Military Protection Glasses Market

Military Protection Glasses Market Size, Market Share & Trends Analysis Report By Material (Polycarbonate, Glass, Quartz, Others), By Application (Ballistic Protection, Laser Protection, Fire Protection, Others), By End-User (Army, Navy, Air Force, Homeland Security), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

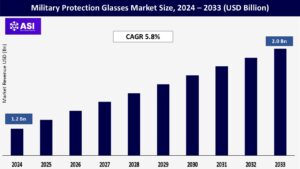

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIADR1013

CAGR: 5.8%

Last Updated : May 18, 2026

The global Military Protection Glasses Market size was valued at approximately USD 1.2 billion in 2024 and is projected to reach USD 2.0 billion by 2033, growing at a CAGR of 5.8% during the forecast period (2026–2033).

Military protection glasses are essential components in defense applications, providing enhanced safety against ballistic threats, laser exposure, and environmental hazards. Increased defense budgets, rising security threats, and technological advancements in protective materials are key drivers fueling market growth.

Rising geopolitical tensions and cross-border conflicts have led to increased global defense spending. According to SIPRI, worldwide military expenditure reached $2.24 trillion in 2023, with major countries like the U.S., China, and India investing heavily in soldier protection systems. Military forces are continuously upgrading their protective gear, driving demand for advanced military protection glasses.

The U.S. remains the largest defense spender, allocating $877 billion in 2023, with significant investments in soldier modernization programs such as the Integrated Visual Augmentation System (IVAS).

The U.S. Army has been actively procuring next-generation ballistic and laser protection eyewear under programs like the Enhanced Night Vision Goggle-Binocular (ENVG-B) and Soldier Protection System (SPS).

China’s People’s Liberation Army (PLA) is undergoing rapid modernization under its 14th Five-Year Plan, prioritizing advanced protective equipment, including ballistic-resistant eyewear, for its ground forces.

The Chinese government has significantly increased procurement of anti-laser and impact-resistant glasses to enhance soldier safety in high-risk combat scenarios. India, under its ‘Make in India’ initiative, has been bolstering domestic defense manufacturing, promoting the local production of military-grade eyewear to reduce dependency on imports.

Programs such as the Future Infantry Soldier As a System (F-INSAS) are driving the demand for high-performance ballistic glasses for frontline troops. Additionally, NATO countries are ramping up investments in protective eyewear for their armed forces in response to emerging threats.

The European Defense Fund (EDF) is allocating significant resources to research and development in advanced military-grade protection glasses, supporting innovation in materials and lens technology.

With the advent of hybrid warfare, including cyber and electronic warfare capabilities, defense organizations are also focusing on specialized eyewear designed to mitigate the risks posed by high-intensity laser weapons and directed-energy weapons (DEWs). These factors collectively contribute to the robust growth of the military protection glasses market.

Innovations in material science have led to the development of polycarbonate, quartz, and laminated glass with superior impact resistance and lightweight properties.

Companies are integrating anti-fog coatings, UV protection, and laser-resistant materials to enhance soldier safety. For instance, researchers are developing smart eyewear with heads-up displays (HUDs) to improve situational awareness.

Military-grade protection glasses require high-end materials and rigorous testing to meet NIJ, MIL-PRF, and ANSI standards. The cost of advanced ballistic and laser protection solutions is significantly higher, which may limit procurement in some regions.

Geopolitical tensions and raw material shortages have affected global supply chains. Dependence on rare elements, such as boron and quartz, for high-impact-resistant glasses increases vulnerability to supply chain disruptions.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Material |

Polycarbonate Glass Quartz Other |

| By Application |

Ballistic Protection Laser Protection Fire Protection Others |

| By End-User |

Army Navy Air Force Homeland Security |

| Key Players |

Gentex Corporation Revision Military ESS (Eye Safety Systems, Inc.) Oakley, Inc. (ESS Division) BAE Systems Honeywell International Inc. Perrone Performance Leathers & Textiles Teijin Limited DuPont de Nemours, Inc. 3M Company |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Military Protection Glasses Market is segmented based on material, application, and end-user.

Polycarbonate led the market in 2024 with a 45.3% share, favored for its high impact resistance and lightweight properties. Glass is widely used in specialized applications such as vehicle-mounted protection systems, while quartz is preferred for high-energy laser protection. Other materials include hybrid composites incorporating ceramics and nanotechnology to enhance durability and performance.

Ballistic protection was the largest segment, accounting for 51.6% of the market in 2024, primarily driven by the increasing need for soldier safety. Laser protection is gaining traction due to the rising deployment of directed-energy weapons (DEWs) in modern warfare.

Fire protection remains essential for high-risk combat zones and vehicle fire suppression systems. Other applications include protection from environmental hazards such as sand, wind, and UV radiation, ensuring operational efficiency in diverse battlefield conditions.

The army segment dominated the market, comprising 53.2% of the total share in 2024, due to continuous advancements in infantry gear. The navy is seeing increased adoption of protective eyewear in naval combat and ship security operations.

The air force is investing in pilot visors and cockpit protection systems, catering to the need for high-performance visibility solutions. Homeland security forces, including law enforcement and border security personnel, are also increasingly utilizing protective glasses for specialized operations.

North America accounted for 38.4% of the global market share in 2024, with the U.S. Department of Defense (DoD) emerging as the largest investor in military protection gear.

Active contracts under programs such as the Enhanced Combat Helmet (ECH) initiative are fostering growth. Canada is also expanding its defense procurement budgets to modernize protective equipment for military personnel.

Europe held a 27.5% share of the market, with Germany, the UK, and France leading investments in modernizing armed forces. The European Defence Fund (EDF) is providing substantial funding for research and development of next-generation military protective eyewear, focusing on improved ballistic resistance and lightweight designs.

The Asia-Pacific region is projected to be the fastest-growing market, with a CAGR of 6.8% during the forecast period. Countries such as China and India are significantly increasing their defense budgets, emphasizing soldier modernization programs.

China’s PLA modernization strategy includes advancements in protective gear, while India’s Make in India initiative supports domestic production of military eyewear to reduce reliance on imports.

In the Middle East & Africa, countries like Saudi Arabia and the UAE are ramping up defense spending to counter regional threats. Local manufacturers are collaborating with international defense firms to produce high-impact military glasses tailored to desert warfare conditions.

Latin America is also witnessing growth, with Brazil and Mexico leading defense investments. The region’s focus is primarily on peacekeeping missions and counter-narcotics operations, where advanced protective eyewear enhances the safety of deployed forces.

The global military protection glasses market was valued at USD 1.2 billion in 2024.

The market is projected to grow at a CAGR of 5.8% from 2026 to 2033.

Increasing defense budgets, advancements in protective materials, and rising security threats.

Polycarbonate dominates due to its high impact resistance and lightweight nature.

Ballistic protection leads the market, accounting for 51.6% of total applications.

North America leads with a 38.4% market share, followed by Europe.

The Asia-Pacific region is projected to grow at the highest CAGR of 6.8%.

Key companies include Gentex Corporation, Revision Military, ESS, Oakley, BAE Systems, and 3M Company.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Military Protection Glasses Market, By Material

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Military Protection Glasses Market, By Application

5.3 Military Protection Glasses Market, By End-User

6.1 North America Military Protection Glasses Market, By Country

6.1.1 Military Protection Glasses Market, By Material

6.1.2 Military Protection Glasses Market, By Application

6.1.3 Military Protection Glasses Market, By End-User

6.2 U.S.

6.2.1 Military Protection Glasses Market, By Material

6.2.2 Military Protection Glasses Market, By Application

6.2.3 Military Protection Glasses Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping