Osteoporosis Drugs Market

Osteoporosis Drugs Market Share & Trends Analysis Report, By Drug Class (Bisphosphonates, Selective Estrogen Inhibitors Modulators (SERMs), Parathyroid Hormone-Related Protein (PTHrP) Analogs, RANK Ligand Inhibitors, Calcitonin, Others), By Route of Administration (Oral, Injectable), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End User (Hospitals, Specialty Clinics, Homecare, Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

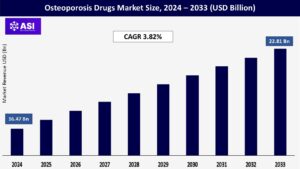

CAGR: 3.82%

Last Updated : December 15, 2025

The global Osteoporosis Drugs Market size was valued at approximately USD 16.47 billion in 2024 and is projected to reach USD 22.81 billion by 2033, growing at a CAGR of 3.82% during the forecast period (2025–2033).

The Osteoporosis Drugs Market encompasses pharmaceutical treatments aimed at preventing and managing osteoporosis, a condition characterized by low bone mass and deterioration of bone tissue, leading to increased fracture risk. These drugs include bisphosphonates, selective estrogen receptor modulators (SERMs), parathyroid hormone analogs, and monoclonal antibodies like denosumab.

Their primary use is to strengthen bone density, reduce fracture rates, and slow bone loss, particularly in postmenopausal women and elderly individuals. Key properties of these drugs include bone resorption inhibition, stimulation of bone formation, and regulation of calcium metabolism, making them vital for improving the quality of life in patients at risk of bone fractures.

The increasing number of elderly individuals worldwide is a significant driver of the osteoporosis drugs market. Aging is closely linked to bone density loss, especially in postmenopausal women and older men. According to the World Health Organization (WHO), the global population aged 60 years and older is expected to double by 2050.

As people age, their bones become more fragile, leading to a higher risk of fractures and osteoporosis-related complications. This demographic trend directly fuels the demand for effective osteoporosis medications for both prevention and treatment.

Growing awareness about bone health, supported by government and healthcare initiatives, has led to earlier diagnosis and better management of osteoporosis. Public health campaigns, bone mineral density (BMD) screenings, and the availability of diagnostic tools have significantly improved early detection rates.

This, in turn, drives the demand for therapeutic interventions. Additionally, professional guidelines recommending regular screening in high-risk groups have increased physician awareness and prescriptions of osteoporosis drugs.

One of the major restraints in the osteoporosis drugs market is the potential adverse effects and safety concerns related to long-term use of certain medications. For example, bisphosphonates, commonly prescribed for osteoporosis, have been associated with rare but serious side effects such as osteonecrosis of the jaw, atypical femoral fractures, and esophageal irritation.

These risks often lead to poor patient compliance and early discontinuation of therapy. Additionally, newer drugs like denosumab require careful monitoring due to potential rebound bone loss after cessation.

Such safety issues not only hinder patient acceptance but also make healthcare providers cautious in recommending long-term drug use, thereby slowing market growth despite the clinical need.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Drug Class |

Bisphosphonates Selective Estrogen Inhibitors Modulators (SERMs) Parathyroid Hormone-Related Protein (PTHrP) Analogs RANK Ligand Inhibitors Calcitonin Others |

| By Route of Administration |

Oral Injectable |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

| By End User |

Hospitals Specialty Clinics Homecare Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Osteoporosis Drugs Market is segmented by Drug class, Route of administration, Distribution Channels and End User. Each factor plays a critical role in improving bone health management, enhancing patient adherence to therapy, and driving the development of safer, more effective treatment options for reducing fracture risk and maintaining quality of life among individuals affected by osteoporosis.

Bisphosphonates The most commonly prescribed class for osteoporosis, bisphosphonates inhibit bone resorption and are typically used as a first-line therapy. Drugs like alendronate and risedronate fall into this category. This segment holds a major share due to its long history of clinical use, cost-effectiveness, and availability in both oral and injectable forms.

Selective Estrogen Receptor Modulators SERMs, such as raloxifene, are primarily used in postmenopausal women. They mimic estrogen’s bone-protective effects without stimulating other tissues. This segment is growing moderately, driven by the rising postmenopausal population. Parathyroid Hormone-Related Protein (PTHrP) Analogs These are anabolic agents like abaloparatide that stimulate bone formation.

Though more expensive, their usage is increasing for high-risk patients with severe osteoporosis. RANK Ligand Inhibitors Denosumab is the key drug in this category, and its use is rising due to convenient dosing (once every six months) and effectiveness in fracture reduction, particularly in elderly and cancer-related osteoporosis cases.

Calcitonin Once widely used, this segment is now declining due to concerns about efficacy and cancer risk. However, it still sees limited use in pain management related to vertebral fractures. Others Includes emerging drug classes and combination therapies under research and development, contributing to future market innovation.

Oral Dominates the market, especially for bisphosphonates and SERMs, due to ease of use and patient preference. However, poor gastrointestinal tolerance in some patients remains a drawback. Injectable Gaining traction, especially for drugs like denosumab, teriparatide, and abaloparatide.

Preferred for patients who cannot tolerate oral medication or require less frequent dosing. This segment is expected to grow at a faster CAGR due to better compliance and emerging biologics.

Hospital Pharmacies Significant market share due to the availability of injectable drugs and the treatment of high-risk inpatients. Preferred for patients under specialist care. Retail Pharmacies A large share of bisphosphonate and SERM sales occur here, especially for maintenance therapy prescribed in outpatient settings.

High accessibility and convenience are driving this segment. Online Pharmacies Rapidly growing, driven by the convenience of home delivery and increasing digital adoption, especially in urban areas and among the elderly during the post-COVID era.

Hospitals Key treatment centers for severe cases, especially involving injectable therapies and inpatient care. High use of advanced diagnostics and specialist interventions support this segment. Specialty Clinics These include endocrinology, rheumatology, and gynecology clinics that manage osteoporosis in outpatient settings.

Growth is fueled by increased awareness and preventive care initiatives. Homecare Rising with the availability of self-administered injectables and oral drugs. This trend supports patient-centric care and improved treatment adherence among the elderly. Others Includes research institutions and rehabilitation centers using osteoporosis drugs as part of recovery and supportive care.

North America holds the largest share in the global osteoporosis drugs market, primarily due to its well-established healthcare infrastructure, high awareness of bone health, and a growing geriatric population. The U.S. drives most of the regional demand, with a large base of postmenopausal women and advanced diagnostic and treatment facilities.

High healthcare expenditure and favorable reimbursement policies also support early diagnosis and long-term therapy adherence. In addition, the presence of major pharmaceutical companies and ongoing clinical research in osteoporosis therapeutics contribute to the region’s market dominance.

Europe is the second-largest market, with countries like Germany, France, the UK, and Italy playing significant roles. The market is driven by a high prevalence of osteoporosis-related fractures, especially among elderly women, and a strong emphasis on preventive healthcare.

Government-supported bone health programs and national screening guidelines promote early diagnosis. However, pricing pressure and regulatory hurdles related to drug reimbursement in certain European countries can restrain market growth slightly. Nevertheless, increased adoption of biologics such as denosumab and teriparatide is boosting market value.

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. This surge is fueled by a rapidly aging population, especially in Japan, China, and South Korea, rising healthcare awareness, and increasing access to diagnostic and therapeutic solutions.

While historically underdiagnosed, osteoporosis is gaining recognition as a major public health concern in this region. Improved healthcare infrastructure, growing middle-class populations, and increased investments by pharmaceutical companies are also accelerating growth. However, challenges such as limited reimbursement and rural healthcare access remain in some developing countries.

Latin America is experiencing moderate growth, supported by increasing awareness of osteoporosis, a growing elderly population, and improving access to healthcare services. Brazil, Mexico, and Argentina are the leading markets within the region.

Initiatives by local governments to enhance elderly care and the expansion of private healthcare services are boosting demand for osteoporosis medications. However, limited availability of advanced therapies and low penetration of preventive screening tools are still notable challenges in several countries.

The Middle East & Africa region holds a smaller market share but is showing gradual growth due to rising awareness, better access to modern healthcare, and growing investment in healthcare infrastructure.

The UAE, Saudi Arabia, and South Africa are key contributors. While osteoporosis awareness is relatively low in many parts of Africa, efforts by international health organizations and local authorities to promote women’s health and aging-related conditions are expected to support market growth. However, factors such as limited diagnostic capabilities and high out-of-pocket costs for medications pose restraints.

The market was valued at USD 16.47 billion in 2024.

The market is projected to grow at a CAGR of 3.82% from 2025 to 2033.

Bisphosphonates hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Amgen Inc., Eli Lilly and Company and F. Hoffmann-La Roche Ltd.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Osteoporosis Drugs Market, By Drug Class

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Osteoporosis Drugs Market, By Route of Administration

5.3 Osteoporosis Drugs Market, By Distribution Channel

5.4 Osteoporosis Drugs Market, By End User

6.1 North America Osteoporosis Drugs Market , By Country

6.1.1 Osteoporosis Drugs Market, By Drug Class

6.1.2 Osteoporosis Drugs Market, By Route of Administration

6.1.3 Osteoporosis Drugs Market, By Distribution Channel

6.1.4 Osteoporosis Drugs Market, By End User

6.2 U.S.

6.2.1 Osteoporosis Drugs Market, By Drug Class

6.2.2 Osteoporosis Drugs Market, By Route of Administration

6.2.3 Osteoporosis Drugs Market, By Distribution Channel

6.2.4 Osteoporosis Drugs Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping