 22, 2026

The global meningococcal vaccine market size was valued at approximately USD 4.65 billion in 2024 and is projected to reach USD 9.83 billion by 2033, growing at a CAGR of 8.05% during the forecast period (2025–2033).

The meningococcal vaccine market refers to the global industry involved in the development, production, and distribution of vaccines that protect against meningococcal disease, a serious bacterial infection caused by Neisseria meningitidis. These vaccines are primarily used to prevent life-threatening conditions such as meningitis and septicemia, especially in infants, adolescents, travelers to high-risk areas, and individuals with certain medical conditions.

The vaccines are also administered during outbreak situations and as part of routine immunization programs in many countries. Key properties of meningococcal vaccines include their ability to stimulate a strong immune response (immunogenicity), safety with minimal side effects, and availability in different formulations such as polysaccharide, conjugate, and protein-based vaccines.

Conjugate vaccines, in particular, offer long-lasting protection and are effective across various age groups. The market continues to grow due to increasing awareness, government immunization initiatives, and the rising demand for preventive healthcare solutions across the meningococcal vaccine industry.

Governments and international health organizations like the WHO and GAVI are actively promoting routine immunization programs, especially in developing countries, to prevent meningococcal disease among high-risk populations.

These initiatives include mass vaccination campaigns, public health awareness efforts, and the integration of meningococcal vaccines into national immunization schedules.

Such programs drive consistent demand and ensure widespread access to vaccines, particularly in regions like Africa’s meningitis belt, , positively influencing the meningococcal vaccine market size.

The rising incidence and recurrence of meningococcal outbreaks globally have heightened the urgency for effective preventive measures. Outbreaks in densely populated areas such as schools, colleges, and refugee camps prompt emergency vaccination drives and stockpiling of vaccines, thereby boosting meningococcal vaccine market demand.

The unpredictable and potentially deadly nature of the disease further encourages individuals, healthcare providers, and policymakers to prioritize vaccination, contributing to sustained growth in the market. This unpredictability contributes to sustained meningococcal vaccine market growth.

One significant market restraint affecting the growth of the meningococcal vaccine market is the high cost of vaccine development and distribution, particularly in low- and middle-income countries, which may limit short-term expansion of the market size. The research and development process for meningococcal vaccines is complex and expensive, often involving advanced biotechnology, clinical trials, and rigorous regulatory approvals.

These high upfront costs can limit the entry of new players and make the vaccines less affordable for public health programs with limited budgets. Additionally, the requirement for cold chain logistics to maintain vaccine stability further increases distribution costs, especially in remote or underdeveloped regions with inadequate infrastructure.

As a result, access to meningococcal vaccines may be restricted in areas where they are most needed, hindering widespread immunization coverage and slowing overall meningococcal vaccine market growth despite rising global awareness and demand.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Vaccine Type |

Polysaccharide Vaccines Conjugate Vaccines Combination Vaccines Men B Vaccines |

| By Serotype |

Serogroup A Serogroup B Serogroup C Serogroup Y Serogroup W-135 Others |

| By Brand |

Menactra Menveo Bexsero Trumenba Others |

| By End User |

Pediatrics Adults |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Government Supplies Online Pharmacies |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The meningococcal vaccine market is segmented by Vaccine type, Serotype, Brand, End user, and Distribution Channels. Each factor plays a crucial role in improving public health outcomes, increasing the adoption of meningococcal vaccination programs, and supporting the development of more effective, broad-spectrum, and accessible vaccines for the prevention of meningococcal disease across diverse populations and regions.

Polysaccharide Vaccines: These are older-generation vaccines that offer short-term protection and are typically used during outbreak situations or in adults. However, their limited immunological memory and inefficacy in young children have led to reduced preference in favor of newer vaccine types.

Conjugate Vaccines: Represent the largest meningococcal vaccine market share due to their strong and long-lasting immune response. They are widely used in pediatric immunization and routine vaccination programs as they provide immunological memory and are effective in infants and young children.

Combination Vaccines: These vaccines offer protection against multiple pathogens, combining meningococcal components with other vaccines (e.g., DTP, Hib). Their ability to reduce the number of injections increases compliance and convenience, particularly in pediatric vaccination schedules.

Men B Vaccines: Targeting serogroup B, these are increasingly important in high-income countries where serogroup B is more prevalent. Vaccines like Bexsero and Trumenba fall into this category and are often recommended for adolescents and young adults.

Serogroup A: Common in the “meningitis belt” of sub-Saharan Africa, leading to significant demand in African immunization programs.

Serogroup B: Prevalent in Europe and North America; increasing incidence has led to focused development and approval of MenB vaccines.

Serogroup C: Historically, a major cause of meningitis in various regions, but widespread vaccination has reduced its incidence significantly.

Serogroup Y and W-135: These are emerging in certain parts of the world and are typically covered by quadrivalent vaccines (e.g., MenACWY), boosting demand for multivalent products.

Others: Include rarer or regional strains (e.g., serogroup X), which are under continued surveillance and research, especially for potential inclusion in broader-spectrum vaccines.

Menactra (Sanofi): A conjugate vaccine covering A, C, Y, and W-135 serogroups; widely used in the U.S. and other developed countries. Menveo (GSK) Another conjugate vaccine with similar serogroup coverage, known for its strong immunogenic profile and use in multiple age groups.

Bexsero (GSK): A recombinant protein-based vaccine specifically designed for protection against serogroup B, popular in Europe and North America. Trumenba (Pfizer) Competes with Bexsero in the MenB segment; approved in several countries for use in adolescents and young adults.

Others: Includes regional brands and newer entrants, particularly in emerging markets where local production is promoted for cost-effectiveness. These players play a critical role in shaping innovation and competition within the meningococcal vaccine industry.

Pediatrics: A major segment due to government-mandated childhood vaccination schedules. Vaccination in infancy and early childhood provides critical protection during peak vulnerability to meningococcal disease.

Adults: Growing demand due to travel requirements, military and healthcare personnel mandates, and adult booster doses. Awareness and education campaigns have also improved uptake in adult populations.

Hospital Pharmacies: Lead the distribution due to their role in public health programs, emergency outbreak response, and patient trust in institutional healthcare.

Retail Pharmacies: Play an increasing role in vaccine accessibility, particularly in developed markets where individuals can receive vaccines without visiting hospitals.

Government Supplies: A crucial segment in developing regions, where governments procure vaccines for national immunization programs through global partnerships (e.g., GAVI, UNICEF).

Online Pharmacies: An emerging channel driven by digital health trends and increasing demand for home-based healthcare services, although still limited by regulatory and cold-chain challenges.

North America holds a significant share of the global meningococcal vaccine market, driven by high healthcare expenditure, robust immunization programs, and strong awareness about meningococcal disease.

The United States leads the meningococcal vaccine market due to mandatory adolescent vaccinations (e.g., MenACWY and MenB), government support through organizations like the CDC, and the presence of major pharmaceutical companies such as Pfizer and Sanofi. Routine immunization schedules, strong cold chain infrastructure, and proactive public health campaigns support sustained market demand.

Europe is another mature and growing market, holding a significant meningococcal vaccine market share, particularly due to the widespread prevalence of serogroup B. Countries such as the United Kingdom, Italy, and Germany have included MenB vaccines, like Bexsero, in their national immunization programs.

The presence of well-established public healthcare systems, strong regulatory oversight (e.g., EMA), and public-private collaboration for vaccine access contribute to the region’s market growth. Additionally, increasing travel and cross-border disease surveillance efforts enhance the demand for broad-coverage vaccines.

The Asia Pacific region is expected to witness the fastest growth in the meningococcal vaccine market due to its large population, increasing awareness, rising healthcare investments, and expanding immunization coverage. China, India, Japan, and Australia are key contributors to the region’s market.

Government-backed vaccination drives and growing public-private partnerships are improving vaccine accessibility. However, challenges such as uneven healthcare infrastructure and vaccine affordability in low-income areas may affect full market penetration. Demand for both imported and locally produced vaccines is rising as countries prioritize epidemic preparedness.

Latin America presents a moderately growing meningococcal vaccine market. Countries like Brazil, Mexico, and Argentina have implemented immunization programs that include conjugate vaccines, particularly for infants and young children.

Public awareness campaigns and WHO-backed initiatives are helping increase vaccine coverage. However, political and economic instability, along with uneven access to healthcare in remote areas, pose challenges. Continued government support and international collaboration will be key to sustaining market growth.

The Middle East & Africa region has a diverse market landscape with varying levels of healthcare access and vaccination coverage. In Africa, particularly in the “meningitis belt” stretching from Senegal to Ethiopia, serogroup A has historically caused devastating outbreaks.

The introduction of the MenAfriVac campaign has significantly reduced these cases. However, the need for broader serogroup coverage (C, W, X, Y) remains. In the Middle East, high-income countries like Saudi Arabia and the UAE have integrated meningococcal vaccines into travel requirements (e.g., for Hajj pilgrims), supporting demand. Nevertheless, overall market growth is hampered by limited infrastructure in lower-income nations.

The meningococcal vaccine market was valued at USD 4.65 billion in 2024.

The meningococcal vaccine market is projected to grow at a CAGR of 8.05% from 2025 to 2033.

The Polysaccharide Vaccines hold the largest meningococcal vaccine market share.

The North America region is expected to witness the highest growth rate.

Major players include Pfizer Inc., GlaxoSmithKline plc (GSK) and Sanofi.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Meningococcal Vaccine Market, By Vaccine Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Meningococcal Vaccine Market, By Serotype

5.3 Meningococcal Vaccine Market, By Brand

5.4 Meningococcal Vaccine Market, By End User

5.5 Meningococcal Vaccine Market, By Distribution Channel

6.1 North America Meningococcal Vaccine Market , By Country

6.1.1 Meningococcal Vaccine Market, By Vaccine Type

6.1.2 Meningococcal Vaccine Market, By Serotype

6.1.3 Meningococcal Vaccine Market, By Brand

6.1.4 Meningococcal Vaccine Market, By End User

6.1.5 Meningococcal Vaccine Market, By Distribution Channel

6.2 U.S.

6.2.1 Meningococcal Vaccine Market, By Vaccine Type

6.2.2 Meningococcal Vaccine Market, By Serotype

6.2.3 Meningococcal Vaccine Market, By Brand

6.2.4 Meningococcal Vaccine Market, By End User

6.2.5 Meningococcal Vaccine Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping